Negative Oil? Sort Of

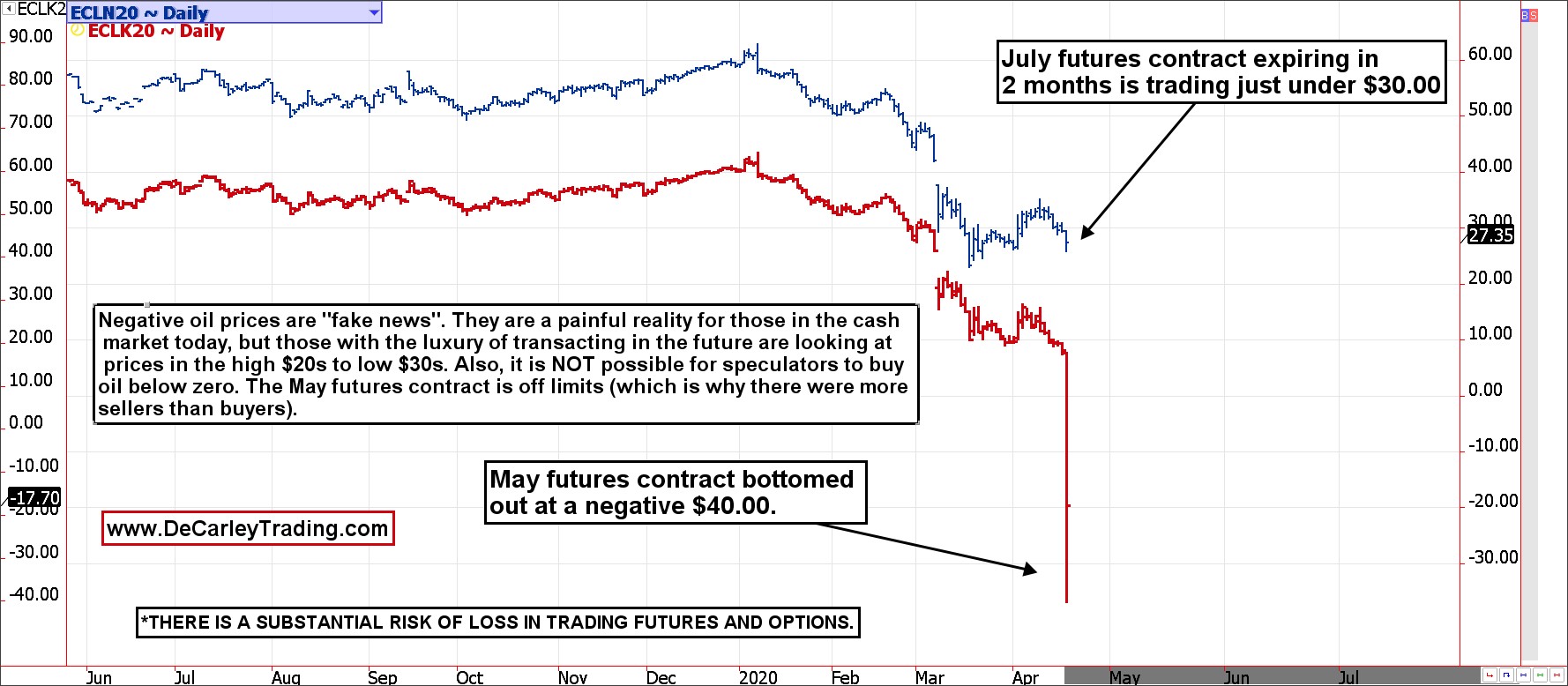

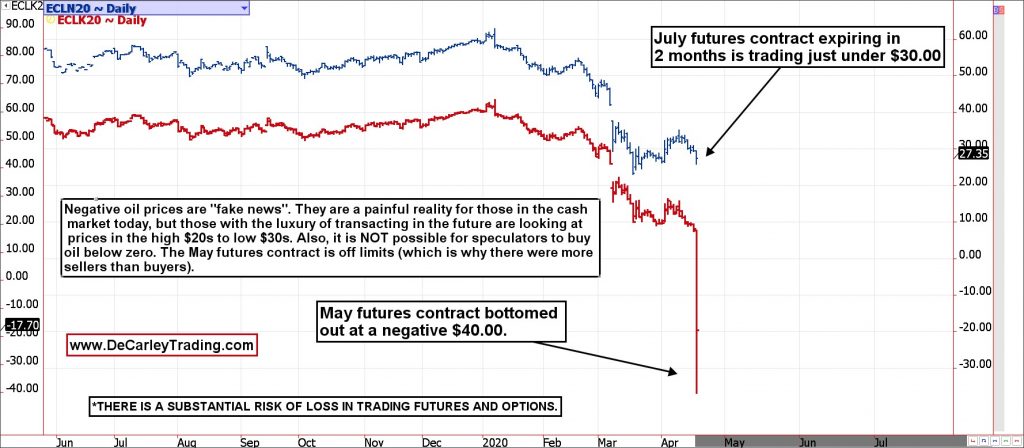

The biggest story on Monday was the decline in the May oil futures contract which expired on Tuesday. Most people understood oil futures prices could go negative in an unlikely scenario because it costs money to receive the physical commodity. Oil is expensive and difficult to contain.

That's why the shipping stocks did well on Monday as the further out contracts are much higher which is called contango. While we knew oil could go negative, the fact that WTI went to -$40 per barrel was a signal of a broken market because it doesn’t cost that much to contain.

The stock market didn’t fall much in response to this broken market and at times during the day some of the energy stocks were up. This broken market was largely irrelevant. Even for oil companies, this was like a firework show. There was a lot of pomp and circumstance, but it didn’t matter much. That’s because the real oil price is the June contract which is in the low $20s.

As you can see from the chart above, speculators can’t buy the May futures contract. There was a lack of liquidity in the cash market, but ultimately this won’t affect oil companies much and it won’t affect the price at the pump as that’s controlled by Brent. Don’t get me wrong, energy companies are in terrible shape; they just aren’t selling oil for negative prices.

Clearly, there is a lack of demand which has created record excess supply which will take many quarters to work through. The energy companies themselves might front run this, but their actual profits probably won’t show improvement until either 2021 or 2022.

Back To February

This market reminds me of February when all the action was in treasuries and most just ignored the modest decline in stocks. Back then we were worried about negative rates and now we are worried about negative oil prices. Even though stocks and oil prices have historically been highly correlated, the decline in rates was a far bigger deal.

10 year yield doesn’t have a contract that becomes meaningless like WTI did. When we see the June contract crash to $15 or below, we can be more enthused. This wasn’t huge deal. We already knew oil demand was very low.

This would have been a relatively boring day if it wasn’t for oil as stocks fell modestly. The stock market was very due for a decline. It would have been more shocking to see a rise of 0.5% than a fall of 2%. We have seen investors who missed the bottom chasing the market. Ultimately, most of the world is still shut down which makes it hard to justify the market nearing new highs.

Work from home stocks have done very well. Many of them like Shopify are huge bubbles. Stocks hit the hardest by coronavirus have rallied significantly. The market likely won't be ready to put them back where they were before the crisis. That is, not until we see how consumers react to the economy reopening.

Plus, many of them are in worse shape because they took on excess debt. We will get our first glimpse of how consumers will react in Georgia because the state plans to reopen next week. Personally, I don’t expect people to go back to anywhere close to normal because Georgia is possibly opening too early. New York will probably not open until mid-May at the earliest. New York might get back to normal quicker because people will feel safer when it opens.

Details Of Monday’s Action

S&P 500 fell 1.79% on Monday. We can expect the stock market to be modestly lower this week. Frankly, I don’t expect many gains in the next few weeks because the market has gotten ahead of itself. Nasdaq fell 1.03% as it outperformed again. Many are very bearish on the work from home stocks like Microsoft, Shopify, Amazon, Netflix, Roku, and Zoom. Obviously, Amazon and Microsoft will be fine in the long term, but they should underperform in the coming weeks. Let’s see how they react to their earnings. Russell 2000 fell 1.28%.

While some energy stocks were up in the morning and afternoon, the sector fell 3.29% as it was the 2nd worst sector on the day. Halliburton stock was actually up 0.66% after it reported its earnings. Non-GAAP earnings of 31 cents beat estimates by 7 cents. Revenues of $5.04 billion were in line with estimates and fell 12.2% yearly. Utilities sector was the worst performer as it fell 3.89%. No sector was up. Best was healthcare which fell 0.78%.

COVID-19 Update

Personally, I'm worried about the idea of Georgia reopening. We will see how that impacts its new cases. Hopefully, they don’t rise in May. As of Monday, it had 19,399 total cases and 775 total deaths. Other news of the day is President Trump is temporarily pausing immigration. Good news is New York is improving.

As you can see from the chart below, total hospitalizations are falling in the state. The situation is getting under control. New York is ahead of most states besides Washington. It probably could do a partial opening in early May. But it will be cautious because it has seen 18,929 deaths already. Parades in May and June are being canceled.

Italy had an amazing day as there were only 2,256 new cases. That’s the lowest since March 10th. This same situation could play put in America if the shutdowns last another 2-3 weeks. Finally, in Italy the number of active cases fell for the first time. It fell by 20 to 108,237.

Spain is also doing well as there were 1,536 new cases which is the lowest since March 14th. Spain also had a decline in active cases. It looked like the country’s active cases were peaking last week, but there was a spike over the weekend. Now we are back to seeing the situation improve.