Stocks Increase Decently On Monday

S&P 500 seems to be attached to the 3,000 level. Another way of saying this is stocks can’t get to new a record high. On Monday, the S&P 500 was up 0.69%, putting it at 3,007. The index has gotten to within 1% of its record high on July 26th in 17 trading sessions since then.

That’s the most trading sessions near a record high since May 2017. In other words, it’s not a huge deal. Investors have been saying the 3 week negotiating period on trade could allow a good earnings season to bring the S&P 500 to a new record. Usually, stocks do well in Q4 and they usually do very well when they are up this much heading into the quarter.

There’s a bit less uncertainty now then there was at the start of the month. We know slightly more on trade, although, it’s still confusing. Some of earnings season has happened. 73% of the first 78 S&P 500 firms to report Q3 earnings have had positive EPS growth. 81% have beaten estimates. 63% have beaten sales estimates on 2.79% growth. It hasn’t been a great quarter because of the large decline in Q4 estimates. But we’re still seeing positive growth in what could be the growth trough of the year.

We have also seen how the Democratic debate went. Sanders seems to be losing steam and Mayor Pete is gaining ground. In the latest Iowa poll, Biden was up by 1% on Warren. Biden fell 6 points to 18% compared to the previous USA Today poll in late June. Warren gained 4 points to 17%. Pete gained 7 points to 13% and Sanders had no change at 9%. If Warren does well, Sanders will likely do poorly. If Biden does poorly, Mayor Pete will likely do well.

Review Of Monday’s Action

Nasdaq increased 0.91% and the Russell 2000 was up 0.95%. Many bears like to make a big deal about how the S&P 500 is just 0.63% from its record high and the Russell 2000 is 10.95% off its record. This doesn’t mean small companies are doing terribly. It shows the effect of the rate cuts on the small banks which are highly represented in the Russell 2000 index. I’ve discussed in previous articles the big decline in net interest margins at the large banks. Small banks are more levered to this because they don’t do IPOs or trading. They do traditional banking.

It might take until the market starts pricing in future hikes for the Russell 2000 to reach a new record high. There is currently a 90.9% chance of a cut in 8 days. Fed can’t talk publicly until then, so that rate cut is a lock. There is a 24.1% chance of a cut in December. Finally, after 3 straight cuts, we will see the Fed stand pat.

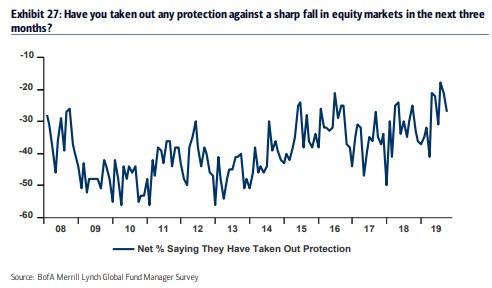

VIX fell 0.25 to 14. It might not get above 20 this month again as many of the uncertainties have cleared up. Biggest is still the trade war, but we might not get major news on that until early November. As you can see from the chart below, in the Merrill Lynch fund manager survey from October, about a net -30% of fund managers have taken protection out on a sharp fall in equities in the next 3 months. That’s down from where it was recently, but still historically high. To be clear, this is global stocks. Investors fear a global recession.

CNN fear and greed index rose 6 points on Monday to 56 which is greed. Stocks have done well recently. Stock performance will look amazing year over year in December if stocks don’t crater this fall like last year. Stocks haven’t done much since January 2018. Beauty is in the eye of the beholder. I see a sideways correction caused by the slowdown.

On Monday, the best 2 sectors were the financials and energy which rose 1.42% and 1.86%. This explains why the Russell 2000 outperformed the S&P 500. Only 2 down sectors were healthcare and materials which fell 7 and 35 basis points. Healthcare sector would like it if Mayor Pete were to rise more in the polls.

Gut Wrenching Netflix Reversal

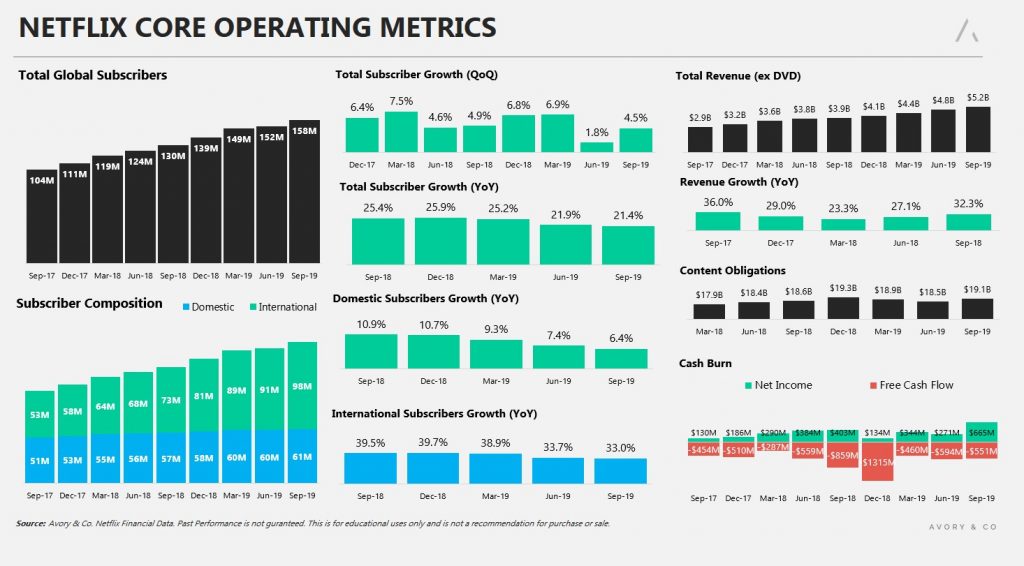

Netflix stock soared 8% after hours on Wednesday evening after reporting earnings. It only closed up 2.47% the next day. Even worse, it fell 6.15% on Friday. With its 1% gain on Monday, it is down 2.87% since before it reported earnings. EPS estimates were beaten sharply as EPS came in at $1.47 instead of $1.04. Revenue of $5.24 billion missed estimates by $10 million.

Domestic subscriber adds were 517,000 instead of 802,000. International subscriber adds were 6.26 million instead of 6.05 million. International is clearly the growth engine. As you can see from the chart below, yearly subscriber growth was 21.4% which was down from 21.9%. Free cash flow burn was a ridiculous $551 million. The firm expects to add 7.8 million subscribers in Q4.

Number 1 original movie streamed on Netflix in the past year was “Bird Box” which was viewed 80 million times. Number 2 was “Murder Mystery” at 73 million. The most popular original show was “Stranger Things” at 64 million. “Stranger Things” season 3 was released in July. There will be some downtime before the next season.

The firm isn’t worried about the new competition which is scary. It sees “modest headwinds.” It stated, “Many are focused on the ‘streaming wars,’ but we’ve been competing with streamers (Amazon, YouTube, Hulu) as well as linear TV for over a decade. Upcoming arrival of services like Disney+, Apple TV+, HBO Max, and Peacock is increased competition, but we are all small compared to linear TV. While the new competitors have some great titles (especially catalog titles), none have the variety, diversity and quality of new original programming that we are producing around the world.”

If I was an investor, I’d be nervous about this lackadaisical approach even if I thought Netflix would come out of this onslaught mostly unscathed. To be fair, this new competition is mostly priced in. It’s not a reason to sell the stock unless you see Netflix taking a big hit.