Disastrous Quarter Ends With A Small Selloff

This week has been calm so far. S&P 500 fell 1.6% and the VIX fell 3.54 to 53.54 on Tuesday. We can expect the VIX to fall even on down days. Panic can’t last forever. It is a short emotional outburst. If stocks fall, they won’t crash like they did in March.

Personally, I think President Trump's Task Force finally threw out the ‘kitchen sink’ on COVID-19. Those experts said between 100,000 and 240,000 Americans may die. Those are grim figures which will likely scare Americans into following the CDC guidelines. That will actually prevent people from dying. As an investor and an American, I love to see a cautious approach.

Reopening the country on April 15th or Easter was never going to happen. That will be near when the peak number of new cases occurs, but not when things will get back to normal. We’ll be looking for a reopening in May or June. Fact that stocks didn’t crater when there was an increase in cases and Trump made this prognosis shows that a lot of the negatives are priced in.

Improvement in Italy provided the first wave of buying last week. We need to see cases peak in early to mid April in America for there to be a 2nd wave of buying.

Q1 Was Very Bad

Q1 was a disaster. Only 1 Dow stock was up. Microsoft was up 1 basis point. This was the worst Q1 in the 125 year history of the Dow. It was the worst quarter since 1987. VIX was up 314% which was its largest gain ever. WTI oil was down 66% which was its largest quarterly drop ever. WTI is the lowest since 2002. There even was a point where Wyoming oil briefly traded at a negative price.

Many places where oil doesn’t have access to pipelines are trading in the single digits. The S&P 500 fell 20% in Q1. This was the worst Q1 ever. Previous worst was 1938 when stocks fell 19.4%. In the rest of the year it gained 54.6%, but obviously that doesn’t mean much.

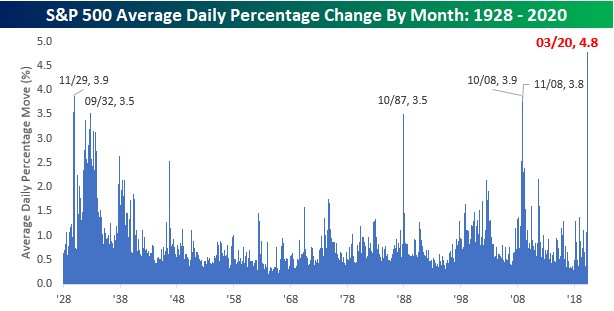

As you can see from the chart below, the average daily move in the S&P 500 was 4.8% in March. That’s the highest ever by a significant margin. Previous high was 3.9% in November 1929 and October 2008. Many are quite certain the moves won’t be as large in April.

By the end of the month, most firms will have reported Q1 earnings and the number of new daily cases in America will have peaked. There will be much less uncertainty about COVID-19.

Details Of Tuesday’s Modest Decline

Nasdaq fell 0.95% and the Russell 2000 fell 0.45%. Dollar Tree was the worst stock in the Nasdaq as it fell 8%. Tesla rallied 4.4% as it was the 3rd best performer. Within the S&P 500, the best sector was energy which rose 1.63%. It’s tough to imagine oil falling to the mid-teens. We’ve seen calls for negative WTI oil which to me signals the negativity has reached its peak. We’ve seen a mad rush to buy tankers because oil demand can’t keep up with supply which means it needs to be stored.

A question many are asking is “how can it get worse?” Answer is if the price war lasts longer and if COVID-19 lasts longer. However, one can argue that those negative catalysts simply keep oil in the low $20s rather than send it even lower. Most people expect oil to rebound eventually. If they didn’t, no one would buy Chevron or Exxon. They would have zero long term value. Their oil would be worth more in the ground than the cost to pull it out.

Worst sectors were utilities, real estate, and financials which fell 4.02%, 3.26%, and 2.99%. JP Morgan stock fell 3.71%. It’s up 14% from its low last week. Long bond still has a recessionary yield which makes sense because we are in a recession. 10 year yield is at 62 basis points. It’s getting closer to its record low of 38 basis points. It will possibly hit a new record low this month. But in a more orderly fashion than its rally in February and March.

COVID-19 Update

The situation is getting much better in Italy. A problem for the hospitals is that there are still 77,635 active cases. They will be in a lot of trouble for weeks after the number of new cases falls to a miniscule level. Even if there were zero new cases, Italy would be in trouble for another 3 weeks.

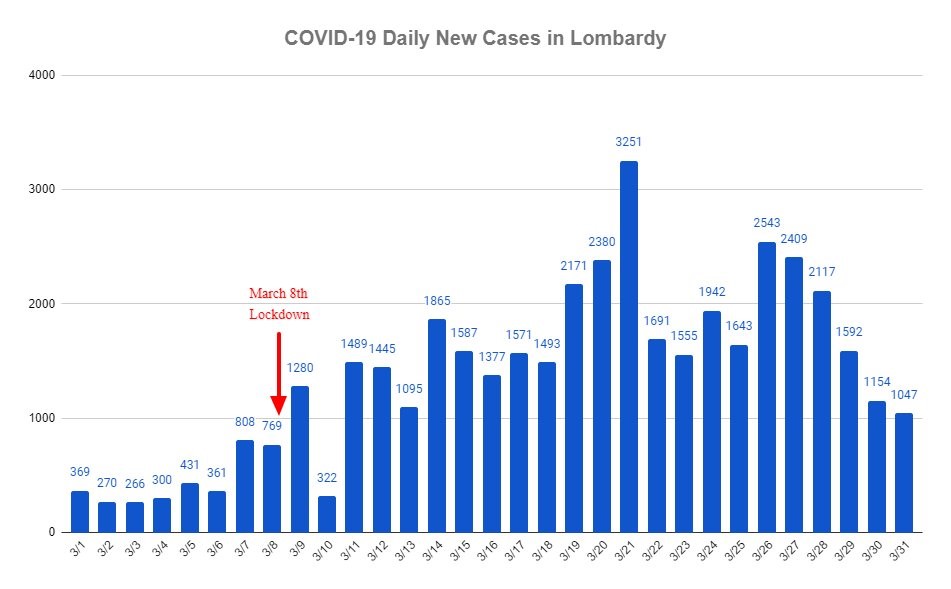

Good news is we are headed towards zero. There were 4,053 new cases on Tuesday which was 3 more than Monday which had the lowest number since March 17th. As you can see from the chart below, the number of new cases in Lombardy fell to 1,047 on the 31st which was the lowest since the 10th. This was the hardest hit area of Italy. It's like New York City for America.

The situation in America got way worse on Tuesday. There were 24,742 new cases. Personally, I expect that spike to lead to a leveling off because. Data is lumpy and we have seen lower growth in the past few days. There have now been 75,983 cases in New York and 4,055 deaths in the entire country. Good news is the odds of there being more than 1 million cases in America by April 15th have fallen to 29%.

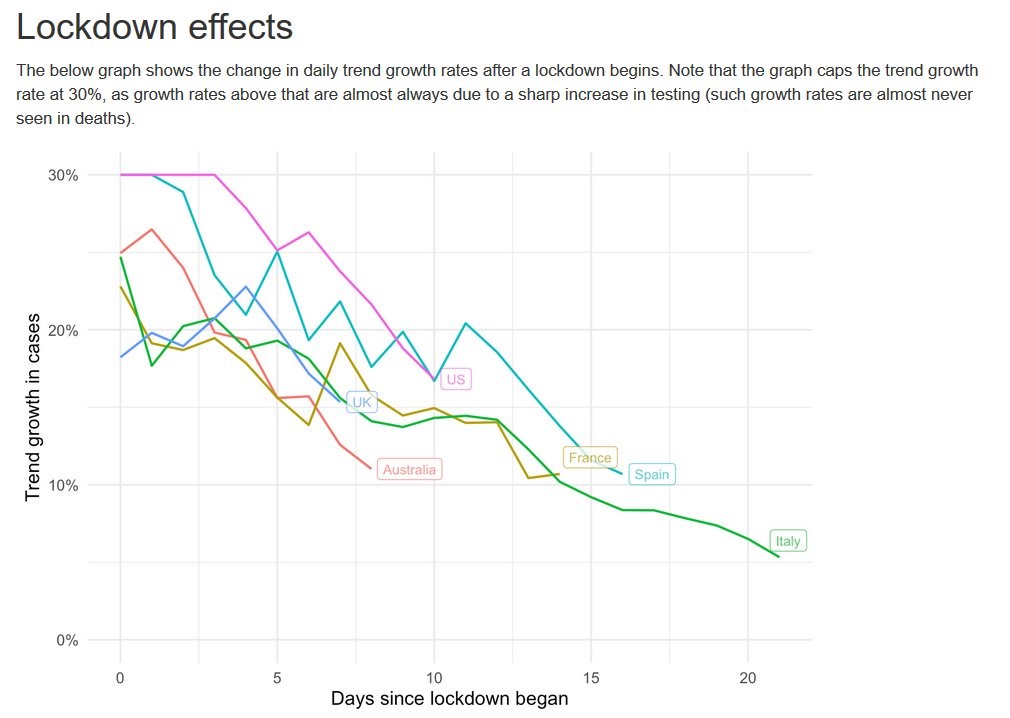

Further good news is seen in the chart above. As you can see, after lockdowns are put in place, the growth rate in cases falls over time. After 21 days of being locked down, Italy has reached about 5% growth. Spain has fallen to 10% growth. American growth is falling, but the nominal number of new cases per day is still rising.

Hopefully, that peaks within the next week or so. It looks like the situation is peaking in New York City. Hospitals have been overwhelmed. They may likely be in dire straits for the next few weeks even if the peak has happened.

1 Comment

Lora Leone

April 1, 2020Great article! Thanks for sharing!