Weak Earnings Guidance

In a shock to no one on the planet, Q1 earnings season has been weak and guidance has been mostly non-existent. The situation is so unusually negative that when a company reports earnings and gives disappointing guidance, it’s a positive because at least there was guidance. We saw that play out with Intel’s earnings report.

Guidance is usually the most important factor with earnings season, but now the entire quarter is being thrown out. Investors love to see a breakdown of exactly when the results started getting bad and if they improved in April. Generally, weak results are being ignored and people are buying almost everything.

If you think about why earnings are important, it helps you realize why this quarter didn’t matter. Investors care about the future exclusively. Latest results give you the best vision into the future usually. An exception would be a retailer’s non-peak quarters (everything but Q4). Those don’t tell you much. Since the economy was shut down, this quarter tells you nothing about the future.

These reports don’t even tell you how recession resistant a company is. They tell you how pandemic resistant a company is, which doesn’t matter unless you are forecasting multiple pandemics in your discounted free cash flow models. Pretty much every company said there was a severe drop off in March and a slight recovery in April. Investors are now modeling modest improvements in the following few months, with a return to normalcy over the next few quarters.

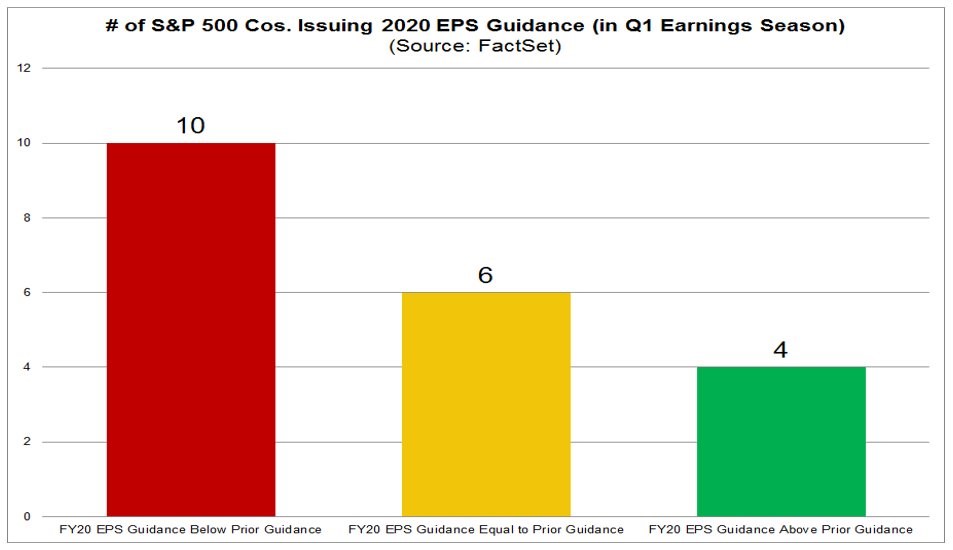

Let’s look at the details on Q1 so far from FactSet. Of the first 122 firms to report Q1 earnings, 50 commented on 2020 EPS guidance. 30 said they are withdrawing guidance and 20 provided full year guidance. That’s an impressive feat. If you’re a company that’s contemplating giving guidance, it makes sense to give incredible conservative guidance.

You’ll get credit after it comes out and credit when you beat the estimates. You probably will get penalized if there’s another spike in COVID-19 cases anyway. No investor would expect a company to know when the pandemic will come back.

Within that stat, 8 industrials firms withdrew their guidance and 3 provided it. 7 consumer staples firms withdrew and 3 gave it. It's surpriseding that so few consumer staples firms gave guidance. Some firms are experiencing more demand than usual which might not last.

No company should extrapolate out future demand. That’s a disaster waiting to happen. Investors who think the same number of people will video conference in 2021 as they did in the spring of this year will be greatly disappointed. In both healthcare and tech, 4 firms gave guidance and 4 withdrew it. Health insurance industry is being helped by people putting off elective surgeries, but we all know these surgeries will occur in the 2nd half of the year.

Finally, as you can see from the chart above, of the 20 firms that gave guidance, 10 gave lower guidance. 6 gave the same guidance and 4 gave higher guidance. That’s an exclusive club. It’s ironic that some of the firms that gave good guidance saw their stocks fall because it was widely expected that they would do well in the shutdown.

Any companies that did well even though they weren’t expected to immediately saw their stocks rally dramatically. Think of how quickly Snap stock rallied on its better than expected report.

Redbook Sales Growth Is Bottoming

There is no evidence from the Redbook results that sales growth is bottoming. But I’m going to predict that this week’s report will be very close to the bottom in yearly growth. That’s because growth was terrible and the economy is starting to reopen. Specifically, in the week of April 25th, same store sales growth fell from -6.9% to -8.1%.

The economy is about to slowly reopen in May. Many sports plan to restart in June and July without fans in attendance. It’s clear the economy is about to get much better. Therefore, either this is the bottom or the bottom will be reached in 1-3 weeks. It probably won’t get much worse than this.

Keep in mind that the stock market is going to completely ignore April’s weak economic data as it ignored the weak jobless claims reports. April unemployment report next Friday is going to be dramatically bad. Usually, the unemployment report is on the first Friday of the month, but when Friday is the 1st, sometimes it slides back a week.

Terrible Consumer Confidence As Expected

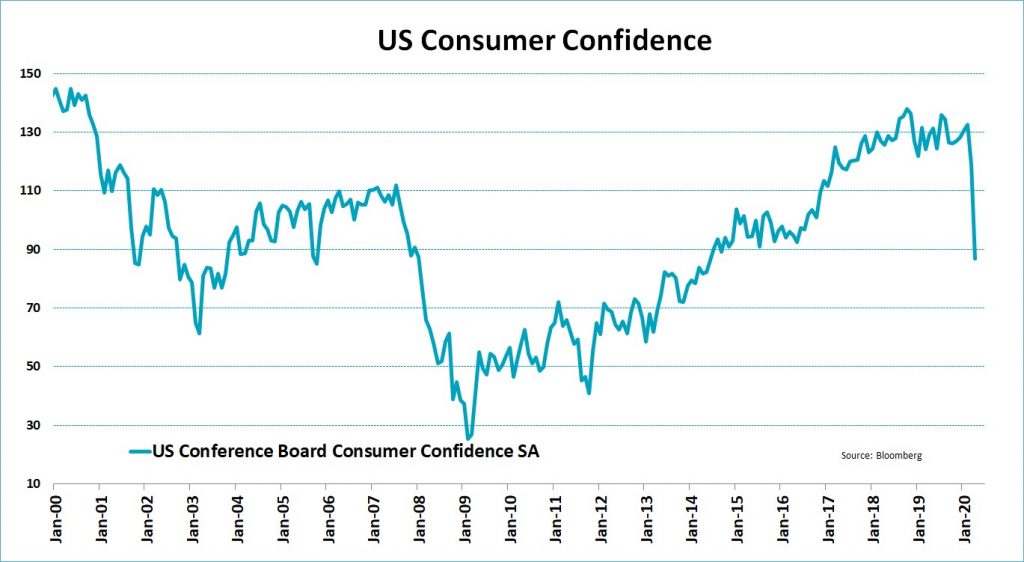

Conference Board consumer confidence index was worse than most analysts expected. As you can see from the chart below, the index fell from 118.8 to 86.9 which missed estimates for 90. Good news is we made a big leap downwards towards the early 2009 bottom. Closer we get to that bottom, the more likely the index is to increase.

We actually might see the index bottom soon (or this could be the bottom) if the economic reopening goes according to plans. Specifically, the present situation index fell dramatically from 166.7 to 76.4. That was the biggest decline on record. Surely May won’t see as bad of a decline.

Expectations index actually increased from 86.8 to 93.8. This report is an extreme version of the University of Michigan one in which expectations simply fell much less than present conditions. Consumers don’t expect coronavirus to come back in the fall. If it does, we will likely have better systems in place and more testing to combat it.

Those saying business conditions are good fell from 39.2% to 20.8%. Personally, I’d like to meet someone who thinks business conditions are good now. If the deepest recession in the past 80 years is good, then we'd all like to know what’s bad. 45.2% said business conditions are bad which was up from 11.7%.

Those saying jobs are plentiful fell from 43.3% to 20% and those saying jobs are hard to get rose from 13.8% to 33.6%. 40% expect business conditions to improve which is up from 18.7%. It’s easy to improve from a closed economy!