Stocks End The Week Lower

Stocks fell on Friday because the White House is considering blocking all US investments in China. To me, this seems like a lot of speculation and not much actual news. This report stated the discussion is in its preliminary stages and nothing has been decided. There also isn’t a time frame for implementation. A goal would be to protect US investors from the lack of Chinese regulations. But investors sold stocks on Friday because they saw it as a negative action within the context of the trade war.

It’s possible the White House leaked this story to talk tough on China right before the negotiations. Investors should not be concerned with this story. Instead, they should be interested to see how the negotiations go on the 10th and the 11th. I’m very confident they will occur. Both sides have the incentive talk. Everyone knows markets will plummet if they don’t. It’s possible the negotiations get further than they did this spring.

Specifics Of Tuesday’s Action

S&P 500 fell 0.53%, Nasdaq fell 1.13%, and Russell 2000 fell 0.84%. There has been hardly any movement in equities for a few weeks. Since September 5th, S&P 500 has fallen just 14 points. At the high end of that range it was up about 1% and now it’s down less than 1%. There has been nothing doing as investors wait for the Democratic debate, earnings season, and the trade talks in October. Also, there weren’t any new polls released on Friday.

VIX was up 1.15 to 17.22. It’s relatively high considering how little movement in equities there has been since September 5th. Investors see it falling in the near term. But there are certainly a few potential negative catalysts for the market in October. CNN fear and greed index fell 5 points to 52 which is almost perfectly neutral.

Another potential reason stocks fell is because of the weak economic data. Consumption growth missed estimates and core capital goods orders were disappointing. This might explain the sector by sector action as consumer discretionary stocks fell 0.37% and industrials fell 0.41%.

Worst sector was tech which fell 1.28%. That’s the sector most impacted by the trade war. The only sector that was up was the financials as it increased 0.24%. Financials were led by Wells Fargo which was up 3.77% because it finally chose a CEO. It picked Charles Scharf who is the president and chief executive of Bank of New York Mellon. The fact that the company hadn’t had a CEO since March certainly weighed on its stock.

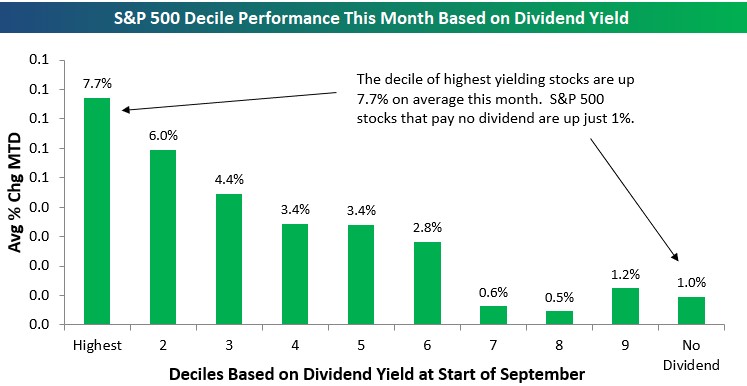

As you can see in the chart below, the higher the yield a stock had, the better performance it has had this month. Stocks with no dividend are up 1% and stocks with the highest decile dividend yields are up 7.7%. That’s somewhat confusing because treasury yields have actually risen this month. One of the highest yielding stocks, Altria, has had a terrible month as it is down 8.3%. Mostly due to worries about vaping regulations and its failed attempt at a merger with Phillip Morris.

There wasn’t much action in the treasury market considering the PCE inflation report was released. That’s probably because it came in close to expectations. Clearly, investors aren’t worried about a burst in inflation or economic growth. 10 year yield fell 1 basis point to just 1.68%. 2 year yield fell 2 basis points to 1.63% which signals rate cut odds increased. Latest odds show a 69.3% chance of a cut this year.

Weak Capital Goods Orders

Headline new orders growth beat estimates in August, but weakness in core capital goods orders sullied this report. Specifically, new orders were up 0.2% monthly which is very strong since the comp was 2% in July. Monthly growth in August beat expectations for a decline of 1.2%.

Excluding transportation growth was also strong as it was 0.5% which beat estimates for 0.2%. Growth in July was -0.5%. Transportation drove order growth in July. That wasn’t the case in August as commercial aircraft orders were down 17.1% and motor vehicle and parts orders fell 0.8%. On a yearly basis, the grounding of the 737 Max caused commercial orders to fall 37.3%. At least motor vehicle and parts orders were up 5.9%.

Core capital goods orders were weak. July’s monthly growth rate was revised down from 0.4% to 0%. Even with this sharp negative revision, August’s growth still missed estimates for 0%, coming it at -0.2%. Yearly, seasonally adjusted non-defense capital goods excluding aircraft orders growth was negative for both months. Growth was -0.8% in July and -0.3% in August. That’s nowhere near the trough of -8.9% growth in 2015, but it’s still weak.

Growth will turn positive in September because the comp goes from 7.6% to 1.7%. As the chart below shows, this latest weakness in core shipments is in line with the weakness in non-residential business investment. It’s not a good combination for consumption growth and business investment growth to be weak.

Let’s look at some of the weak numbers in this report. Orders for transportation fell 0.4% after rising 7.2%. Shipments of core capital goods were up 0.4%, but that is offset by a 0.6% decline in July. Orders for electrical equipment, appliances, and components fell 1.3%. Unfilled orders were up 0.1%, inventories were up 0.3%, and total shipments were up 0.1%.

Conclusion

Friday wasn’t a great day for economic data as there was weakness in core durable goods orders growth and consumption growth. This ruins optimism for the quarter based on the recent housing data. I can’t react to reports of something the White House just started considering.

Obviously, if the negotiations go well in October any negative action towards China won’t be enacted. If there is a trade deal, tech stocks will outperform. The economy won’t be out of the woods completely if there is a trade deal as the cyclical weakness wasn’t caused by the trade war. Tariffs just made the slowdown worse.