Consumer Credit Disappoints

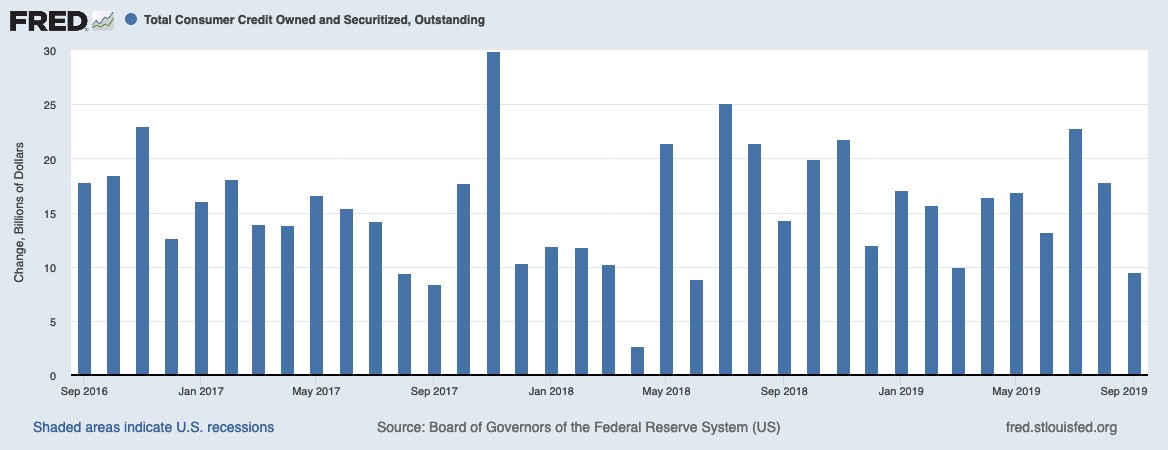

Monthly growth in consumer credit missed estimates sharply in September. In August, monthly growth was revised from $17.9 billion to $17.8 billion. As you can see in the chart below, there was only a $9.5 billion increase in consumer credit. It missed estimates for $15 billion, and missed the low end of the consensus range at $13 billion. And it was the lowest monthly growth since June 2018. Annualized growth fell from 5.2% to 2.8% which is the lowest reading since June 2018.

Results are less dramatic when you look at yearly growth as it fell from 3.8% to 3.5%. Changes in debt growth was all about the decline in student and auto loan growth. Specifically, revolving debt, which is credit card debt, fell $1.1 billion in September after falling $2.2 billion in August. 2019 has had 4 months where credit card debt has fallen.

Latest declines could be related to pairing down debt before the holiday shopping season. Quarterly average isn’t negative though. Last time it was negative was in Q2 2012. This revolving reading probably isn’t something to worry about yet.

Changes in non-revolving credit growth caused this sequential decline as revolving debt fell less than in August. In September, non-revolving debt growth was $10.6 billion after rising $20 billion in August. That was the smallest gain in 4 months. Yearly growth in non-revolving debt fell from 5.5% to 5.4%.

If you’re curious about the breakdown between student loans and auto loans, outstanding student loans were up from $1.61 trillion in Q2 to $1.64 trillion in Q3. Outstanding debt for vehicle loans increased from $1.17 trillion to $1.19 trillion. In other words, the sequential increase was near equal. Consumer credit report doesn’t track housing debt. Housing leverage has declined sharply this cycle.

Slight Improvement In Consumer Sentiment

University of Michigan consumer sentiment report improved very slightly in its preliminary November reading. It increased from 95.5 to 95.7 which missed estimates for 96. Since the report has been solid, this slight improvement should be considered decent news.

For those focused on the difference between current conditions and future expectations, the recessionary signal wasn’t as strong this time because expectations increased and current conditions worsened. Specifically, the current conditions index fell from 113.2 to 110.9 which was a 1.2% yearly decline.

Expectations index rose from 84.2 to 85 which was a 2.5% decline. As you can see, the sequential movements didn’t make up for the intermediate term trend as yearly growth in the current index was better.

Consumers were more confident in the economy, but slightly less confident in their own personal finances. This report obviously covers a different period than the consumer credit report, but it’s in line with a weakening opinion on personal finance. Maybe consumers know they will burst their budget on holiday shopping.

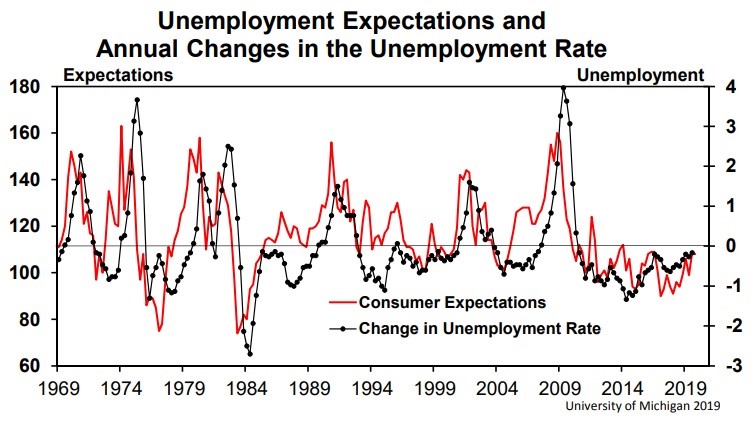

As you can see from the chart below, consumer expectations for the change in the unemployment rate are correlated with actual changes in the yearly growth in the unemployment rate. Right now, we have nothing to worry about which is in tune with the recent Fannie Mae housing report.

25% of consumers made negative references to tariffs which is down from 27% in October and 36% in September. Tariffs are slowly becoming less of an issue. If that rate goes down to near zero percent, there is plenty of room for the expectations index to rise further. I’m not sure how much tariffs are holding back retail sales.

Obviously, there isn’t a perfect causal relationship between confidence and actual spending. The savings rate has recently increased. That could be because consumers are hesitant because of the trade war and the cyclical weakness or because they are saving for the holiday shopping season.

It’s interesting because with tariffs becoming less of an issue and consumers having some pent-up savings, they might spend a lot this holiday season. That goes directly against the extremely low expectations for Q4 GDP growth.

Obviously, no one mentioned the GM strike in this report because it is over. Less than 2% mentioned the impeachment inquiry probably because it might not impact economic policy. The election is much more important than this inquiry. It is about who is president for the next 4 years not the next few months. Plus, President Trump is unlikely to be impeached by his own party. No Republicans voted for the resolution that sets up the rules for the public phase of the impeachment inquiry.

The Very Low Q4 GDP Estimates

It’s still very early in the quarter as most hard data reports from October haven’t even come out yet. That means the estimates for Q4 GDP growth won’t be that accurate. However, we should still follow them because they quickly summarize what we know so far about economic growth in the quarter. It’s interesting to see stocks rallying so much with such terrible GDP forecasts.

Forecasts might be too grim because consumer spending could be strong this holiday shopping season. Median of 8 estimates is for 1.5% growth. The average estimate is 1.7%.

You know the data has been terrible when the always bullish St. Louis Fed Nowcast is only expecting 1.87% growth. Atlanta Fed Nowcast is calling for 1% growth. In the update on November 8th, the estimate for the contribution of inventory investment improved from -0.59% to -0.53%. NY Fed Nowcast fell another 7 basis points to 0.73%. That’s extremely low.

For context, at this point last quarter, the estimate was for 1.58% and growth was 1.9%. If growth is about 3 tenths higher, it will only be 1%. That’s still very weak. Personally, I expect the hard data to boost the Nowcasts towards the mid 1% range.

Conclusion

Consumer credit increased less than expected, but I don’t view it as problematic. Consumer sentiment improved slightly. Estimates for Q4 GDP growth are extremely low. Yet stocks are rallying swiftly as they continue to make new records.