Solid Headline Durable Goods Orders Growth

The July durable goods orders report is an example of headline data not matching the details of the report. New orders growth was 2.1% monthly which beat estimates for 1.2% growth. That’s great even though the June reading was revised slightly lower from 2% to 1.8%. Yearly growth was weak, but showed solid improvement as it went from -1.9% to 1%. That was the highest growth since January and the first positive reading since March. The 2 year stack showed very strong improvement since the comp got tougher. The 2 year growth stack improved from 0.7% to 11.2%.

The problem with this headline reading is it was driven by transportation order growth. Civilian aircraft orders were up 49% after increasing 101%. It’s good to see an improvement after the grounding of the 737 MAX, but aircraft orders are very volatile. They don’t help determine the direction of economic growth. It’s better to look at ex-transportation and core results. Motor vehicle orders were up 0.5% in July. Even though that’s obviously in the transportation category, it’s good to see. The July motor vehicle sales report showed some weakness. Autos were blamed for weakness in the August flash Markit manufacturing PMI.

Weak Core Durable Goods Results

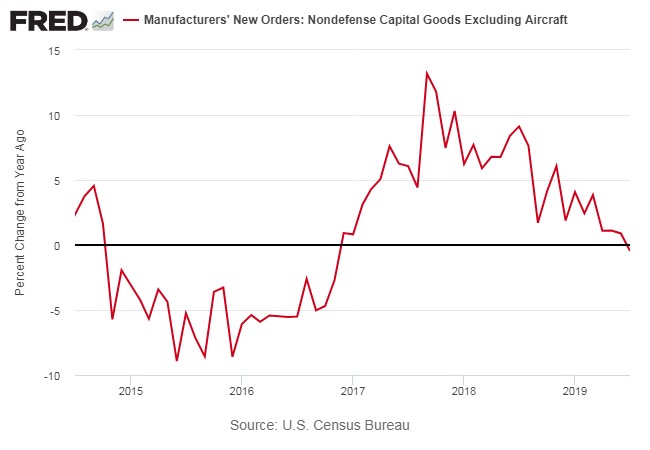

Ex-transportation monthly growth missed estimates and core growth only beat estimates because the June report was revised sharply lower making for an easier comp. Specifically, ex-transportation monthly growth was -0.4% which missed estimates for no change. It missed estimates even though June’s growth rate was revised down from 1.2% to 0.8%. Core capital goods growth was 0.4% which beat estimates for no change. However, June’s reading was revised down sharply from 1.9% to just 0.9%. As you can see from the chart below, yearly growth fell from 0.9% to -0.5%. That’s the worst reading since November 2016. During the last manufacturing recession, growth troughed at -8.9%. Unlike headline growth, the 2 year core growth stack was fell modestly as it went from 9.3% to 8.6%.

Shipments of core capital goods orders fell 0.7% which is a bad sign for non-residential fixed investment growth in the GDP report. This growth was negative in the Q2 GDP report; it’s starting out weak in Q3. Orders for primary metals, fabricated metals, and machinery fell 1%, 0.9%, and 0.6%. Communications equipment growth was strong as it was up 1.9% after increasing 3.7% and 2%. Electrical equipment orders were up 1.1% even though they also faced tough comps.

Unfilled orders were up 0.1% after falling 3 straight months. Inventories rose 0.4% and total shipments fell 1.1%. That’s not good news because it means production will need to fall soon. In Q2 inventory investment fell while consumption rose which implied inventory investment would increase in the 2nd half if demand stayed strong. Demand might not be strong in Q3 because the tariffs have hurt consumer sentiment.

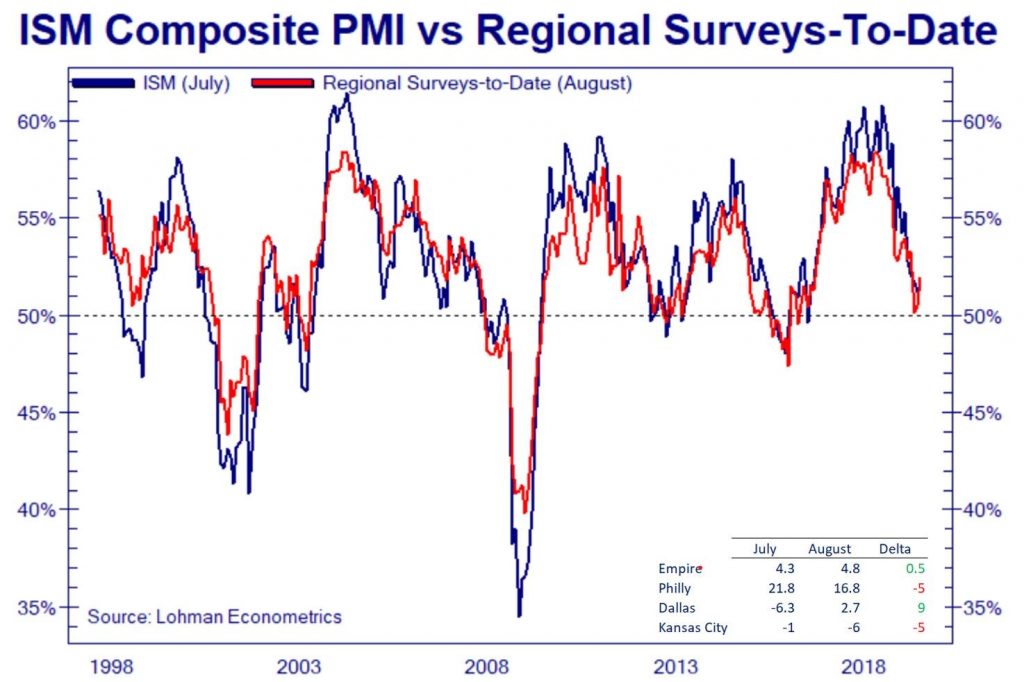

Dallas Fed Index Beats Estimates, Pulling Up Average

The Dallas Fed manufacturing index showed solid improvement which pulled up the average of the regional Fed surveys. Now half of the 4 have beaten their July results. The Dallas Fed index showed more of a sequential change than any of the others, so it had a big impact on the average. The final regional reading is on Tuesday when the Richmond Fed report comes out. The ISM manufacturing PMI comes out next Tuesday after Labor Day. The last PMI was 51.2.

I had expected the PMI to decline because of the previously weak regional Fed readings, the overall trend lower, and the tariff announcements. As you can see from the chart below, the Dallas Fed index’s increase pushed the average towards expecting a modest improvement in the PMI. That would be different from the Markit flash PMI which fell from 50.4 to 49.9. Remember, the new orders reading is part of the leading indicators index. The index will likely be hurt by the S&P 500’s August performance.

Now let’s look at the details of this surprisingly solid Dallas Fed report. The production index was up from 9.3 to 17.9 and the general activity index was up from -6.3 to 2.7 which beat estimates for -3 and the high end of the estimate range which was -2. It’s interesting that most of the results in the current index showed improvement, but most of the results in the expectations index fell. In the current index, new orders were up 3.8 points to 9.3, while in the expectations index they fell 8.1 points to 23.7. In the current index, shipments were up 7.4 points to 17.6 and in the expectations index they fell 13.7 points to 26.2.

Capex and the outlook uncertainty index were consistent with 6 month expectations as capex fell 7.8 points to 7.4 and uncertainty increased 8.9 to 18.6. Somehow even though every single index in the expectations category except delivery time fell, the outlook index rose 5.9 points to 5 in the current index (it was also up in the expectations index). Finally, the expectations for general business activity fell 4.6 points to 1.4.

Now let’s look at the quotes from this interesting report. Most of the quotes mentions tariffs and the trade war. The most interesting quote was from a transportation equipment manufacturing firm which stated, “Although we are required to “Buy American” for material procurement, uncertainty in the import marketplace relating to tariffs continues to put upward price pressure on U.S.-sourced supplies. We are eager to see a clearer rationale behind this administration's attempts to develop a business strategy.” Obviously, these firms don’t like the higher costs tariffs cause. The firms are angry because they don’t see how the trade war is going to help them. The goal of the tariffs is to promote free trade and fairness. That will only be achieved with a good trade deal.

Conclusion

Core durable goods orders fell yearly which is a negative for the overall economy. One solid regional Fed reading isn’t enough to counteract that negative, but it was enough to significantly push up the average of the 4 readings which increases my expectation for the August manufacturing PMI. The Markit flash PMI was much more negative.