Slight Decline On Thursday: Peloton IPOs

Stocks declined slightly on Thursday, although, I think they would have risen if the news about the timing of the U.S. China talks had come out before the close. Specifically, the S&P 500 fell 0.24% which put it near where it has been for most of the month. One of the biggest news events of the day was the $1.16 billion IPO of Peloton which sells exercise bikes with touch screens.

The stock opened $2 below its IPO price of $29. It sold off throughout the day as it closed at $25.76. On the one hand, this doesn’t signal problems with the market because this firm’s fundamentals are suspect. On the other hand, this is yet another example of a company with weak fundamentals going public at a high valuation.

VCs are starved for firms with business plans that might lead to profitable growth. It says a lot about the economy’s competitive landscape that new firms with great potential aren’t going public.

More Bears Than Bulls?

Nasdaq fell 0.58% and the Russell 2000 fell 1.12%. VIX was up 0.69 to 19.07. It has been in the mid to high teens for weeks now. The market hasn’t broken out to a euphoric high where volatility truly dies, but there hasn’t been a real correction. The 5% correction in August wasn’t a big deal.

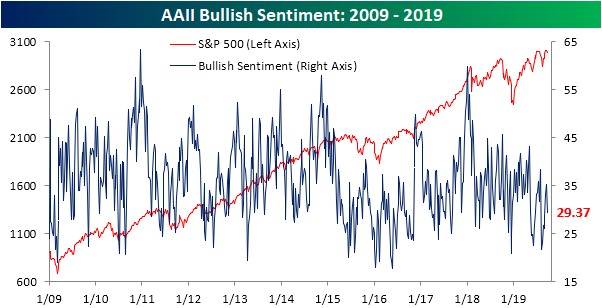

CNN fear and greed index fell 2 points to 57 which is on the low end of greed. Even though the CNN index suggests the market is seeing greed and the S&P 500 is near its record high, the AAII investor sentiment index shows investors are skittish. That’s great news for the bulls.

As you can see from the chart below, the survey shows just 29.4% of investors are bullish which is below the 33.3% that are bearish. In the week of September 25th, the percentage of bulls fell 6% and the percentage of bears rose 5.4%. You’d think the market was in a correction with numbers like that. The trade war, presidential election, and yield curve inversion have really scared people.

China Meetings Are On October 10th

We always knew the meetings between America and China were going to occur in early October, but we didn’t know when. Now we do. Talks will resume October 10-11th in Washington D.C. That’s just a few days before the next round of tariffs will be implemented. If the meetings go well, the tariffs will be delayed further.

Chinese Vice Premier Liu He will be representing China’s delegation. He came to America this spring and promised China would buy more American soybeans, but he was stripped of the title “special envoy” when Chinese leaders didn’t agree with is concessions. It’s good a negotiator is coming who is willing to give a little. However, it would be unfortunate if he made a grand deal and then Chinese leaders balked at it, putting the negotiations back at square one.

Many investors think we could see stocks rally modestly in anticipation of this meeting which is in about 8 trading days. Personally, I expect it to push the ball downfield to use a football analogy. There, obviously, won’t be a deal made. Hope is the 2 sides agree to meet again this fall.

Sector Analysis

On Thursday, the biggest winners were real estate and consumer staples as they increased 0.9% and 0.5%. It was a risk off day even though stocks didn’t fall much. Headlines claimed stocks fell because of worries about the impeachment process. Is this the new excuse for every movement in stocks?

It used to be stocks rose and fell depending on how traders felt about the trade talks. More movement than reality was ascribed to the negotiations. Obviously, they do impact stocks, but they don’t control every day’s action. Biggest losers were communication services and energy which fell 0.79% and 1.33%.

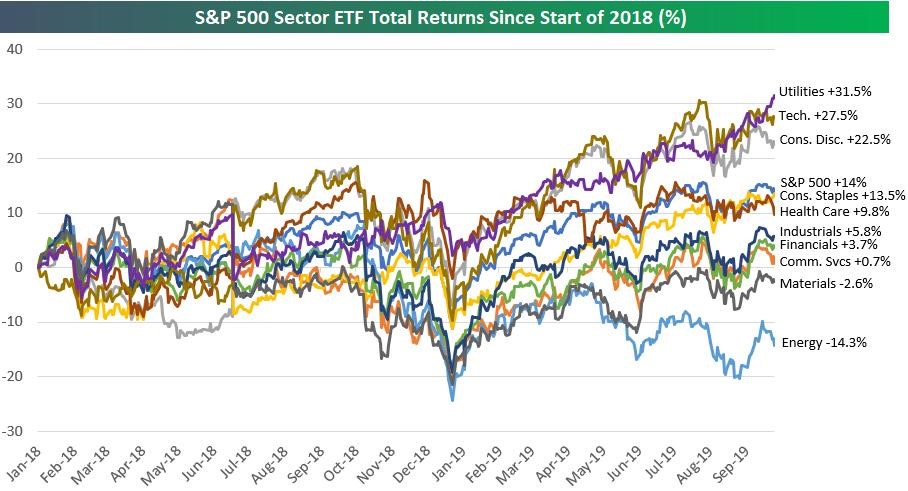

As you can see from the chart below, energy has been the worst sector since the start of last year and communication services has been the 3rd worst. The former is down 14.3% and the latter is up 0.7%. Healthcare sector, which is the largest one, fell 0.63% on Thursday and has 9.8% total returns since the start of 2018.

The Pricing In Of Elizabeth Warren

We never know how much something is priced in. Sometimes it seems like a catalyst is priced in and then it happens and markets still react to it. Obviously, the market hasn’t full priced in Warren becoming president since we are over a year away from the election. However, it is certainly starting to be on the market’s radar.

As you can see from the chart below, as Warren’s odds of being the Democratic nominee have increased, United Health Group’s stock has cratered. It has a lot of room to fall if she becomes the nominee.

Latest national poll shows Biden is leading by 11 points over Warren. However, the same pollster showed Warren 4 points lower and Biden 4 points higher in late August. That’s a big shift in 1 month. If the same shift happens again by the end of October, Warren will be within the margin of error.

Biden is now up 7.3 points in the average of the 8 most recent polls. October 15th and 16th debates will take place in Ohio. The lineup of which candidates are debating on which night hasn’t been released yet. Deadline to make the debate is October 1st which means the details will likely come out soon afterwards.

Conclusion

Mid-October is now very important as the Democratic debates with be on the 15th and 16th, the meetings with China in D.C. will be on the 10th and 11th, and earnings season is starting.

At least the Fed meeting is at the end of the month as it’s on the 30th. I can’t rate the order of their importance because it depends how they play out. For example, if the debates don’t affect the polls, then they won’t matter.