Slightly Improved Consumer Confidence

Shocking August consumer confidence reading which caused everyone to discuss the impact of tariffs was updated on Friday. It showed a modest improvement. At first, the University of Michigan index seemed important because August retail sales growth was strong.

With the weakness in real consumption growth in the PCE report, many investors changed their minds. Personally, I’m now focused on what the confidence index shows. Preliminary September readings showed an improvement after the gap down in August. A final reading improved further.

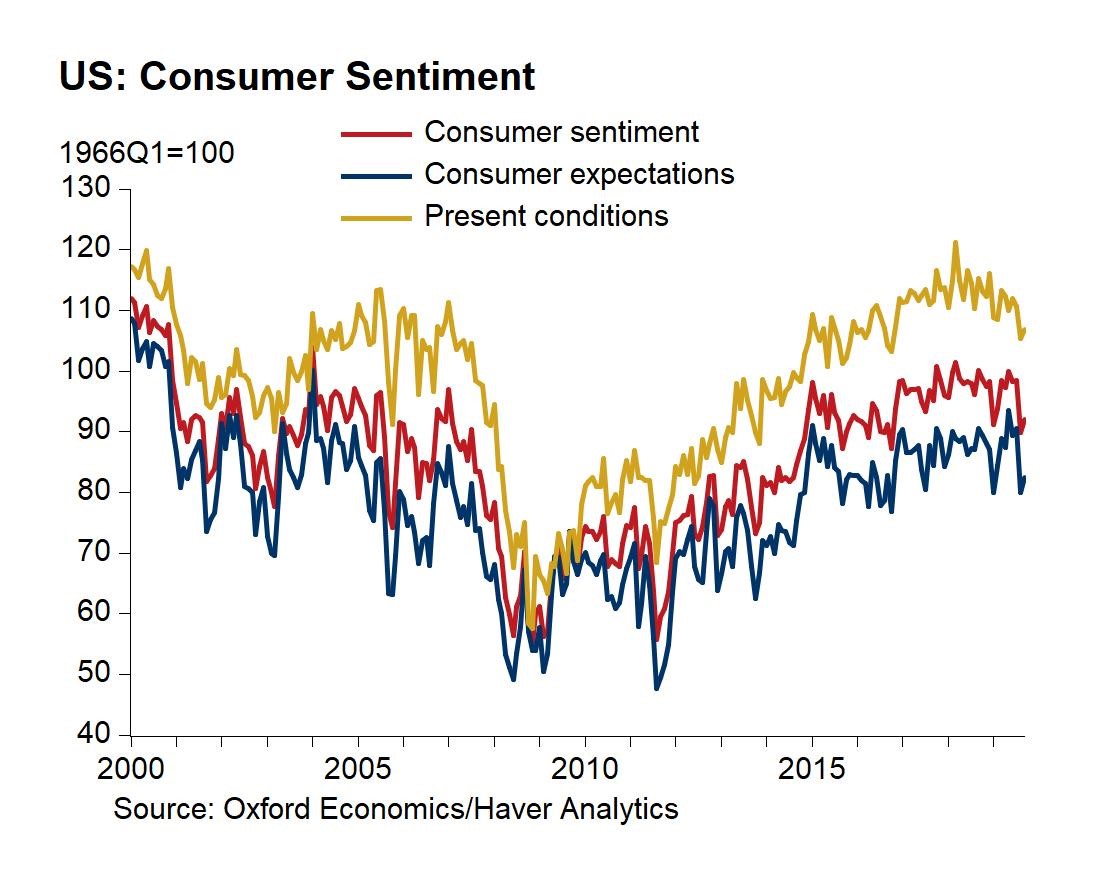

Specifically, from August the index improved from 89.8 to 93.2 which was a 3.8% monthly increase and a 6.9% yearly decline. As you can see from the chart below, the current index improved from 105.3 to 108.5 and the expectations index improved from 79.9 to 83.4. Note that each part of this index and the overall reading are far below last month.

This is like a stock that gapped down sharply and then recovered some of its losses the next day. It doesn’t mean consumers are very confident. It’d be helpful if a trade deal is made. Conference Board consumer confidence index was very strong in August and weakened in September. Let’s see which index real consumption growth follows in September.

Conference Board index focused on the weakness in the labor market and the University of Michigan index focused on the references to the trade war. About 35% of consumers gave spontaneous unfavorable references to tariffs which is near the highest level since early 2018 (when the mentions started). I always focus on what consumers are saying about the labor market because that’s what they are the most knowledgeable on.

On the one hand, payrolls growth has been falling all year. On the other hand, jobless claims are very low. There isn’t great demand growth, but demand isn’t falling enough to cause a burst in layoffs. I think this slowdown is on the precipice of causing layoffs and becoming a modest recession. It doesn't seem like it will get to that point. This is like 2016 where it looked like a recession was likely and then it didn’t happen. Obviously, it's good to closely follow the economic reports and Q3 earnings season. Let’s see where Q4 EPS estimates head (down slightly or down sharply).

Last September Regional Fed Index

September Dallas Fed manufacturing index was the last of the 5 regional Fed manufacturing reports to be released. Its production index fell from 17.9 to 13.9 and its general activity index fell from 2.7 to 1.5 which beat estimates for 1. As you can see from the chart below, the average of the regional Fed indexes signals more weakness for the ISM PMI than it did in August. However, since the ISM PMI was below the average last month, the average calls for a slight increase.

Personally, I expect the ISM PMI to rise slightly above 50. My estimate range is from 49.5 to 50.5. Consensus estimate is 50 and the range is from 49.1 to 52. If the PMI falls from its reading of 49.1, it will be bearish. If it rises slightly, there probably won’t be a market reaction. Soft data gives no indication of a deep manufacturing recession, but it also doesn’t suggest we are out of the woods. That’s similar to the August industrial production report which showed continued weakness, but results that beat estimates.

Let’s look at the details of the Dallas Fed manufacturing index which showed more of the same i.e. modest weakness. New orders index fell 2.2 points to 7.1, but the growth rate of orders index rose 2.6 points to 4.4. Most categories didn’t show much change as this was a mixed bag.

Biggest gains were in the prices paid for raw materials and employment indexes which were up 10.5 and 13.3 points to 20.3 and 18.8. It’s surprising to see employment improve because generally firms don’t hire more workers when production is in a slowdown. Recent weakness in oil prices could lead to weakness in prices paid and can be bad for manufacturing in the Dallas Fed district since this region has a lot of fracking activity.

Company outlook index was up 2.4 points to 7.4 and the outlook uncertainty index fell 5.3 to 13.3. You’d think uncertainty would be high because of the trade war and incoming new tariffs on October 15th. Now let’s review the expectations category. It showed similarly mixed results as the production index was up 0.4 to 25.4 and the shipments index fell 7.8 points to 18.4.

Compared to the other expectations categories in the regional Fed indexes, this one wasn’t bad. Growth rate of orders, new orders, and capex indexes were up 4, 0.2, and 6 points to 18.8, 23.9, and 23.3. That being said, the general business activity expectations index fell 8.2 points to -6.8.

Looking through the comments section in this report, 6 firms mentioned tariffs as the trade war continues to be a big issue for the manufacturing sector. A nonmetallic mineral product firm stated, “Uncertainty due to tariffs is a big problem for costing—selling prices—planning. Do we find vendors in alternate countries from China (which may not be possible in the 12–24-month short term)? Do we redesign products, and expand our factory to make some products here? It is very difficult to plan.” This gives you insight into how the trade war is creating uncertainty for firms.

Conclusion

Consumer confidence improved slightly, but it’s still in the same area it was in August. That index has gone from great to good. It needs a trade deal to spike higher again. Dallas Fed manufacturing index showed more of the same results we’ve seen in the other manufacturing regional Fed reports. Manufacturing sector is in a modest slowdown. There could be a cyclical upturn next year if there’s a trade deal and global monetary policy stimulus is effective.