Stocks Fall As Expected

It’s not surprising stocks fell on Friday. The market was very overbought and the airstrike that killed Soleimani gave investors an excuse to take profits. Also, the Fed Minutes were hawkish. Plus, the ISM manufacturing PMI missed estimates.

If you believe the ISM numbers, the stock market priced in a manufacturing recovery that hasn’t happened yet. Personally, I think the ISM has been a bit too negative in the past few months. It was way too positive in 2018. Even still, the stock market always reacts to the ISM PMI, not the Markit PMI.

Several commentators say the only good thing about the ISM PMI was that it came out on the day of a geopolitical event. That's not necessarily true. Markets can handle many events at once. It’s not as if the market can only focus on one thing at a time.

In fact, the main cause of the selloff might have been the PMI and not the geopolitical event. Stocks only fall on average 0.1% after airstrikes. Remember, stocks do well when the PMI is below 50, but if the market already priced in a recovery, it needs to happen. Stocks can’t rally indefinitely in a weak economy.

Specifics Of Friday’s Action

S&P 500 fell 0.71% on Friday. It wouldn’t be surprising if stocks fell that much without the airstrikes or the weak PMI. Mostly because tocks were extremely overbought. Airstrikes were an excuse to sell, as investors would have used anything as an excuse. Considering the news flow, it’s surprising stocks didn’t fall more.

Nasdaq fell 0.79% Let’s look at today’s action in terms of Apple. The stock rallied 55.35% from August 5th until January 3rd. It fell 0.97% on Friday. This decline wasn’t much. That being said, potentially none of the news events on Friday will affect the company. We’ll need to wait longer for its negative catalysts to play out.

Russell 2000 fell 0.35% which means it has now fallen in 5 of the past 6 trading sessions. It’s amazing how quickly indexes can go from winning streaks to losing streaks. That’s what will happen to the rest of the market later this winter.

VIX was up 1.55 to 14.02. The CNN fear and greed index only fell 4 points to 93 which is extreme greed. We need to see much more selling to bring the market to equilibrium. I don’t expect the geopolitical issue to be the catalyst for the decline, but I can’t rule it out. Good news is that President Trump stated, “We took action last night to stop a war. We did not take action to start a war.” There have been comments that this action will have a domino effect, but many are skeptical of that.

Even though oil rallied, the market’s action actually wasn’t good for most of my predictions for 2020. Energy sector actually fell 0.34%. It only marginally outperformed the market. Worst sectors were materials and financials which fell 1.62% and 1.1%. Utilities and real estate rose 0.11% and 0.81% as they were the only sectors in the green. In keeping with trades going against nexpectations, the 10 year yield fell 9 basis points to 1.79%. Weakness in manufacturing and a geopolitical event are a great combination for treasuries.

2 year yield fell 4 basis points which usually means the odds of a Fed rate cut increased. However, the odds of a hike increased because of the Fed Minutes. Odds of one cut increased from 3.3% to 41.2%. More hikes than expected is bearish for stocks.

Another Weak ISM PMI

Median forecast for the December ISM PMI was 49 and it came in at 47.2 which was down from 48.1 in November. This was the worst PMI since June 2009. Unless manufacturing production crumbles in December, I think it’s too negative to say the manufacturing sector is in the worst shape since the last recession.

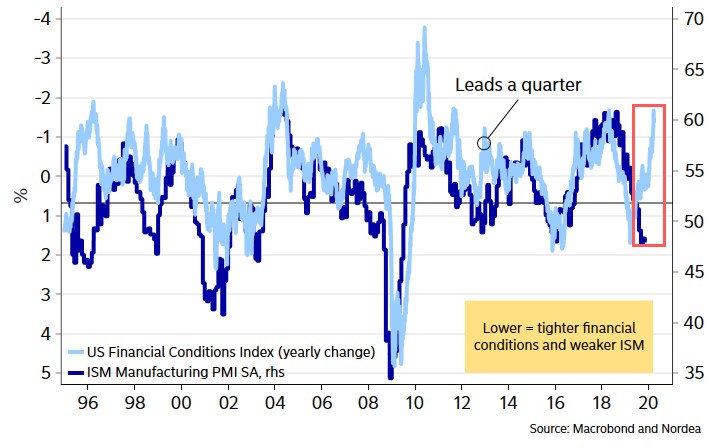

The stock market has already priced in a recovery, so if it doesn’t happen, stocks will crash. To be clear, we expect the recovery to happen, but it didn’t in December. We also expected a weak PMI after seeing the other reports on the sector. The chart below shows how the market priced in an improvement that hasn’t happened by comparing the financial conditions index’s yearly change with the ISM PMI.

PMI is consistent with 1.3% GDP growth which is probably below where Q4 growth will be if the December PCE report is solid. New orders index fell 0.4 to 46.8 and the production index fell 5.9 points to 43.2. Employment index fell 1.5 points to 45.1, but this sector doesn’t employ many workers anyway.

Prices index exploded up 5 points to 51.7 which supports previous points about inflation increasing. That’s consistent with the Markit PMI. Just like in the Dallas Fed report, there was only one mention of tariffs in the comment section of the ISM report. Weakness has mainly been because of cyclical factors, not the trade war. A fabricated metal products firm stated, "Anticipated large export orders did not materialize. As a result, expected U.S. production has decreased."

Conclusion

The stock market fell modestly on Friday which is pretty great. Especially when you consider that the Fed Minutes were hawkish, the ISM PMI missed estimates, the stock market had been very overbought, and there was a geopolitical event.

Anyone who thinks investors ignored the Fed, the overbought nature of the market, and the weak data is very wrong. The media might only be able to focus on one thing, but investors will focus on whatever matters.