Weak PMIs and Trade War Send Stocks Lower

The stock market started what is the worst month on average (September) with a loss as the S&P 500 fell 0.69% on Tuesday. The Nasdaq fell 1.11% and the Russell 2000 fell 1.51%. The VIX was up 0.68 to 19.66 as the market is still technically in a correction. It might be better to call this a range bound market as there hasn’t been a new low for a few weeks. I think the market is holding up very well considering the weak data and the negative headlines.

I’m not saying stocks should have collapsed because of the weak manufacturing PMIs which weren’t a huge shock. However, a slowdown as bad as 2015-2016 could easily justify a 10% correction. Add in the trade war worries and it can get worse. The CNN fear and greed index makes it seem like that negative situation is already here because it is at 25 which is extreme fear. There isn’t extreme fear in the S&P 500 though.

Most sectors fell on Tuesday as only 3 were up. It was a classic ‘risk off’ day as consumer staples, utilities, and real estate were all up. They increased 0.51%, 1.31%. and 1.75%. That’s massive outperformance for the utilities. This sector has been on a rampage along with treasuries. It is up 22.46% year to date. It hit another record high. From September 4th, 2015 to July 22nd, 2016 the sector was up 28.81%. From June 8th, 2018 until today, the sector is up 30.8%. That’s not the exact same length of time, but from peak to trough, this has been a better run than the one from 2015 to 2016 when the 10 year treasury yield hit a record low. In this run, the 30 year yield hit a record low.

The worst sectors were the industrials and tech which fell 1.42% and 1.26%. The industrials obviously didn’t like the weak manufacturing PMIs. I simultaneously think it’s too early to call for a recession and that it’s too early to call for an end to the manufacturing weakness. There isn’t much evidence for either thesis. You can make a lot of money if you are sure of either call, but it also doesn’t make sense to bet on hope with no support.

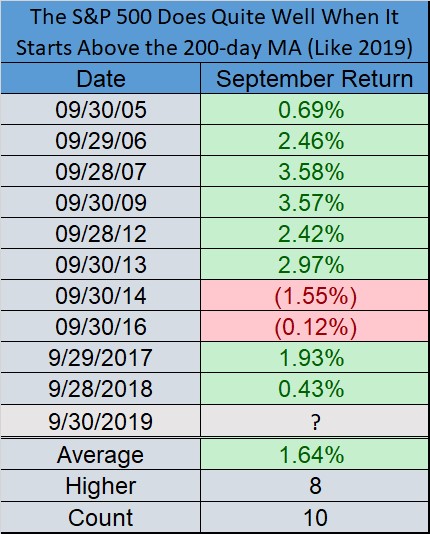

Stocks Can Rally In September If There Is Momentum

We know September is the worst month of the year, but lately it seems like August has been the source of pain for investors. Could traders be front running this expected volatility? Personally, I don’t pay much attention to how stocks do seasonally because there can be positive setups in bad months and negative setups in good months. For example, stocks rallied in September last year and cratered during what was supposed to be the Santa Clause rally.

If you need a reason to go against the historical data in September and buy stocks, the table below is for you. As you can see, the average return in the past 10 Septembers in which the S&P 500 started the month above its 200 day moving average, like it did this month, is 1.64%. 8 were positive and 2 were negative. Momentum trumps calendar effects.

Trump Tweets Are Bad For Stocks

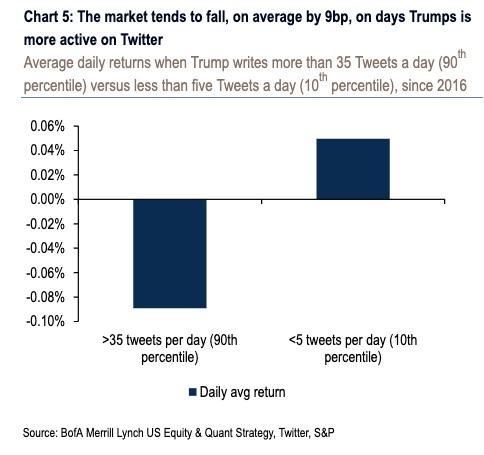

As you can see from the chart below, when Trump tweets more than 35 times per day, stocks fall an average of 8 basis points and when he tweets less than 5 times per day, stocks rise 4 basis points. If this chart highlighted tweets mentioning trade, the bifurcation would have likely been bigger. Obviously, there are plenty of tweets that don’t impact markets. There’s not much we can do with this information because we don’t know when Trump will tweet a lot ahead of time.

The latest new on the trade war is that President Trump wanted to double the tariffs after China put a tax on $75 billion in U.S. exports in August. It’s not a good sign that tariffs could have been raised further, but it doesn’t necessarily mean the trade war will go on much longer. This is Trump’s final period where he can increase his threats in the game of chicken to get China to give in. 6 months from now, he will be at the start of the Presidential election.

On Tuesday morning, Trump tweeted, “We are doing very well in our negotiations with China. While I am sure they would love to be dealing with a new administration so they could continue their practice of “ripoff USA.” Here he is acknowledging that China is waiting until the end of his presidency. As I have mentioned in previous articles, that might not be a great idea for China because the Democrats probably won’t go easy on China as well. The negotiating style will be different, but America will have similar demands.

September Fed Meeting Is Coming Soon

With the decline in treasury yields on Tuesday, they are near their recent lows. The latest change is that the 10 year 2 year spread is normal. While it’s a bad thing for the curve to steepen, this movement isn’t enough to mean anything. The latest 2 year yield is 1.46% and the 10 year yield is 1.47%. We need to see about a 50 basis point gap before I get nervous about a recession.

The September Fed meeting is coming soon as it is only 14 days away. There is a 93.8% chance of a rate cut of 25 basis points and a 6.2% chance of 2 cuts. The most likely options by the end of the year are either 2 or 3 more cuts, bringing the total to 3 or 4. I remember when the Fed was planning to hike rates 3 times in 2019. Much has changed in the past year. The slowdown has gotten worse and the trade war has seen more tariffs. The 20% decline late in 2018 set the stage for these rate cuts. Core PCE inflation being below 2% has helped the cause for cuts.