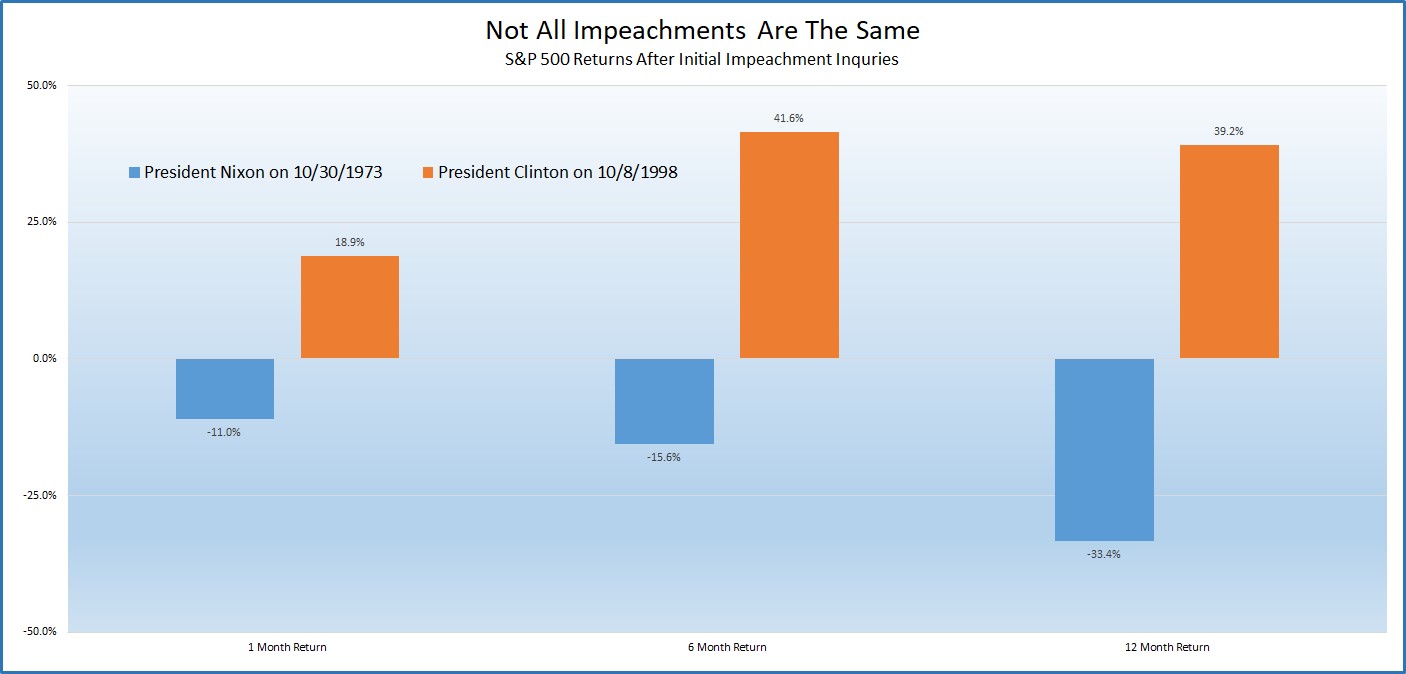

Stocks Regain Impeachment Inquiry Losses

It’s no surprise stocks rallied on Wednesday, regaining their impeachment related losses. The market doesn’t see President Trump being removed from office, so it isn’t selling off. As you can see from the table below, the returns after Nixon and Clinton were impeached were much different.

You can either say an impeachment that leads to the President leaving office causes stocks to fall or that stocks trade on fundamentals not politics. I’ll go with the latter. If Trump is removed, stocks will probably fall, but I don’t like to speculate on unlikely political events.

Specifics Of Wednesday’s Trading Session

The market is back at the level it had been stuck at for 13 days prior to Tuesday’s decline. There is little reason for stocks to rally or decline until we get more information on earnings season and the October trade deal meetings. Specifically, the S&P 500 rallied 0.62%. It’s back near the 3,000 level which it has been glued to.

America reached an initial trade agreement with Japan. This continues the trend of America and China striking deals with countries other than each other. President Trump also stated a trade deal with China could come sooner than we think. Yet many investors will react when and if we see the negotiations in October going well. As you can see from the chart below, the President’s approval rating on trade is in the negatives. This is the incentive he has to make a deal a few months before the November 2020 election.

Nasdaq rose 1.05% and the Russell 2000 rose 1.11%. VIX fell 1.09 to 15.96 just as expected. CNN fear and greed index is back where it was earlier this week as it increased 5 points to 59. Even though stocks are near their record high, I wouldn’t say they are very overbought because they haven’t done much in the past 2 weeks. S&P 500 is up about 6 points since the close on September 6th.

Wednesday was basically a reversal of Tuesday as the utilities fell 3 basis points and communication services rose 1.12%. Biggest loser was healthcare which fell 0.48%. And the biggest winner was technology which rose 1.24%. Tech loves when the odds of a trade deal increase. Healthcare doesn’t like when a leftist Democrat gains in the polls.

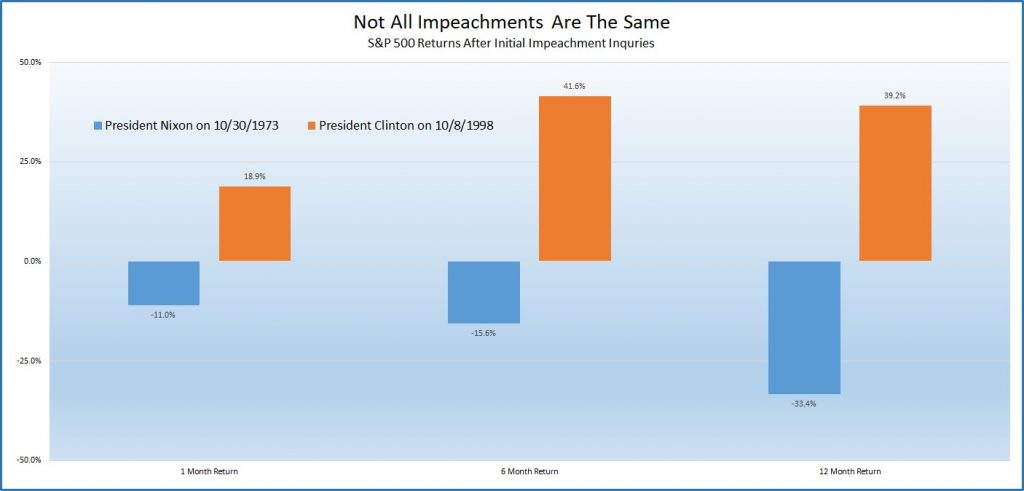

Warren Is Now The Favorite To Be The Democratic Nominee

The Democratic primary is really heating up as Elizabeth Warren has momentum in the polls. Debates will be shaken up as she will be the center of attacks instead of Biden who was the previous front runner. In the past 2 national polls, Warren was up by 1 and 2 points. That explains the chart below which shows her odds of being the nominee spiking to about 50%. Biden’s lead in the average of recent polls has fallen to 7.6% which is the lowest this year.

An October debate on the 15th and possibly the 16th will have 12 candidates. Warren has seen bursts in the polls after the previous debates. It will be interesting to see how she does as the front runner. The market will begin digesting her policy proposals in the next few weeks if she stays high in the polls.

Her policies will be discussed in detail in the media now that she has a serious shot of being President (she has a 24.7% chance of being President). That could be bad news for the banks and healthcare. She’s known for her strict proposals on bank regulations and could support a version of Medicare for All.

Rally In Treasuries Keeps Gaining Steam

Longer the yield curve stays flat, the more it is like the inversions which didn’t come right before recessions. This could be like the 1998 inversion. That would consistent with calls for no recession this year and next year. 10 year yield is at 1.7% and the 2 year yield is at 1.66%. The curve is almost perfectly flat. Odds of a rate cut by the end of the year are 71.3%. NY Fed President James Bullard stated, “We’ve made a big move. I think we probably have a little bit more to go here.”

It’s interesting that 2 rate cuts is considered a big move now. He called for 2 cuts at the last meeting, so it would have been bigger. It’s not a shock he thinks there’s more room to cut since he voted for another cut this month. Personally, I don’t see the room for another cut because it limits the ammo to deal with a recession. Just because I don’t see a recession occurring soon, doesn’t mean I don’t the Fed should be prepared for one. Fed should let the rate cuts it has already done flow through the system.

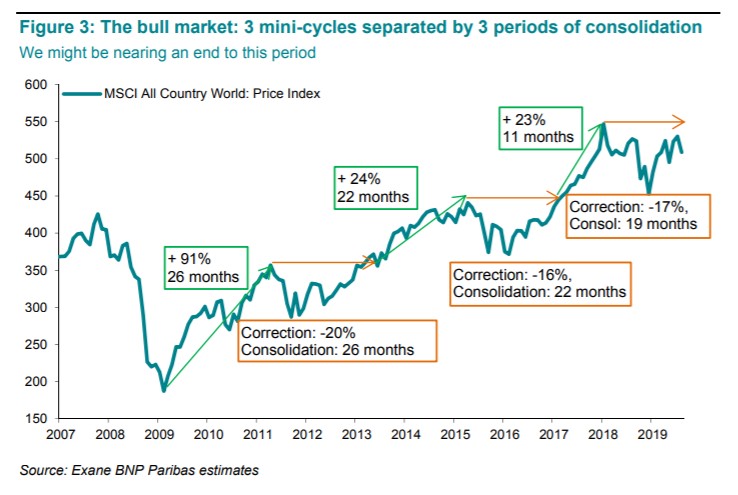

Mini Cycles

This expansion has had mini cycles in terms of economic growth and equity performance. It's the 3rd US slowdown. Even though the S&P 500 has surpassed its January 2018 high, the MSCI all country world index is still below its record high made in that month.

The chart below shows the 3 mini cycles in this bull run which started in 2009. In the market consolidated of 2012-2013, the index fell 20%. It also consolidated from 2015-2016 when the energy market imploded as it fell 16%. In this consolidation, it has fallen 17%. The past 2 lasted 26 and 22 months. This one has been 19 months. If this one is 24 months, which is the average of the past 2, it would be consistent with the call for a global cyclical recovery in 1H 2020.

Conclusion

I’m much more focused on the Democratic primary than I am Trump’s supposed "impeachment inquiry." Especially since he probably won’t be removed from office. And the Dems will pick a candidate within the next 5-9 months. The stock market should stay near where it is now until the trade meetings and earnings season get under way in the next 2-3 weeks.