Very Strong Retail Sales

The consumer appears to have weakened in the back half of June and the first half of July, but that didn’t impact the June retail sales report. That’s because consumers were optimistic in the first half of June and still had extra income to spare. There was pent up demand.

Monthly headline retail sales growth was 7.5% which beat estimates for 5.2%. That’s even though the May reading was revised from 17.7% to 18.2% growth. There were very tough comps and growth was still strong. July will likely negative growth as confidence has fallen and there will be tough comps.

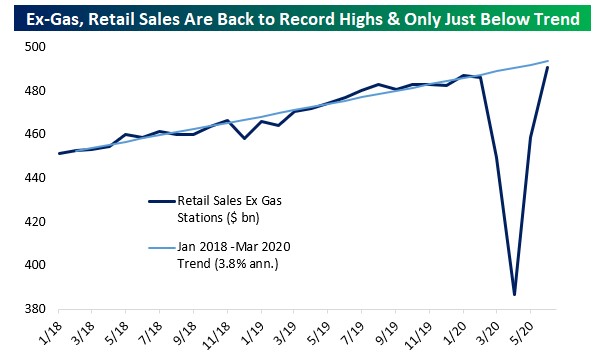

As you can see from the chart below, retail spending excluding gas is at a new record high and is just below its long term trend. Sales were 0.7% above the January peak. To make up for the decline and to account for the boost in incomes due to the stimulus, we would have predicted an even higher record in July if it wasn’t for this latest spike in COVID-19 cases.

Highest growth was at clothing and accessories stores which had sales up 105%. Electronics and accessories stores had 37.4% sales growth. This explains the huge rally in Logitech stock which is benefiting from the work from home trade. This tech stock is up 46% since May 1st.

Online sales were down 2.4% because of the tough comp and because people started going out again in the first half of June. That spells bad news for Amazon’s quarterly earnings results which will be released next Thursday. Sales at restaurants and bars were up 20% from last month. That’s about to come down sharply in July because of the restrictions in California. Headline yearly sales growth was 1.1% which would normally be considered weak, but is obviously strong because of this situation.

On the other hand, yearly control group sales growth was 6.3% which would always be considered strong (unless there were really weak comps). Finally, motor vehicle and parts sales growth was 8.3% monthly and 7.5% yearly. People started buying cars again because they are trying to avoid public transportation due to the virus.

Consumers Expect Their Jobs Back

You might be wondering why consumers were so excited about spending money in the first half of June. The answer is the people who hadn’t gotten their jobs back, expected them to come back quickly. As you can see from the chart below, the net percentage of consumers expecting to get their jobs back in the next 6 months hit a record high. To be clear, this comparison isn’t fair because there never has been a situation where millions temporarily lost their jobs.

It’s scary to think of the people who won’t get their jobs back because of the 2nd wave of COVID-19. Plus, they will be losing their unemployment benefits from the federal government. No wonder why credit card spending growth stopped increasing and sentiment fell modestly.

Good news is 40.3% of workers who lost their jobs in the pandemic were already back to work as of early July. 12.8% expect to be back at their job soon. 15.9% expect to return eventually. On the negative side, 28.5% never expect to return. We can strongly expect the permanent job losses in the July labor report to spike.

The stock market must expect there to be another stimulus because it hasn’t been selling off; it hasn’t priced in the recent slowdown at all. In fact, in the past week, cyclical stocks have rallied. Something has to give. There needs to be another stimulus or cyclical stocks need to fall.

Weakening Consumer Confidence

Consumer confidence has weakened in the past few weeks as the labor market has reversed course. As you can see from the chart below, consumer sentiment has been contracting since the end of June. It might actually be bottoming. You can argue that it isn’t bottoming because the labor market keeps worsening. If the stock market were to correct, that could catalyze further weakness in sentiment.

Some continue to believe Arizona is a leading indicator for the other hotspots which are Texas, California, and Florida. Those 3 are much more important to the economy than Arizona obviously. On Thursday, there were 3,259 new cases in Arizona which was about the same as the day before. The 7 day average fell from 3,248 to 3,135.

Another Weak Jobless Claims Report

Every week we discuss another poor jobless claims report. Are you noticing a trend? Until national COVID-19 cases stop increasing, we will have a weak labor market. We can expect weak jobless claims reports for the next 2-6 weeks. There were 73,388 new cases on Thursday which was a new record high.

There were 1.3 million initial claims in the week of July 11th which was only down 10,000 from the prior week and above estimates for 1.288 million. I have been projecting an end to the streak of declines which could ‘shock’ the market. We barely skirted that this week.

Next week will be the survey week for the BLS report, which spells bad news for the monthly reading. There was a 118,000 decline in PUA claims which is the best news from this report. Because non-seasonally adjusted initial claims were up, the total NSA level was stuck at 2.4 million (there was no change).

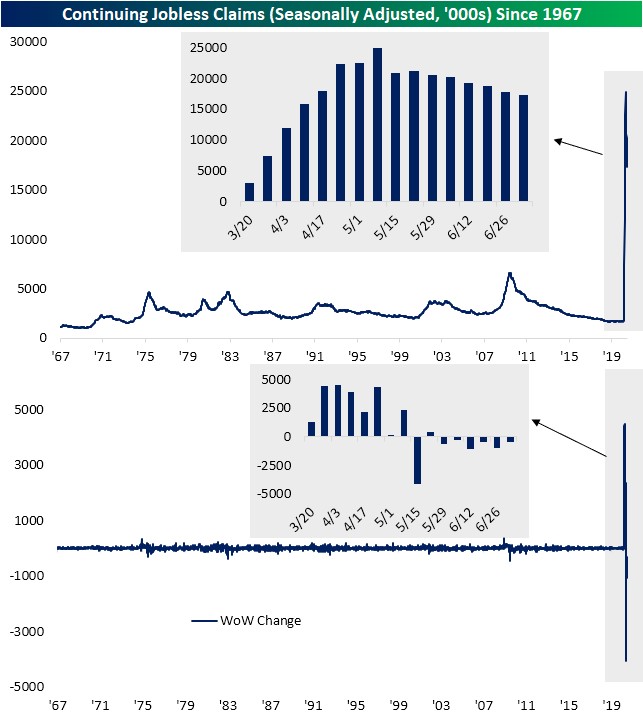

As you can see from the chart above, there were 17.338 million continued claims which was down from 17.76 million. That’s in the week of July 4th, so 2 weeks from now will be the BLS survey week. This 422,000 decline was the smallest decline since the week of June 6th. Once again, we have poor results.

Conclusion

Retail sales were strong in June, but a weak report in July is coming based on recent consumer confidence surveys and initial jobless claims in the past few weeks. Consumers widely expect to get their jobs back in the next 6 months, but many will be disappointed.