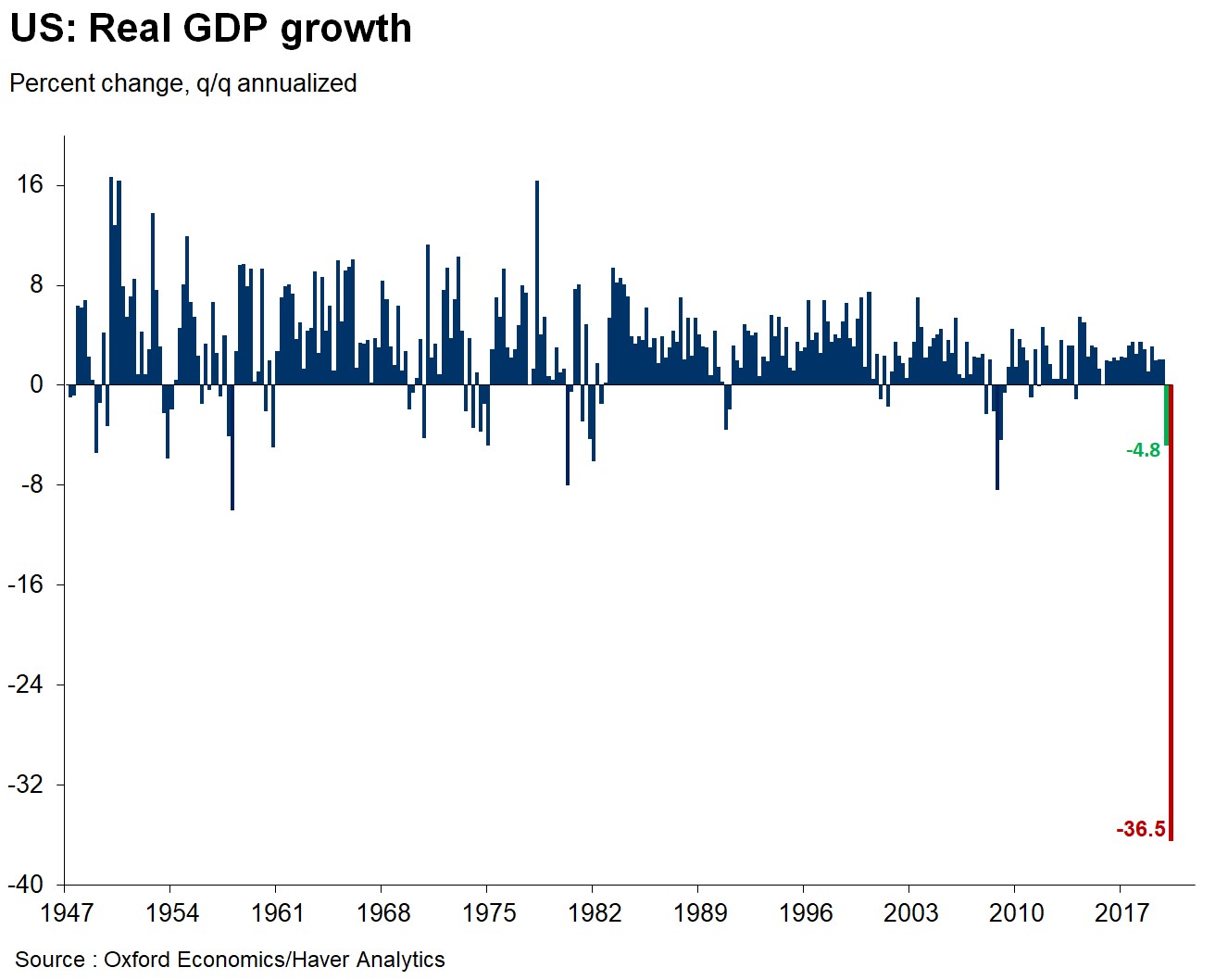

Q1 GDP Growth Was Bad & Q2 Will Be Worse

Q1 GDP report showed -4.8% growth which missed estimates for -3.7%. 2.25% of the decline actually came from healthcare because elective surgeries were delayed. This is the worst growth since the last recession as the chart below shows. The chart also includes Oxford Economics’ Q2 estimate which is -36.5%. That would be the worst quarterly annualized growth ever.

We aren’t even 1 month through Q2, but it’s clear it will be much worse than Q1. GDP Nowcasts because we know the results will likely be awful, but also that it won’t last. This estimate isn’t outlandish because GDP sank at an annual rate of 48% in March. April was probably worse for the economy than March. May should be similar to March. June will be better than the prior 3 months, but still much worse than the first 2 of the year.

Real consumer spending fell 7.6% which missed estimates for a 1.5% decline. Prices rose 1.3% which beat estimates by a tick. CPI will likely fall below zero in April and May. Powell stated at the presser, which I will review next, that "Anchored inflation expectations should prevent deflation." Oxford Economics is calling for PCE deflation in May. PCE is usually below CPI, so it has a better chance of going negative. They are also calling for core PCE to fall below 0.5% yearly which would be the lowest core inflation rate ever.

As if we needed more of a reason for the Fed to cut rates, deflation adds pressure for the Fed to be dovish. Fed worries more about deflation than inflation because it feels it can fight inflation better (by hiking rates). And the Fed has been trying to generate inflation for years. Now the fight will get 10 times harder.

Business investment fell 8.6% which is quite bad on its own. It will be worse in Q2. Residential investment rose 21% as the housing market was exceedingly strong in the first 2 months of the year. Remember, we had a warm winter. Inventories dragged growth by a half a percentage point. Net trade helped growth by 1.3 points as exports fell 8.7% and imports fell 15.3%. Government spending was up 0.7%.

Government spending will be a much bigger component of growth in Q2 since it has implemented massive stimulus measures. State and local governments are facing a budget collapse which is why the Fed extended its municipal bond purchases to smaller cities.

Within the report, services hurt growth by 4.99% making this the worst quarter for services on record. Residential investment’s 0.74% contribution to growth was its biggest contribution since Q3 2003. Imports helped GDP growth by 2.32% because of weakening demand.

Obviously, China wasn’t able to import as many goods to America because of COVID-19. Domestic final private demand growth fell from 1.15% to -5.69%.

Transportation services contributed -0.74% to GDP which is more than twice as bad as the trough in the 2007-09 recession. Food and beverages purchased helped GDP growth by 1.11% which is over triple the highest impact since the mid-1990s. Clothing and footwear hurt growth by 0.78% which was over double the trough of the last recession. It's worth mentioning these impacts because of how unusual this situation is.

Seasonally adjusted annual growth in food at home was over 20%, while it was almost -30% for restaurants, bars, and hotels. Personal savings increased from $1.27 trillion to $1.6 trillion which increased the rate as a percentage of disposable personal income from 7.6% to 9.6% which is the highest rate since 1992 outside of the blip in 2012. This money could help boost the economy in the 2nd half as there is some pent-up demand.

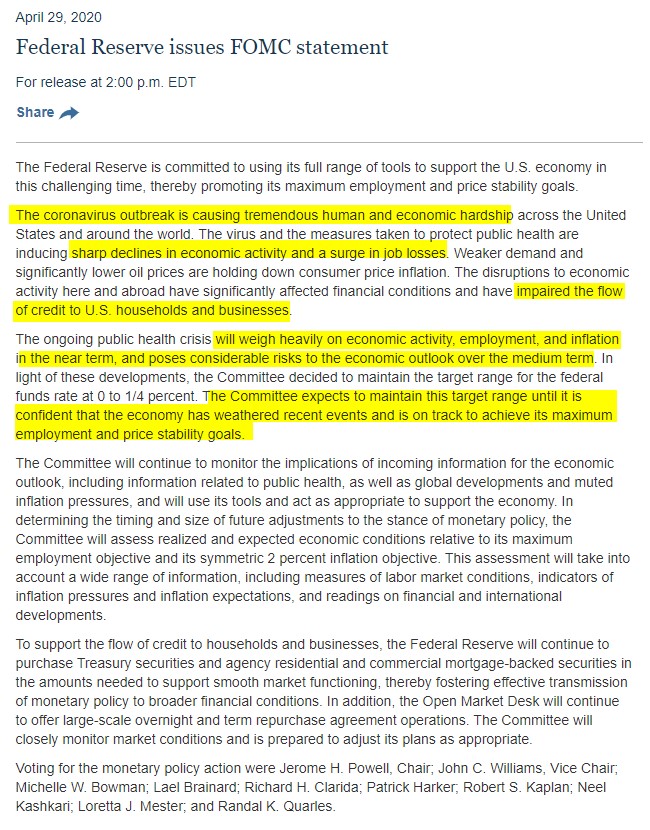

No Rate Cut As Expected

Fed didn’t cut rates because they are already at zero and cutting them to the negatives is counterproductive. And the Fed would rather do QE than cut rates below zero. The image below shows the changes the Fed made to the statement.

That sentence on the coronavirus is obvious. It shows the Fed is taking this situation seriously as we already knew it was when it cut rates to zero last month. There have been “sharp declines in economic activity and a surge in job losses.” The Fed is extremely negative on the economy as it should be. There was “impaired flow of credit” to households and firms. That’s why the Fed is lending to small businesses and the government boosted unemployment insurance payments.

Fact that the Fed said this “poses considerable risks to the economic outlook over the medium term” rather than the short term shows the Fed is ready and willing to be extremely dovish for multiple quarters if necessary. Fed expects rates to stay at zero “until it is confident that the economy has weathered recent events.” So the Fed can’t be any more dovish than that. One of the main tools the Fed has left is to buy stocks, which we don’t expect it to do in this cycle since the shutdowns are ending and stocks are rallying.

Powell stated, “Overall economic activity will likely drop at an unprecedented rate in the second quarter.” He understands how bad the Q2 GDP report will be. It will set records. Adding to the extremely dovish guidance, Powell stated, “It may well be the case that the economy will need more support from all of us if the recovery is to be a robust one. Will there be a need to do more though? I think the answer to that would be yes.”

Fed is ready and willing to do whatever it takes to get the economy back on track. There is no limit to what the Fed can do. He said, “We have a number of dimensions on which we can still provide support to the economy as you know our credit policies are not subject to a specific dollar limit.”

The stock market has been rallying in the past month because it has become clear the Fed will go to the end of the Earth to save the economy.