Below Trend Growth, No Recession

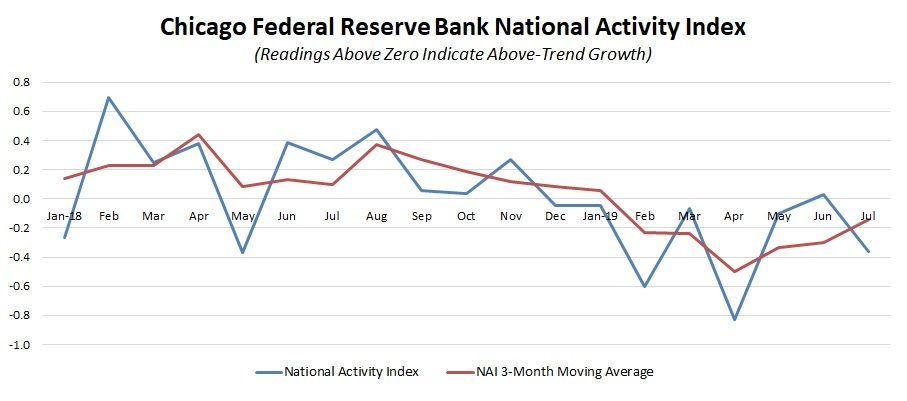

Bears loved the July Chicago Fed National Activity index because it was negative for the 7th time in the past 8 months. It would have been 8 out of 8 if it wasn’t for the 5 basis point positive revision to the June reading. However, even with all this negativity, the 3 month moving average increased from -0.30 to -0.14 because the terrible April reading wasn’t included anymore. A terrible April reading was revised down 10 basis points to -0.83 making it the worst reading since early 2014. If that was the 3 month moving average, it would signal a recession. Anything below -0.7 is recessionary.

Even though the July reading was weak, the 3 month average isn’t close giving off a recession signal. The economy is simply growing below trend. If below trend meant a recession, we would have seen many recessions since 2009. As you can see from the chart below, July’s index was -0.36 which was the worst reading since April. 59 individual indicators in this index made negative contributions and 26 made positive contributions.

The production category hurt the index by 0.25. Personal consumption and housing hurt the index by 0.06. Sales orders and inventories hurt it by 0.05 and employment hurt it by 0.01. Employment growth has been weakening recently especially if you look at the latest revisions to the data. Good news is housing looks like it’s about to go on an upswing especially if you look at the great June new home sales report which hit a cycle high.

China Disagrees With Trump’s Statement

Latest news on trade is China stated it didn’t come back to the negotiating table like President Trump stated. the President framed it as if China was scared of the tariffs and was finally willing to give in to what he wants. If Trump had stated the negotiations have restarted in a neutral manner, China may have agreed. It’s very clear, we aren’t on the cusp of a deal before the September 1stdeadline.

The way this trade war has worked is negotiations have followed new taxes. Then the negotiations hit a snag at which point Trump threatens more tariffs. Then new taxes are announced and the cycle starts over again. Question is, where will the tariffs go from here if the next round of negotiations in the next few months don’t go well? Options this fall will be extreme action or substantive negotiations where something gets done.

If you visualize a game of chicken as 2 cars driving headfirst at each other, this latest group of tariffs is like both cars increasing their speeds to 80 miles per hour. There will be major economic damage in 2020 if nothing gets done. Some say China will ramp up its tariffs to hurt the U.S. economy just as President Trump runs for re-election. However, I think the current plans will already do damage to his chances. The economy is already in a cyclical slowdown, so it doesn’t take much to catalyze a significant slowdown.

The chart below breaks down the categories that will see higher tariffs in the next few months. Because Trump delayed some of the phase 3 tariffs until the holiday shopping season is over, the December 15th tariffs have a big impact on toys & sports equipment, footwear, and electronics & electrical machinery. As you can see, there will be a big impact on final consumer goods and capital goods in December. However, let’s not sleep on the September tariffs which will have a big impact on textiles & clothing, vegetable products, and fuel.

Conference Board Consumer Confidence Increases

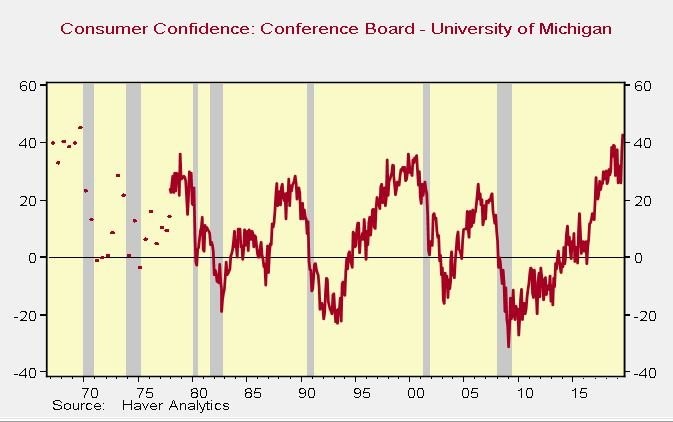

Conference Board Confidence index beat estimates and fell slightly. That’s much different from the University of Michigan index which was weak. The difference between the Conference Board and University of Michigan index is itself an indicator. As you can see from the chart below, the difference spikes at the end of the cycle. The divergence is at a record high. This record may be generated by the fact that this is the longest expansion since the 1800s. I’m not willing to call a recession based on this stat. However, it certainly gives caution to this great August Conference Board index.

Headline index fell slightly from 135.8 to 135.1 which beat estimates for 130 and the high end of the estimate range which was 133. Present index was up huge and the Expectations index fell. That’s the same type of divergence that occurs at the end of expansions. Present index was up from 170.9 to 177.2 and the Expectations index fell from 112.3 to 107. The difference between the two indexes is the highest since November 2000.

Even though employment growth has fallen, consumers’ opinion on the job market improved. Those saying jobs are plentiful increased from 45.6% to 51.2% and those saying jobs are hard to get fell from 12.5% to 11.8%. Expectations weren’t as great as the proportion of consumers expecting more jobs to be available in the next 6 months fell slightly from 19.9% to 19.7%. Those expecting fewer jobs rose from 11.1% to 13.6%. Those expecting in short term income prospects to improve fell from 24.9% to 23.8%. However, those who see their income falling in the short term also fell as it went from 6.6% to 5.8%. The net change was marginal.

Conclusion

Chicago Fed National Activity index was weak, but technically it signals the odds of a recession fell because the terrible April reading is gone. July results can easily be revised to below -0.7, but as of now, I don’t see a recession. The trade war is about to have a major impact on economic activity in the fall. GDP growth in 2020 will face a lot of headwinds if there isn’t a trade deal soon. I see one occurring by the end of the year. We will know if I’m correct by December 15th. Conference Board index was very strong in August, however, it usually spikes much more than the University of Michigan index at the end of the cycle, so be careful of that.