December Retail Sales Should Be Great

Final December consumer sentiment reading showed consumers as very confident. Sentiment improved, not that it was weak in November. It’s interesting that the savings rate increased in November. Even though it was during the holiday shopping season and consumers were optimistic.

Last time spending was weak (December 2018), sentiment weakened in the following months. While spending growth wasn’t as weak in this past November, there was no evidence of any sort of slowdown continuing into December in the sentiment report. We're expecting very strong December retail sales and PCE growth.

Latest strong sales readings support the notion that sales shifted into December from November. This likely wasn’t captured fully in the seasonally adjusted November reports.

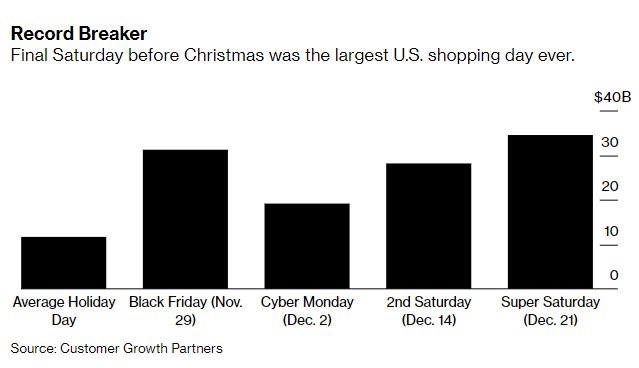

As you can see from the chart above, Super Saturday, which is the Saturday before Christmas, was the largest U.S. shopping day ever. Super Saturday’s sales were $34.4 billion which beat Black Friday’s sales by 10%. And Super Saturday was also the day before the first day of Hanukkah.

Sales on Black Friday were $31.2 billion. Next biggest days were December 14th which had $28.1 billion in sales and Cyber Monday which had $19.1 billion. Online sales have accounted for 58% of sales growth. Somehow online sales growth fell from October in the retail sales report. I think that report was too weak.

According to the National Retail Federation’s last survey 147.8 million people planned to take advantage of the sales on Super Saturday which was up from 134.3 million last year.

This holiday shopping season was short, so many consumers put off buying until the last minute. CEO of the National Retail Federation noted there was an "impressive turnout by procrastinators" expected. Super Saturday has been the biggest shopping day of the year since 2014.

While that makes this new record sound less impressive, as of early December fewer shoppers finished their holiday shopping by early December which supports the point that December will be great.

Last year 88% of consumers had started their shopping by early December and 58% were done. This year, 86% started and 52% were done. 2013, which was the last year there were 26 days in between Thanksgiving and Christmas, consumers had completed 50% of their shopping at this point.

This year, consumers expect to spend an average of $1,047.83, including purchases already made, which is 4% higher than last year. Remember, the November retail sales report only showed 3.3% growth.

December Consumer Sentiment

Consumer sentiment improved in December. Overall index was up from 96.8 to 99.3. That’s 1% yearly growth. This index can’t show much growth because it’s already very high. Current index was up from 11.6 to 115.5 and the expectations index was up from 87.3 to 88.9.

Impeachment had virtually no impact on this report as only 2% of consumers mentioned it. This is much different from the government shutdown which caused government workers to go without pay. It’s also pretty obvious that the President won’t be removed. PredictIt shows there is a 9% chance the Senate will convict President Trump.

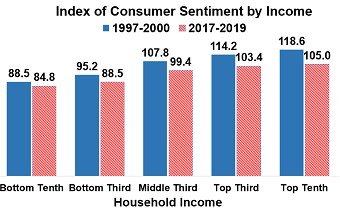

This report showed much more confidence gains among the upper third of income earners compared to the bottom 2/3rds. Top third had a 7.5% gain and the bottom 2/3rds had a gain of only 0.8%. Low income earners have had higher income growth than upper income earners. But the rich are enjoying the stock market’s amazing gains.

As you can see from the chart below, compared to the late 1990s, the bottom income group is doing relatively well versus the top tenth. Each tenth is lower than the late 1990s, but the difference between the top and bottom tenth is only 20.2, while it was 29.5 in the 1990s.

Prior to the big burst in confidence among upper income people in December, the difference was even smaller. All income groups should be happy about the low inflation rate of this cycle. Inflation is a big tax on the poor.

1 year inflation estimate was 2.3% which was the lowest rate since December 2016. 5 year expected inflation rate was 2.2% which was the lowest level ever. Question started being asked in the late 1970s.

Manufacturing Weakens In December

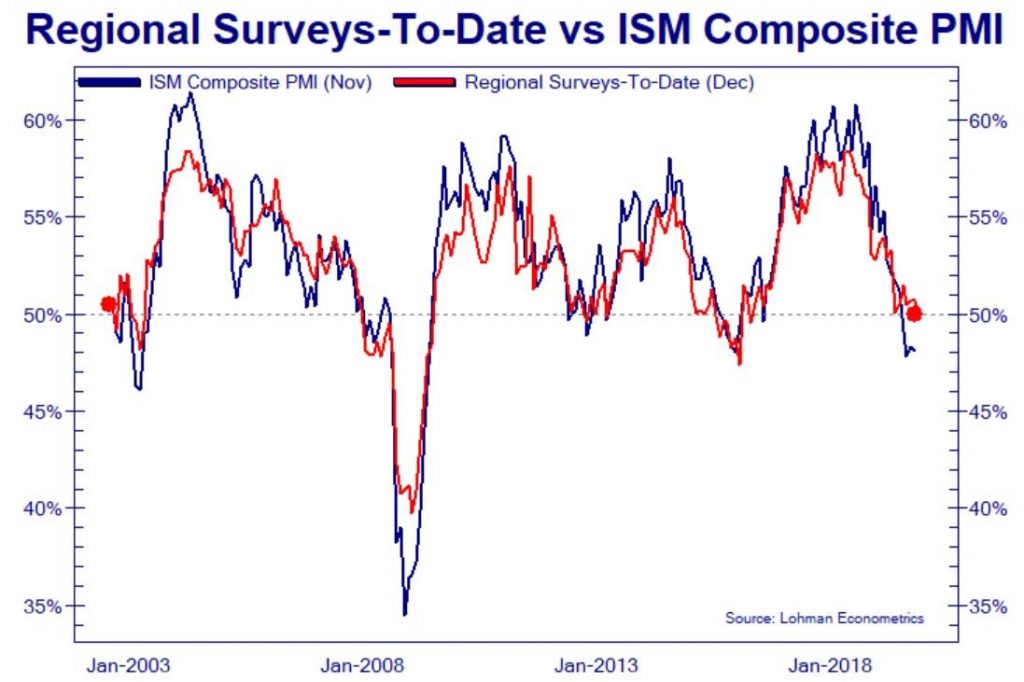

We’ve been optimistic about the possibility of a manufacturing recovery, but it might not happen in December. Markit flash PMI fell slightly and each of the first 3 regional Fed manufacturing indexes have fallen.

Third index to show a decline was the Kansas City Fed index which fell from -3 to -8. Now finally the average of the regional Fed indexes is predicting a below 50 ISM PMI as you can see from the chart below. It would be ironic to see the PMI rise above 50.

Remember, when the November PMI disappointed, stocks fell. That was one of the few negative catalyst stocks faced in the past few weeks.

The report was weak. Production index fell 2 points to -7, the volume of shipments index fell 13 points to -6. And the volume of new orders index fell 13 points to -16.

Expectations index was also weak. Composite fell 5 points to 10. Production index fell 13 points to 12. Volume of shipments index fell 15 points to 10. And the volume of new orders index fell 12 points to 16. Two of the 10 comments mentioned tariffs and 2 mentioned oil prices.

Conclusion

There’s more evidence the consumer is having a good holiday shopping season despite what the modestly weak November retail sales and PCE reports stated. Those reports weren’t terrible, but I’m anticipating a very strong season. Many think GDP growth will be above 2% because of this.

Manufacturing sector may have weakened in December. ISM reports have recently been too weak. If the PMI continues to stay too weak, it might fall. If the gap between the Markit PMI and the ISM PMI shrinks, it could increase.

First 3 manufacturing Fed indexes all fell, yet they still are showing an increase in the ISM PMI from November.