Stocks Fall Sharply On Disappointing ISM PMI

September ISM PMI was the weakest since June 2009. This sent stocks careening lower after they had initially rallied slightly because of the encouraging Markit PMI. It’s clear which PMI the market follows the closest. Markit PMI has double the sample size, but traders and algos don’t care.

This isn’t something new as the ISM report has always been the most followed. Only new aspect is the recent divergence. While the difference of a couple points in the PMI probably doesn’t change the intermediate term trend, if the PMI was 49.8 instead of 47.8, stocks wouldn’t have sold off.

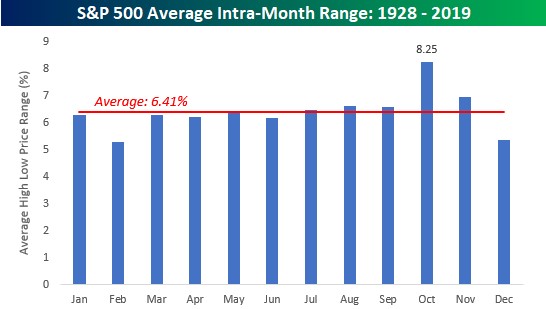

Volatile Start To October

Let’s look at Tuesday’s action first. As you can see from the chart below, since 1928, the intra month range in October is the largest out of any month by far. The month started off in tune with this wide range as the S&P 500 fell 1.23%. Nasdaq fell 1.13% and the Russell 2000 fell 1.97%.

Personally, I don’t see this being the start of a big decline. I think the ISM report is a little more bearish than reality. But I also think the manufacturing sector is in a slowdown. It has been in one for a few months, so this shouldn’t be new.

Size of the decline in the index is a bit surprising, but it could be wrong. Also, the trade war caused much of the weakness and there will be negotiations in 8 days. Stocks should only fall into a correction if the meetings don’t go well.

VIX rose 2.32 points to 18.56. I predicted the VIX would hit 20 this month. This prediction almost came true in the first day of the month. That was quick. I didn’t expect such volatility until the middle of the month.

Latest update on the Democratic primary election, which could cause some volatility later this month, is that Biden is dominating in South Carolina.The latest poll showed him up by 11 points.

Also, Warren is up by 1 point in New Hampshire. Biden, Warren, and Sanders will be the center of the debate on the 15th. CNN fear and greed index fell 6 points to 48 which is neutral. It can easily fall further as the trade negotiations and Democratic debate get closer.

Very Strong Dollar

Every sector fell on Tuesday because it was a washout. It’s no surprise industrials, materials, and energy fell sharply because of the weak ISM PMI. They were down 2.4%, 2.3%, and 2.3%. Financials were down 2.08% because treasury yields fell. It was a risk off day as the dollar also rallied.

As you can see from the chart below, the dollar index is the strongest since May 2017. This is right in line with weak oil prices as commodities are priced in dollars. Everything fits together like a puzzle.

Banks like the slight steeping in the curve as the 10 year yield is at 1.66% which is 11 basis points above the 2 year yield. Fed’s next rate cut will steepen the curve which might not be a good thing because the curve steepens in recessions. Currently, there is a 63.1% chance of a cut in October and a 78.3% chance of a cut by the end of the year. Basically, the next cut moved closer by about 6 weeks.

Labor reports will play a big role in whether the Fed cuts later this week. I’m getting nervous about the BLS report because of the latest trend in the data. And also because of the increased pessimism about the labor market expressed in the Conference Board index.

Consensus is for 145,000 jobs created. I wouldn’t be surprised if less than 100,000 jobs are added. We’ll get a better idea of how the number will come in when the ADP private sector jobs report comes out on Wednesday.

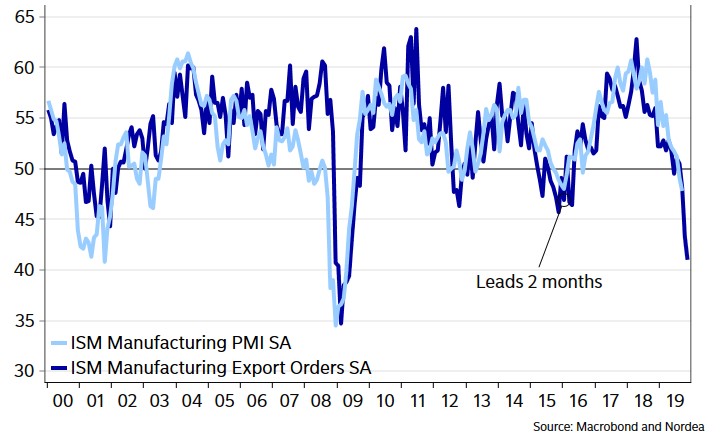

Export Orders Index Plummets

Let's finish up my review of the ISM manufacturing report which caused stocks to fall on Tuesday. Difference between the ISM PMI and the Markit PMI report may have been partially driven by inventories. ISM inventories index fell 3 points to 46.9. Inventories have a bigger weighting in the ISM report than the Markit PMI.

As you can see from the chart below, the new export orders index has been plummeting probably because of the trade war. It fell 2.3 points to 41. This is the worst reading since the financial crisis. Since 2000, it has only been lower in 2008 and 2009. Either this index is mistaken or the overall PMI is about to plummet because historically export orders lead the overall index by 2 months.

In this report, 3 sectors were expanding and 15 were contracting which leads us with a net -12. Even though this report missed the low end of the consensus range, it’s consistent with 1.5% GDP growth which is only slightly below most estimates.

Consensus is for 1.9% GDP growth. This report caused Merrill Lynch to lower its estimate to 1.8% growth. Prices paid index rose 3.7 points to 49.7. It’s very rare to see the PMI in contraction while the prices paid index increases this sharply.

These quotes are important here because we must know why firms became so pessimistic. 3 of the 10 quotes mentioned the trade war or tariffs. An electrical equipment, appliances, and components firm stated, “Economy seems to be softening. The tariffs have caused much confusion in the industry.”

This is in line with the 1.3% decline in monthly orders for this exact segment in August. That was the weakest growth since November 2018. Based on the ISM PMI and this quote. It seems like orders continued to weaken in September.

A chemical products firm stated, “Continued softening in the global automotive market. Trade-war impacts also have localized effects, particularly in select export markets. Seeing warehouses filling again after what appeared to be a short reduction of demand.” That’s consistent with the 0.8% monthly decline in motor vehicle and parts orders.