Very Strong Redbook Improvement

Narrative for the past few weeks has been the economy will strengthen in August as the number of COVID-19 cases falls. In the past few days, the decline in cases has slowed, but it’s still below the July peak and hotspots have cooled off. Next worry is about cases spiking as schools reopen. 52% of students are going to school virtually, 19% are hybrids with both virtual and in person, and 25% will be in person. Quarter that go in person will be tests for the rest of the country.

We obviously won’t have data on the impact of schools reopening until September. So far, the economy looks good. If the stock market gets too ahead of itself, we can consider pulling back on cyclical investments. It’s all about making smart bets. If you think the economy has a 60% chance of recovering quickly in the 2nd half and the cyclical stocks run wild, it’s time to take profits.

With that in mind, Redbook same store sales growth rose from -7.1% to -3.4% in the week of August 8th. This is a huge improvement in what is commonly expected to be a weak environment because of uncertainty on unemployment insurance. Investors became less focused on government stimulus once the great July labor report and the solid jobless claims reading came out. Labor market was strong even as COVID-19 cases roared higher. We are already seeing a pickup in the rate of improvement (according to jobless claims) now that cases have fallen.

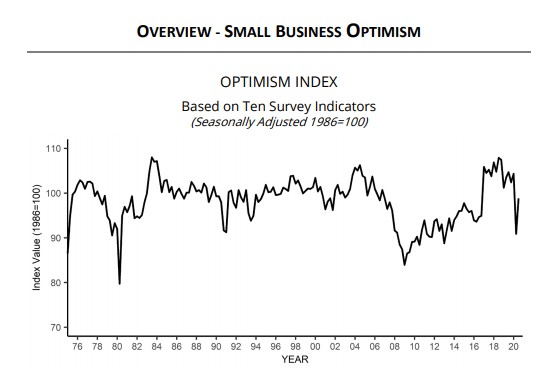

Small Business Confidence Falls Slightly

NFIB small business confidence index is unique in the sense that it showed extremely high confidence in June. That doesn’t make much sense given the hardships small businesses are facing. In July, the index fell from 100.6 to 98.8 which missed estimates for 100. This is still a strong reading. Since the economy weakened in July, it’s no surprise the index fell slightly. It's still surprising that it’s this high to begin with.

Small businesses are arguably facing their worst setback ever, but the chart below shows they are more confident than they were in 2016. Remember, confidence is usually higher when the GOP is in charge. If Joe Biden wins, this index will plummet. That doesn’t necessarily mean the economy will be bad. It’s just how this survey has historically worked.

Within this report, there was one major change in sentiment. Net percentage expecting the economy to improve fell 14 points to 25%. That’s a huge swing, but it's never much of a concern with how small businesses think the economy is doing because just look at their profits/sales. In this case, it’s even less important because the economy has picked up since this survey was done. Good news is earnings trends improved 3 points to -32%. Bad news is those expecting real sales to go up fell 8 points to 5%.

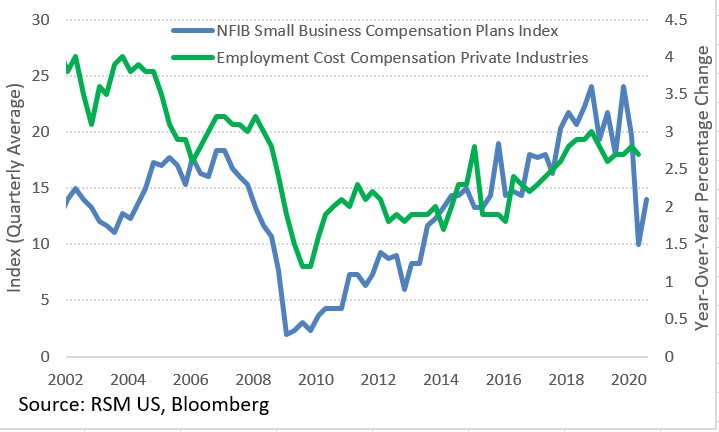

As you can see from the chart below, the improvement in the small business compensation plans index implies employment cost compensation will improve. Current job openings index fell 2 points and the plans to increase employment rose 2 points which essentially means they canceled each other out.

July PPI Beats Estimates

Usually, the PPI report isn’t a big deal, but this report seems to have stoked fears already present. Namely, with such low rates and high valuations for growth stocks, people fear a spike in inflation can stoke a phase change for the market. Since July producer inflation beat estimates, the new trend of higher rates continued.

Headline yearly inflation was -0.4% which was above estimates for -0.6% and last month’s -0.8%. Inflation without food and energy was 0.3% which beat estimates for zero and June’s 0.1%.

As you can see from the chart below, PPI’s measurement of the healthcare industries’ inflation implies the PCE healthcare price index will rise. We should get closer to the Fed’s target for 2% core PCE inflation, but we won’t get there yet. When easy core PCE comps occur next year, the Fed won’t raise rates. It wants steady 2% or even higher inflation. Fed is about to unveil a codification of when it will raise rates to show its commitment to boosting inflation.

COVID-19 Improvements Slow

Tuesday was a very bad day on COVID-19 data as Florida’s spike in deaths to a new record high caused the national reading to hit a record. There were 54,519 new cases which was very slightly below last week’s 54,648. 7 day average of new cases has flatlined for 5 days. This isn’t the good kind of curve flattening as the curve was declining in the prior couple weeks. There were 1,504 deaths which was above last Tuesday’s 1,360. Deaths will fall on Wednesday because the data is lumpy.

Higher Earnings Estimates

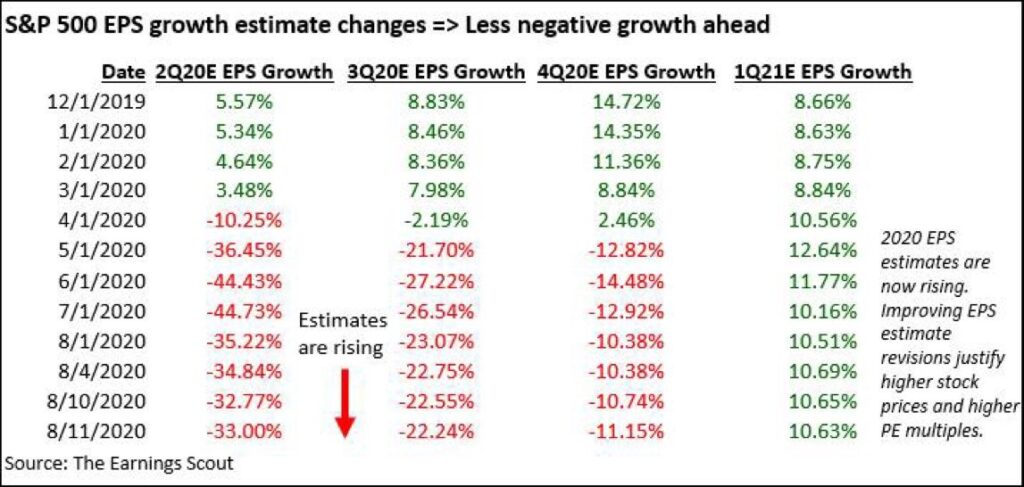

Q2 earnings season is almost done. As you can see from the table below, EPS growth was -33%. This is why stocks fell so sharply in March. Q3 EPS estimates have risen because the economy mostly improved besides some weakness in July. Growth expectations went from -27.22% on June 1st to -22.24% on August 11th. There wasn’t much guidance this quarter, but there were the most earnings estimate beats ever.

With a better economy, growth should improve in the 2nd half. EPS growth in Q2 and Q3 2021 is going to be incredibly high because of the easy comps. Normally, at this point in the year, everyone is looking at the next year. This time is different as traders have a shortened attention span. Work from home and online retail plays are still doing well even though within 1-2 years, the economy will be back to normal.

Conclusion

Redbook same store sales growth improved which is important because it signals the consumer recovered even before President Trump’s announcement of an extra $300 to $400 in weekly unemployment benefits. Small business confidence fell slightly in July, but it was still relatively high. PPI inflation was up. Higher inflation is the worst fear for treasury and growth stock investors. Earnings estimates have been improving.