Housing Is Strong

The housing market is flat out strong. That’s weird to hear about a part of the economy because most of the economy is weak on an absolute basis, but improving on a rate of change basis. Housing market is strong and improving. That’s because the demand that usually occurs in March was simply delayed. It wasn’t removed like so many people thought. It makes sense that people thought the demand would be gone because demand is weak for most non-essential items. If there was a modest dip in prices, buyers snapped that up. They are enjoying the low rates.

In the week of May 28th, the 30 year fixed mortgage rate hit a record low of 3.15%. Since then, rates have risen to 3.21%, but that’s still one of the lowest readings ever. It’s possible that some people will start moving from cities because of COVID-19 which would cause an increase in demand for single family houses. That trend likely hasn’t started yet because COVID-19 isn’t gone yet.

Thousands of rich people left NYC when the shutdowns started. They probably have plans to come back in the summer. We don’t know how this virus will impact tastes. After all, this virus is a rare event. On the other hand, if some people switch to working from home, they can move away from the city for more affordable housing.

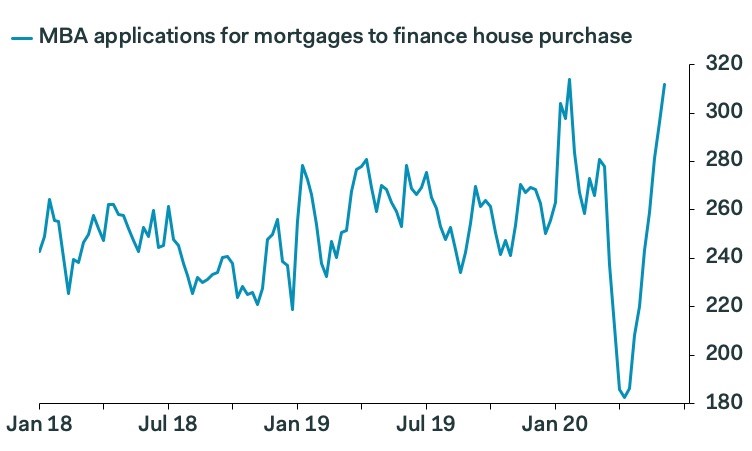

In the week of June 5th, the MBA composite index was up 9.3% weekly after falling 3.9%. The refinance index rose 11% after falling 9%. Obviously, rates are at a record low, but rates have been low for years. There is certainly an uptick in refinances, but it won’t hit previous highs. There are 2 theories on this.

You can say people are worried about more important things and the banks are busy which will limit refinancing. On the other side, you can say people have more time on their hands and are more than willing to save as much as they can because they may have lost their job. The follow up is the people who are in forbearance can’t refinance.

Purchase index was up 5% weekly after rising 5% the prior week. Unadjusted purchase index was up 15% from last week and 13% from last year. As you can see from the chart above, this is almost as high as the index has ever gotten. The housing market was very strong before this recession.

It's shocking how quickly it recovered. This is obviously much different than the last recession because the last one was caused by the bust in the housing bubble. This is just like how tech rebounded quickly after the last recession as the prior one was caused by the tech bubble burst. Bubbles don’t repeat.

Very Weak Inflation As Expected

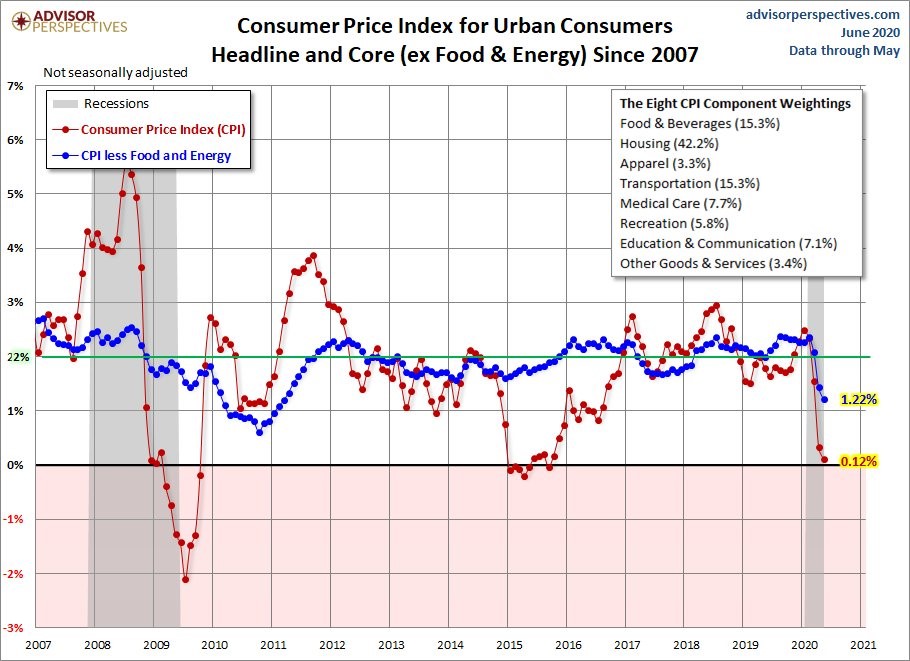

Fed thinks PCE inflation will be 0.8% this year and core inflation will be 1%. CPI inflation is almost always higher. Monthly headline CPI was -0.1% and yearly CPI was 0.1%. Monthly CPI was up 7 tenths and yearly CPI was down 2 tenths. That’s all about comparisons. Core CPI was -0.1% monthly and 1.2% yearly. Monthly rose 3 tenths and yearly fell 2 tenths. You can see in the chart below that this is the lowest core CPI since early 2011 and the lowest headline CPI since late 2015.

Food inflation was strong and energy inflation was very weak as you’d expect. Food inflation was 4% as food at home prices were up 4.8% and food away from home prices were up 2.9%. Meats, poultry, fish, and eggs inflation was 10%. There was a beef shortage which drove prices higher. Energy inflation was -18.9% even though oil prices rebounded last month. The decline was caused by the -33.2% inflation in energy commodities.

Fuel oil prices were down 37.5% and gas prices were down 33.8%. Within the core rate, commodities prices were down 1% and services less energy prices were up 2%. Apparel prices were down 7.9% as stores like JCPenney went bust. A lack of demand caused discounting. Transportation services prices were down 8.7%. Medical care services inflation was high again as it was 5.9%. Shelter inflation was low as it was 2.6%.

Very Strong Jobless Claims Report

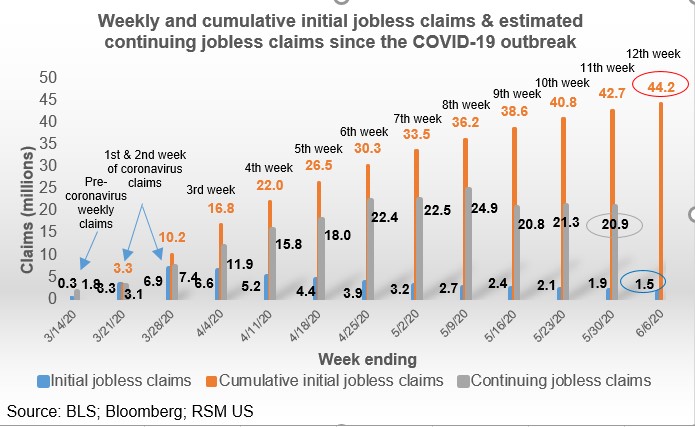

This was a very strong jobless claims report even though stocks fell sharply on Thursday. They didn’t fall because of claims. Last week’s initial claims were revised 20,000 higher to 1.897 million. In the week of June 6th, initial claims fell to 1.542 million which beat estimates for 1.565 million. It’s amazing that after reaching such high unemployment with the economy almost fully reopened that there are still more initial claims than at any point prior to this cycle.

We could finally see claims fall below their previous record high this summer if there aren’t more lockdowns. On a percentage basis, growth was -18.7% which is the lowest rate since April 11th. Last week had growth of -10.6%.

As you can see from the chart below, continuing claims fell for the 2nd straight week as they were down from 21.268 million to 20.929 million. That’s the 3rd reading below the peak on May 9th. This latest report is from the week of the 30th which means in 2 weeks we get the report that goes with the sample week of the BLS report. It seems like the recession likely ended in May or June. Data isn’t getting worse anymore.

However, we could see further weakness if shutdowns come back. Most don’t expect them to, but it’s not out of the realm of possibilities as the market learned the hard way on Thursday. Based solely on initial claims, the stock market should keep increasing unless it sees them spiking.

As you can see, cumulative claims this recession have been 44.2 million in just 12 weeks. There will be many months in this recovery where it feels like we are still in a recession because we started from such a rough point.