Same Store Sales Growth Falls Again

A decline in same store sales growth in the Redbook report should continue because the initial burst in grocery shopping is over. Some people aren’t getting access to their unemployment insurance which will hurt spending. Rich and upper middle class are pulling back hard on discretionary spending.

Specifically, in the week of April 7th sales growth fell from 6.3% to 5.3%. I have some concern about the manner in which this is measured because you’d think sales would be falling, but I think the direction is accurate. This was the 2nd straight week growth fell.

Big Decline In Small Business Confidence As Expected

Small business confidence fell sharply in March as you’d expect. Personally, I can’t imagine small business confidence in April not coming near its early 2009 trough. Small businesses are the worst hit by the shutdowns. Wal-Mart and Amazon are taking market share from small retail stores.

People can’t dine out at restaurants; they need to order food. Weakness in March is only the beginning. It’s possible that there will be talks of reopening state economies by the end of the month. But that won’t counteract the extreme strife facing firms in most of April. New York will be shutdown until at least April 29th. With the continued decline in the number of new cases and ICU patients, it’s possible that in 2 weeks Cuomo announces New York will reopen in May.

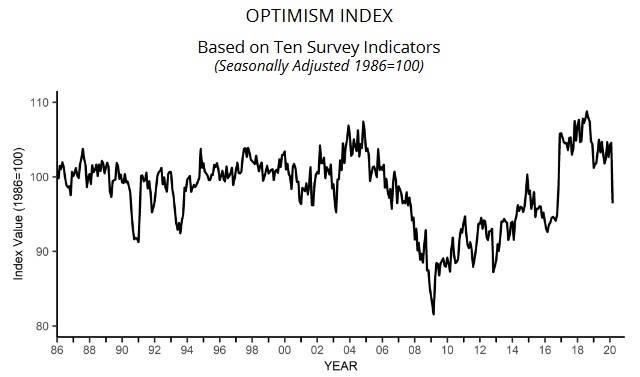

As you can see from the chart above, the NFIB small business optimism index fell from 104.5 to 96.4. This ended its 39 month streak of above 100 readings. This was its largest monthly decline in its 34 year history. It was quite high in February which gave it plenty of room to fall. It’s still in the middle of its 2018 peak and 2009 trough.

It has much further to fall. It would be shocking if it didn’t at least fall to the low 80s. As you’d expect, the specifics of the March report were a bloodbath. Only indicator that increased was current inventories which was up 2 points to -2%.

Expectations figures were the worst. Net percentage of small firms expecting real final sales to be higher fell 31 points to -12%. That was its largest drop ever. Uncertainty index rose 12 points to 92 which was its highest reading since March 2017. Net percentage expecting the economy to improve fell 17 points to 5%.

It's surprsing that more firms are optimistic than pessimistic. That will change in the April report. Percentage saying now is a good time to expand fell 13 points to 13%. Good news is the percentage of firms who said their borrowing needs weren’t met only rose 1 point to 3%. A net 4% of firms said their last loan was harder to get than the previous one which was up 3 points.

Earnings Update

Earnings season starts next week. Personally, I don’t think stocks are going to crater when most firms suspend guidance.It's unclear how any one expects firms to keep their guidance. Usually, uncertainty is bad, but in this case the uncertainty is known. Most firms will report terrible numbers in Q2.

Can you fault a firm for reporting weak results when the economy is shut down? Stocks already declined because of the shutdown in March. That’s not to say all traders will ignore earnings season. It's just that it will unlikely be the black hole for investors that some people fear.

Estimates have come down significantly in the past few days. Estimates for Q1 EPS growth fell from -6.6% to -8.35%. It’s tough to get a grasp of how bad results will be because the first 2.5 months of the quarter were fine, but the last 2 weeks were completely destroyed by the shutdowns. It’s also tough to tell if the -13.29% expected EPS growth in Q2 is low enough.

If firms don’t report guidance, analysts will be left in the dark. They will probably be conservative with their estimates. Some top down estimates call for outright losses in Q2. Good news is estimates are starting to get very beatable in Q4 as growth is expected to be 0.7%. If the shutdowns end in a few weeks, Q4 shouldn’t be hit that hard. There will be some pent-up demand unleashed.

The lower the estimates for Q1 2020 growth go, the higher the estimates for Q1 2021 go. As you can see from the chart above, estimates are for 13.12% growth in Q1 2021. Analysts expect the shutdowns to be long gone by then; therefore, they expect a recovery next year.

With the first 21 firms reporting Q1 2020 earnings, there is -1.99% EPS growth and 5.08% revenue growth. That’s not bad because the first 2 months of 2020 weren’t bad. There obviously was sharp margin contraction.

Stocks Are Just As Expensive As They Were In February

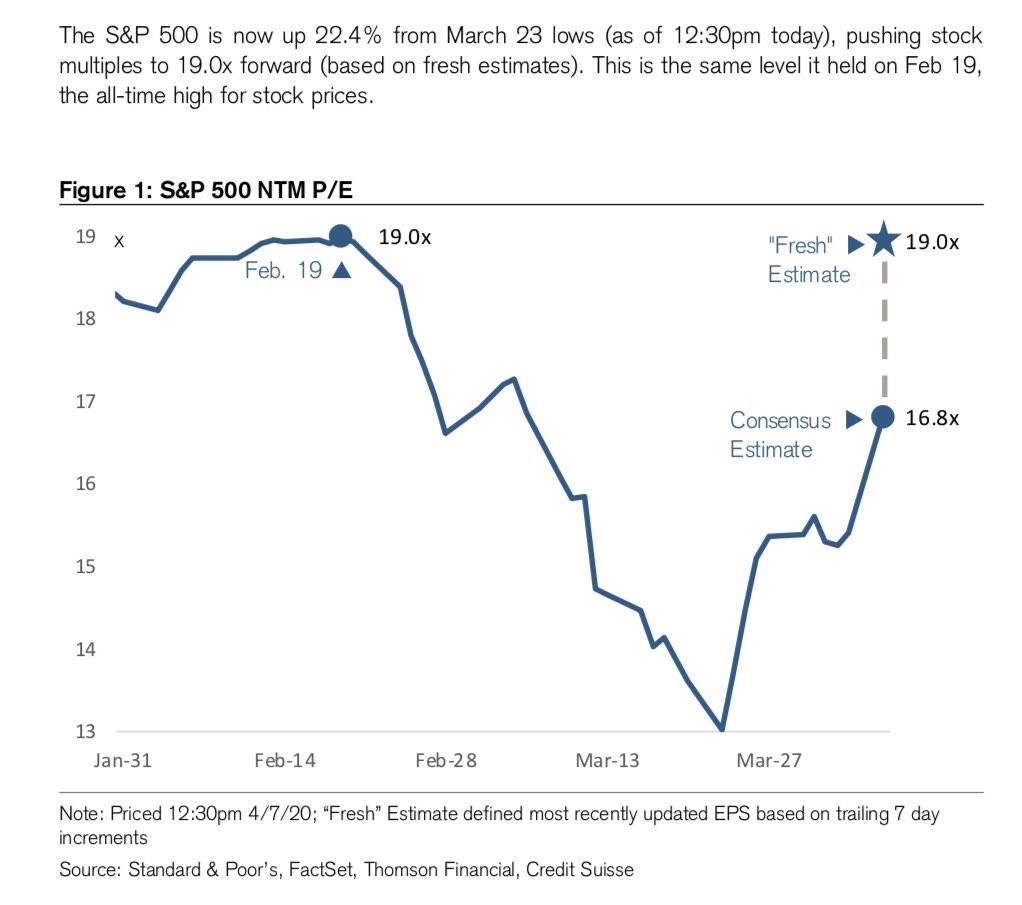

When earnings estimates fall, stocks become more expensive. Obviously, you can’t expect stocks to be cheap on a forward basis when earnings are suffering because investors look past the temporary decline. Even though stocks fall sharply during recessions, it’s common to briefly see expensive valuations based on the weaker expectations.

As you can see from the chart above, based on the consensus estimate, the forward PE ratio fell from 19 on February 19th to 13 at the bottom. Now it’s back to 16.8. If you include the recently updated estimates, the stock market is back to a 19 PE multiple already.

This is what is meant by the stock market being expensive when it falls. A key is to remember that the market’s long term value isn’t derived from 1 or 2 quarters. That’s just a blip on the radar even if earnings fall sharply. On the other hand, the decline in earnings lowers buybacks which removes a big buyer of shares.