Stocks Inch Closer To Record High

S&P 500 rallied on Thursday, but didn’t reach a new high. There is very sharp resistance at the record high. S&P 500 was up 19 basis points to 3,010 which is the highest level since July 30th. It is now about 15 and a half points away from the record.

Normally, I’d say anything can cause stocks to break this level because we’ve seen small factors cause movements larger than this. However, it seems like even a positive catalyst might run into trouble with the market facing such sharp resistance. Even if a new high isn’t made this year, 2019 has been amazing.

Review Of Thursday’s Action

Nasdaq was up 0.81% and the Russell 2000 was down 17 basis points. VIX was down 0.3 to 13.71 as the past week has been very quiet compared to the first week of the month. CNN fear and greed index rose 2 points putting back into the greed category as it’s at 57. Best 2 sectors were tech and the utilities which rose 1.48% and 0.39%. Tech will be helped by Intel stock on Friday as it rallied 4.06% after hours on earnings.

As you can see from the chart below, as of mid day just 54% of the tech sector was above its 50 day moving average. The lowest was energy at 50%. Most sectors are overbought with the market near its record high. Tech should be struggling as its sector has had the worst earnings season due to the global cyclical slowdown.

Worst 2 sectors were healthcare and communication services which fell 0.6% and 0.73%. In the latest Iowa State poll Warren was in first at 28% and Mayor Pete was in second at 20%. If Mayor Pete becomes the nominee, it’s mildly positive for healthcare stocks as he’s more moderate than Warren and Sanders.

Fed funds futures market has been steady in the past few days as the October 30th rate cut has been locked in. There is a 93.5% chance of a rate cut in 5 days. Also, there is a 27.6% chance of one more cut in December. By April 2020, there is a 58.4% chance of at least 1 more cut. And, there will be somewhat of a stabilization after the next cut.

Let’s see if the Fed supports that with its statement and Powell’s presser. Difference between the 10 year yield and 2 year yield is 18 basis points as they are 1.76% and 1.58%. That’s still a very small difference. If the two separating meant a recession, that wouldn’t be enough.

Twitter Earnings Disaster

Twitter’s earnings report was one of the biggest disasters this quarter so far. Its stock fell 20.8% on this report on Thursday. EPS was 20 cents which missed estimates by 3 cents. Revenues were $823.7 million which missed estimates for $874 million. There were 145 million monetizable daily active users.

In Twitter’s explanation of this weak quarter, the firm stated, “In Q3 we discovered, and took steps to remediate bugs that primarily affected our legacy Mobile Application Promotion (MAP) product, impacting our ability to target ads and share data with measurement and ad partners. We believe that, in aggregate, these issues reduced year-over-year revenue growth by 3 or more points in Q3.”

As a big Twitter user, I noticed the ads becoming less targeted. Ad load also was ratcheted higher for people with a lot of followers. Users noticed more ads, although, I’m not sure how many followers you previously needed to not be shown many ads. Personally, I don’t see power users leaving because of ads.

If you are a celebrity that uses the service to promote products and connect with fans, you will keep using it. The service helps these people make money, so a few ads aren’t an issue. You’d think more ads would increases advertising revenue. However, cost per engagement fell 13%. Total ad engagements were up 23%. Total advertising revenue was $702 million which was up 8%, but way below estimates for $756 million.

There was also an issue with advertising data being shared even when users opted out. Unfortunately, all these problems caused the firm to report Q4 revenue guidance of $940 million to $1.01 billion which missed estimates for $1.06 billion. Even worse, the issue might bleed into 2020.

Amazon Misses EPS Sending Its Stock Lower

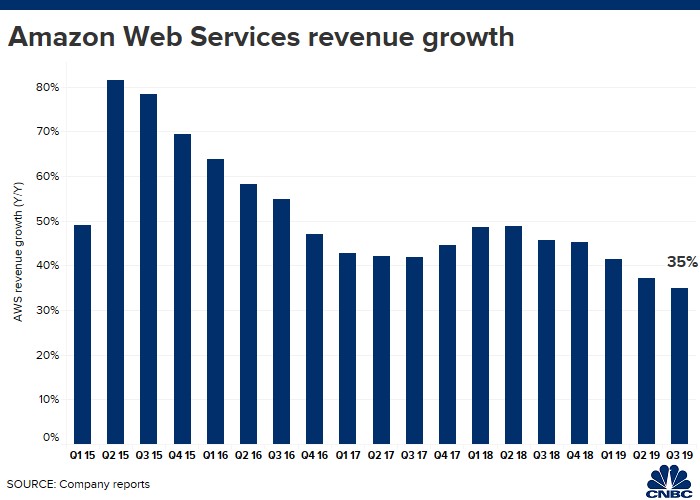

Amazon stock fell 6.73% after hours after the firm missed earnings estimates. It reported $4.23 in EPS which missed estimates for $4.62. It had revenues of $70 billion which beat estimates for $68.8 billion. That’s a 24% increase. One major problem for Amazon is AWS revenue is growing at a slower pace as you can see from the chart below.

Growth was 35% which was the slowest since Amazon starting reporting this number in 2015. It’s barely outperforming the rest of the company. Its revenue of $9 billion missed estimates by $100 million. It’s still the dominant cloud player, but it is losing share to Microsoft’s Azure. AWS’s operating income was only up 9% to $2.26 billion which missed estimates for $2.55 billion.

Amazon’s net income fell 26% as it hired many more workers and invested in adding more products that ship in 1 day with Prime. Amazon added 96,700 workers as it now employs an astounding 750,000. Amazon is the 2nd biggest employer in America to Wal-Mart.

And, Amazon has spent over $800 million in each of the past 2 quarters to expand free one day shipping with Prime. The firm plans to spend another $1.5 billion in Q4 to expand its warehouse footprint and product selection. It is taking shipping into its own hands which is hurting FedEx.

Also, the firm gave weak Q4 guidance which spooked investors since it includes the pivotal holiday shopping season. Specifically, the firm put forth revenue guidance of $80 billion to $86.5 billion. Meaning, the entire range is below the consensus of $87.4 billion. I’m not worried about this as the holiday shopping season should be great with consumers expressing optimism. A scary aspect is the very low income growth at AWS.