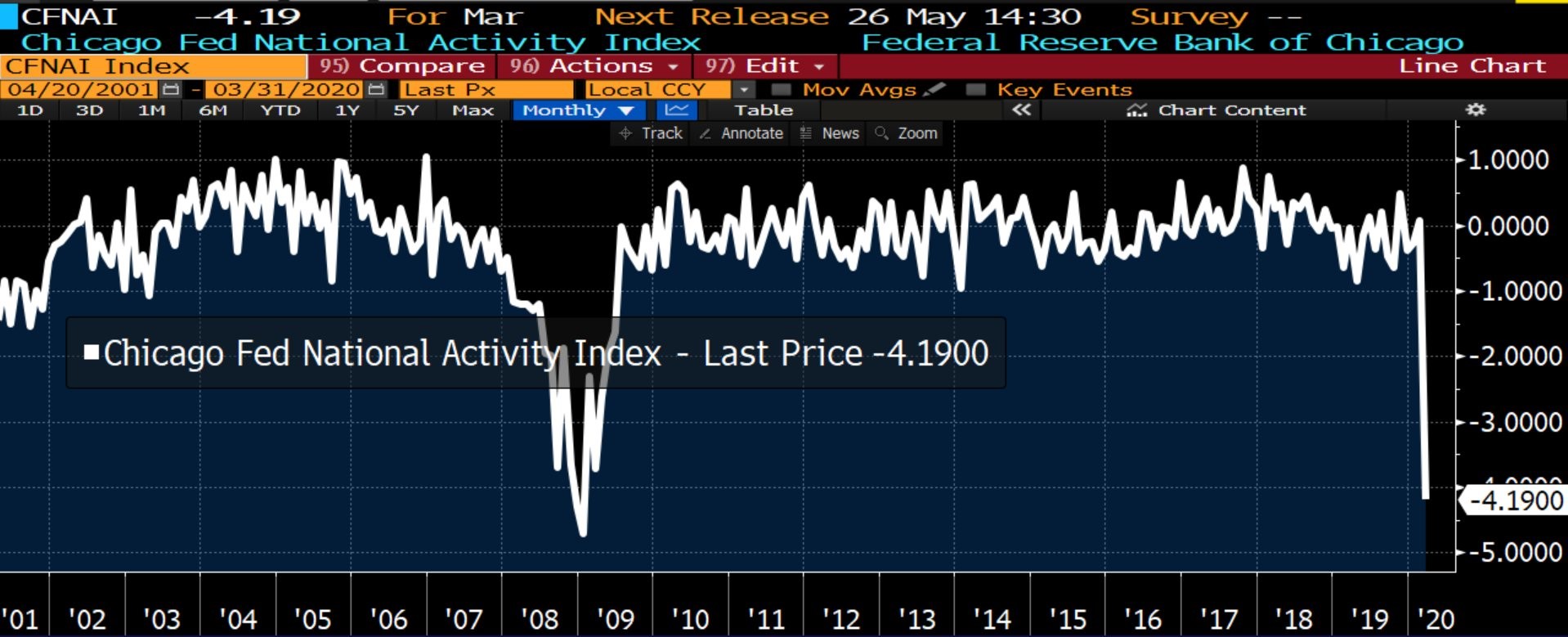

March Activity Plummets

We knew the March Chicago National Activity index would be bad. Most of the March economic reports are already out and they were terrible. However, even those low expectations weren’t met. We didn’t have a specific estimate for this report because such a guess is futile.

However, it's still surprising how bad this was because we know the data will be worse in April. As you can see from the chart below, the index fell from 6 basis points to -4.19. It’s very close to the trough in the 2007-09 recession.

There has been an ongoing discussion on how bad this recession will be. Personally, I think a depression has been taken off the table because of fiscal and monetary support. There has also been some flexibility in the system. People aren’t being kicked out of their houses for not paying the mortgage or rent.

Credit card payment due dates are being delayed. Debt covenants are being waived. The system is reacting as good as it can. Everyone knows the economy has paused. This isn’t the ruthless capitalism we are used to.

Since a depression is off the table, it's nteresting how bad this recession could get. It seems likely that this will be the worst recession since the Great Depression, which means it will be worse than the great financial crisis. Of course, that’s not a given. That’s why we're reviewing these reports.

It looks very likely the Chicago Fed index will get below the 2009 low in April. A positive revision to the March report is unlikely. There will be sharp revisions in most data points because of how severe the drop-off in activity was in the 2nd half of the month.

When the 3 month moving average falls below -0.7, it’s recessionary. Obviously, this economy is in a recession as the 3 month average is at -1.47. 18 of the indicators within the report made positive contributions, 2 made neutral contributions, 65 made negative contributions. Production indicators hurt the index by 2.72 which was down from the 6 basis point gain last month. Employment category had a -1.23 impact after rising 7 basis points.

Personal consumption fell 19 basis points after falling 2 basis points. That’s where the April report will be much worse. There won’t be anymore grocery hoarding in April. Plus, the consumer is in much worse shape than the first half of March. Finally, the housing category hurt the index by 19 basis points instead of 2 basis points. That also will be weaker.

Very few people are buying houses. That’s why the housing market index’s traffic index was in the 5th percentile. With that in mind, the Chicago Fed index will likely hit a new record low in March.

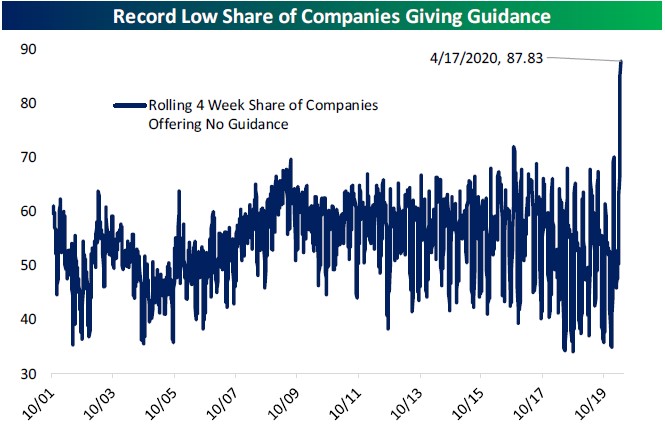

There Is No Guidance

Guidance is the most important part of earnings reports. It’s way more important than prior quarter EPS or revenues because it tells you what the firm thinks about the future. The future is the only thing that that matters to investors. This is about to be one of the worst earnings seasons ever. You might assume guidance will be terrible.

However, it’s worse than there being bad numbers. There are no numbers! As you can see from the chart below, 87.83% of firms haven’t given guidance in the past 4 weeks. Obviously, not many firms have reported in the past month, but this trend will likely continue. This is by far the lowest percentage of firms giving guidance ever.

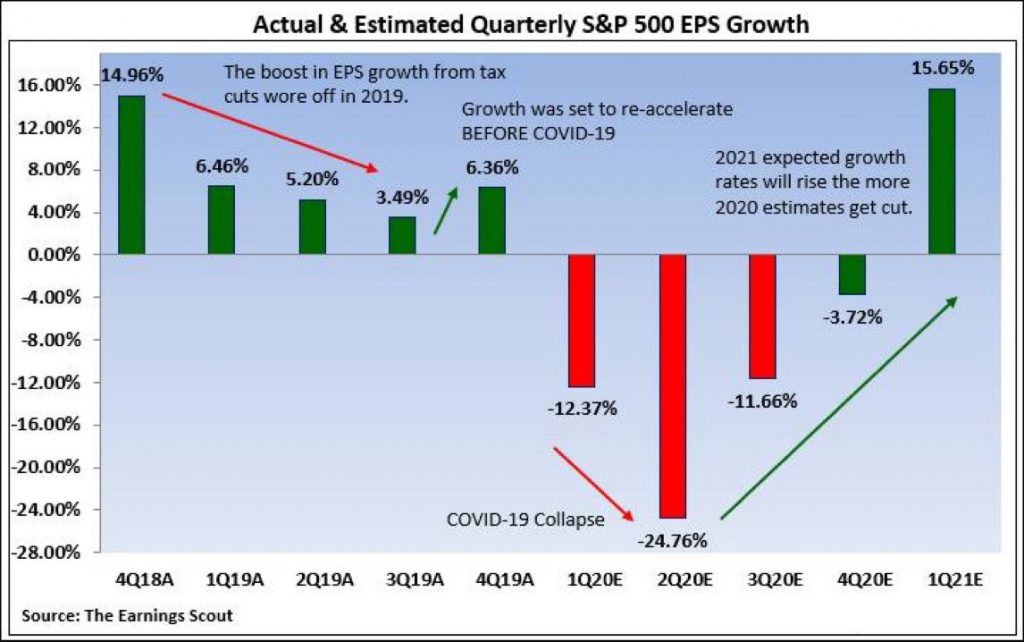

According to Morgan Stanley, Wall Street expects a 15% decline in EPS in 2020. They expect a 14% decline in Q1 and a 25% decline in Q2. Calls for a 100% decline or more by Goldman Sachs were greatly exaggerated because top down estimates don’t mean much. Anyone can come up with any reason for an overarching prediction. Bottom up estimates rely on analysts actually doing work on individual companies.

These estimates are based on company specific reports, not on extrapolated bearishness from a few negative macroeconomic numbers. Healthcare, tech, utilities, communication services, and consumer staples sectors all will have positive earnings. Other sectors will need to lose significant money to make up for those earnings.

Ignore The Things You Don’t Like

We are seeing some investors just ignoring negative results in 2020 because they are a one off. This makes sense for long term investors. But recognize that stocks always fall in recessions even though the earnings declines are always short lived. This is about uncertainty, the decline in buybacks, and the decline in investment capital. People who don’t have jobs, don’t have access to capital to invest the normal amount they put in to their retirement funds every month.

2020 earnings are probably still valid even though the bulls have begun to look past them. Earnings season will be front and center in the next 2 weeks. Q2 EPS estimates will fall dramatically. Soon estimates for the 2nd half will be far too low if we can defeat this virus and reopen the economy.

As you can see from the chart above, The Earnings Scout sees the Q1 EPS growth consensus at -12.37% and the Q2 consensus at -24.36%. From there, growth is expected to rebound, but it’s still negative. If we see Q4 EPS growth estimates below -10%, it will likely be very beatable.

Latest update as of after the close on Monday is 69% of the 54 firms reporting Q4 EPS beat estimates with -12.3% growth and 72% beat sales estimates with 3% growth. Firms tend to always beat estimates more than they miss them because estimates are lowered to a beatable range. This includes a few firms with Q1s that include March.

If analysts were able to get the correct beatable estimates for these reports, we can trust them to do so for Q2. We might see estimates for growth down to -35%. But those results will be beat, meaning there will be positive earnings in Q2.