Hiring Slows

In a shock to no one, the data shows hiring is slowing. The only companies that are hiring are the ones seeing more demand because of COVID-19 which is a select few. In this bucket you have necessities like groceries and healthcare. You also have online retail, but even Amazon is running into difficulties.

Its workers in a warehouse in Staten Island, which has been hit hard by the coronavirus, are striking because of unsafe working conditions. This story highlights the struggle facing all workers who don’t work from home. The economy isn’t built to handle this much work from home.

According to a survey of hourly workers by Homebase, only 6% of workers said they can do their work from home. Personally, I see this situation causing more people working from home in the long term. Obviously, this extreme situation where no one can leave the house will not continue.

It's jsut that more work will likely be done remotely. That trend was already in place with companies like Zoom and DocuSign heralding the change. The trend will only grow stronger in the next few months.

A current spike in unemployment is being catalyzed by the decline in hiring more so than uptick in layoffs. Number of separations, which is firings plus quits, fell during the last recession. Number of hires fell dramatically. That same sharp decline in hiring is occurring in this slowdown.

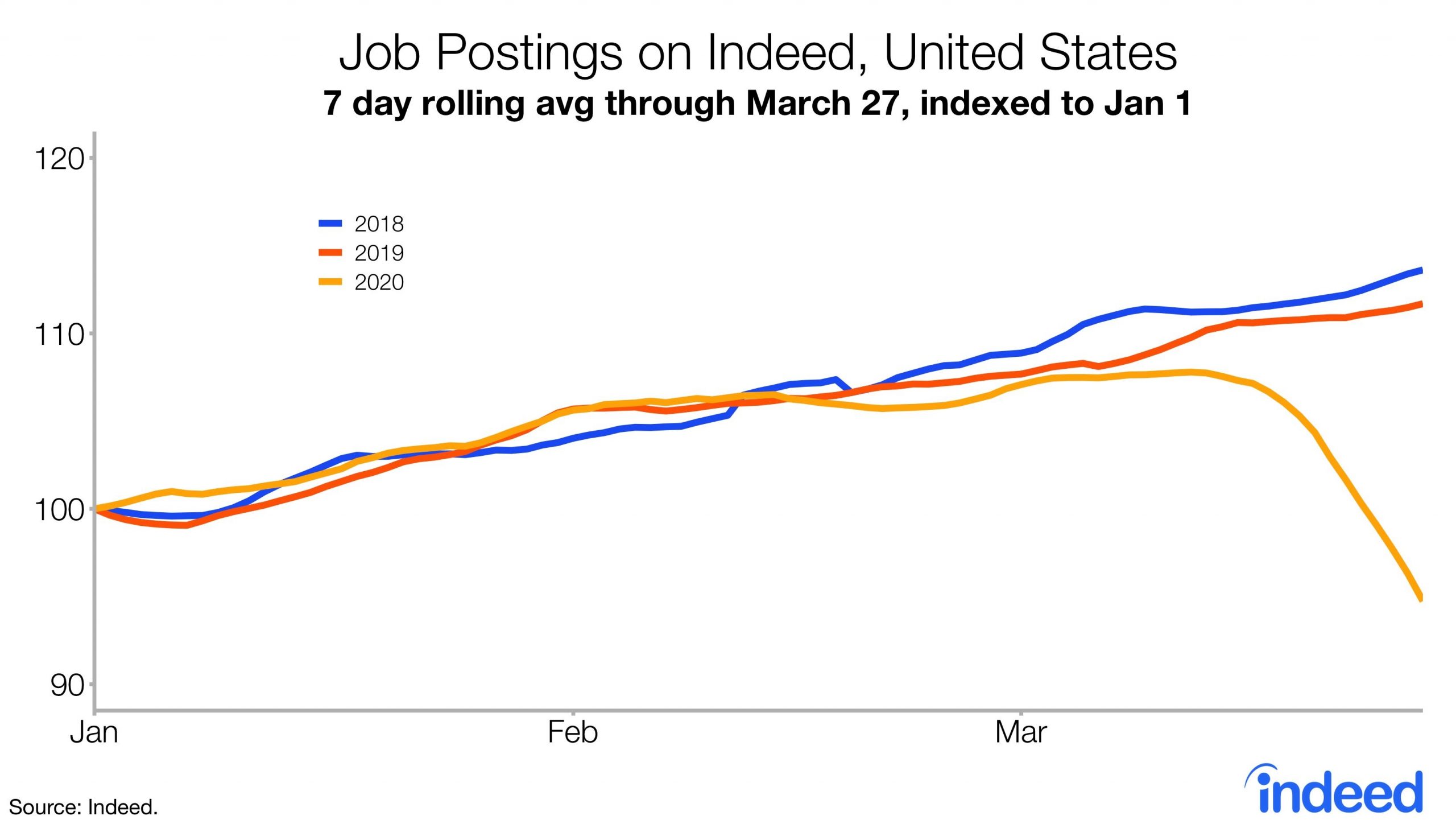

As you can see in the chart above, the 7 day rolling average index of job postings on Indeed has been falling precipitously. This decline started in the 2nd half of March which is around when the spike in jobless claims occurred. Job postings are down 15% and hospitality/tourism postings are down 58% from last year’s trend.

Consumer Confidence Is Diving With The Labor Market

Consumer confidence is obviously swooning. There is little reason to be optimistic as job losses mount and the stock market is falling. Even if you have money, it’s difficult to spend it. It wouldn't be surprising if the consumer sentiment indexes hit record lows. They weren’t around during the Great Depression. That’s not to say we won’t see a quick rebound in sentiment.

Even if it takes a few months for the economy to recover, the stock market can provide optimism. Plus, as soon as the shutdowns end, there should be a burst of confidence as the worst will be over. We're anticipating the shutdowns starting to end in May.

Even though today Virginia ordered a stay home action until June 10th. It’ll be tough to justify that draconian order when the number of new cases starts to fall.

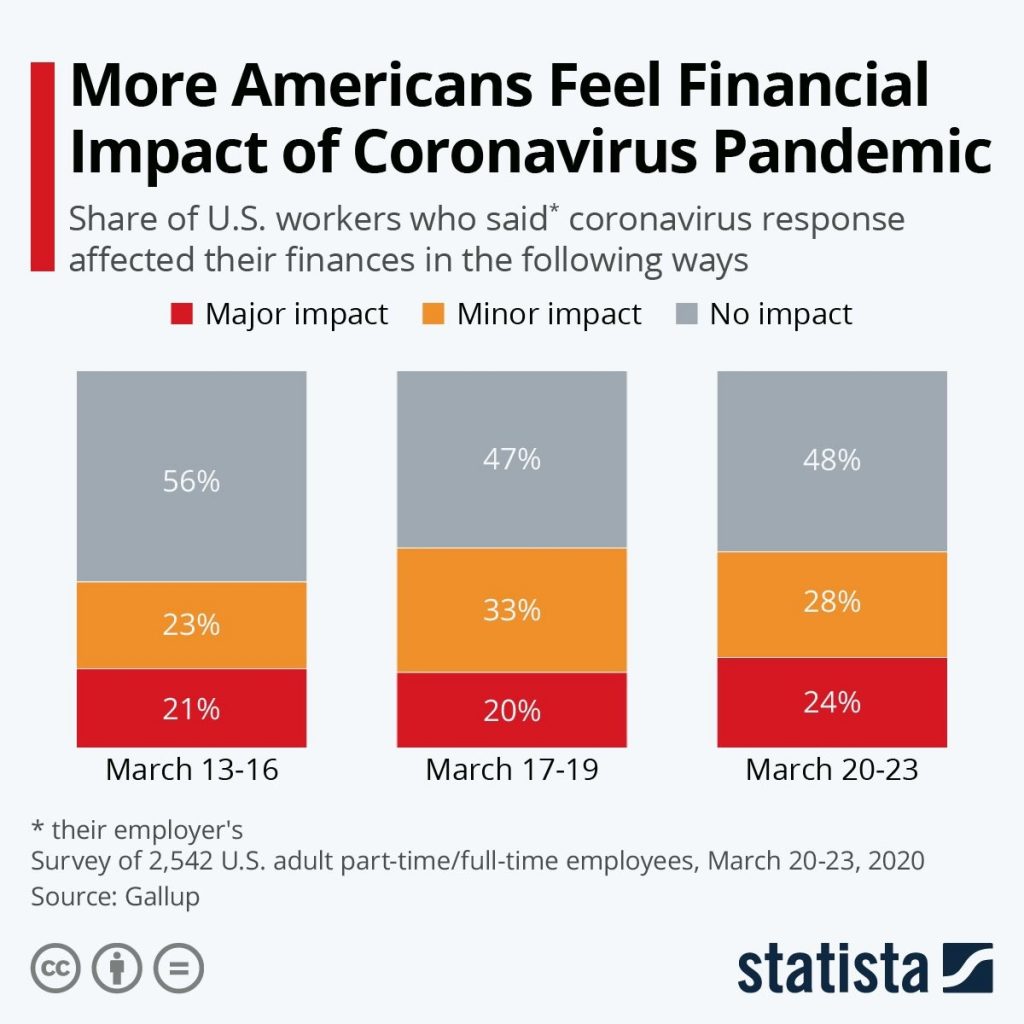

As you can see from the chart above, the impact on consumers’ finances has grown in the past couple of weeks. From March 13-16 to March 17-19, the percentage of workers who said the coronavirus response had a minor impact on their finances rose 10 points to 33%. From March 17-19 to March 20-23, the percentage of workers who said the coronavirus response had a major impact on their finances rose 4 points to 24%.

Obviously, the trend makes sense, but it's actually surprising that 48% still said it had no impact. That must be because the shutdowns were limited to about half of the population as of last week. Surely, if this question was asked again it would show the virus impacted more people. I’d guess that over 75% have seen some impact.

Even with unemployment insurance, there will be an impact. Unemployment insurance played a big role in preventing an outright depression (assuming we avoid one).

Capex Disaster

It’s no surprise capex plans are being pulled back with the energy sector having the most plans cut. You can see the unrelenting weakness in the March Dallas Fed Manufacturing report. Production index fell from 16.4 to -35.3. And the general activity index fell from 1.2 to -70 which badly missed the lowest estimate which was -32. Current capex index fell from 6.9 to -34.3.

6 month expectations index fell from 18 to -39.5. Expected capex index fell from 21.2 to -19.8. A machinery manufacturing firm stated, “Coronavirus is a game changer and hopefully will be relatively short in duration. Even though we are currently operating and have no supply issues, new activity is flat to nonexistent as of the middle of the month. However, we do think it will rebound when this is all over.”

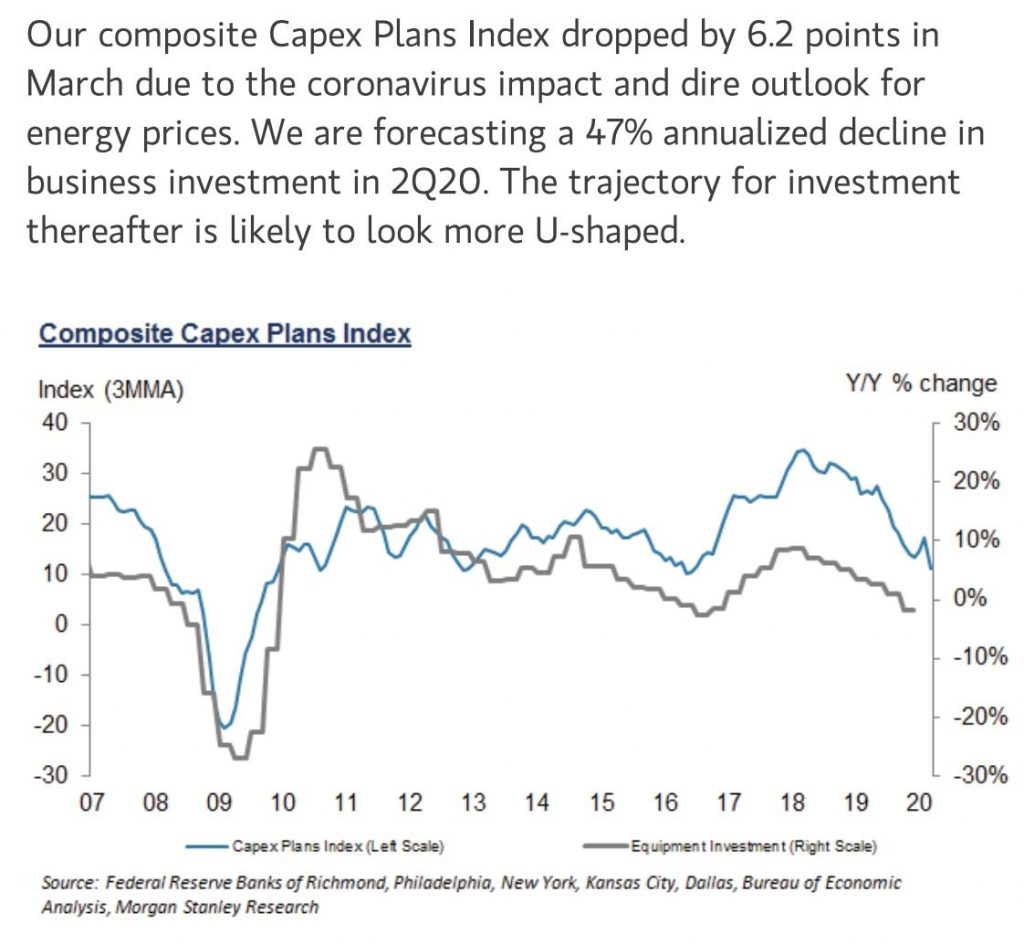

A drop in capex plans will be shown in the hard data in the next few months. You can see the cyclical decline in the capex plans index in the chart below. Equipment investment growth follows soon afterwards. Morgan Stanley used the capex plans data in the regional Fed reports to project a previously impossible to imagine 47% annualized decline in business investment with a U-shaped recovery to follow.

Downgrades Everywhere

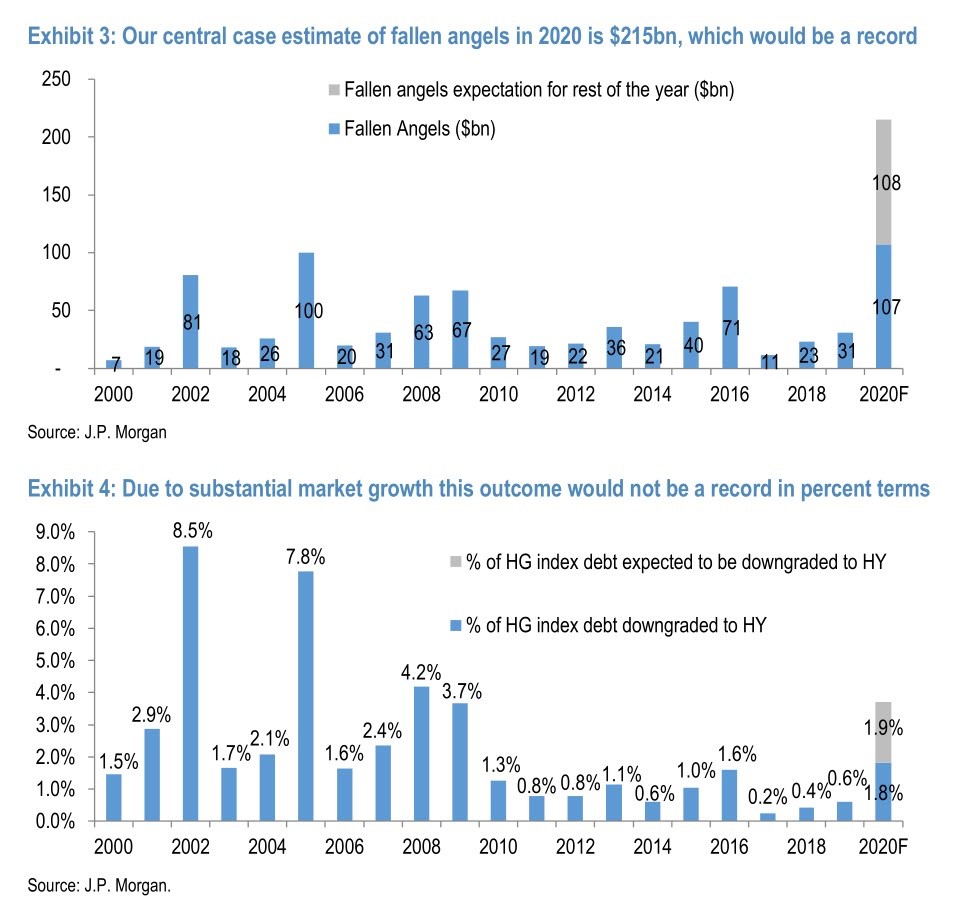

Let’s set the scene. Heading into this recession, there was a high percentage of corporate debt to GDP. There was a lot of BBB rated investment grade debt. There still was a lot of energy debt in the high yield market. A crash in the oil market and the corporate debt market was the worst case scenario for the economy. This led to the most downgrades since at least 2002.

As you can see in the chart below, in 2020 there has already been more debt from fallen angels than ever before. That’s set to double by the end of the year. To be clear, a fallen angel is a firm with investment grade debt that gets downgraded to junk which has much higher interest rates and default probabilities.

Good news is due to the huge growth in the corporate debt market, the nominal record hasn’t led to anywhere near a record percentage of fallen angels. It will be 3.7% if JP Morgan’s estimate is accurate. That would match the percentage in 2009.