Amazing New Home Sales Revision

It's always good look at the revisions to data as well as the latest numbers. Usually, I look at the latest numbers the closest. Revisions aren’t extreme and the market reacts to the latest numbers. In the case of the July new home sales report, the revision was extreme, which is why it’s the story of this report.

Whatever number is largely different than expectations gets the coverage. That’s why the negative employment revision earlier this week was so important. It fundamentally changed how we must look at the 2018 labor market. I believe we should look at old data because it can alter how we see the future.

You can’t ignore a decline of 501,000 jobs, but focus heavily on a monthly report missing estimates by 50,000. The revision is literally 10 times larger than that example miss.

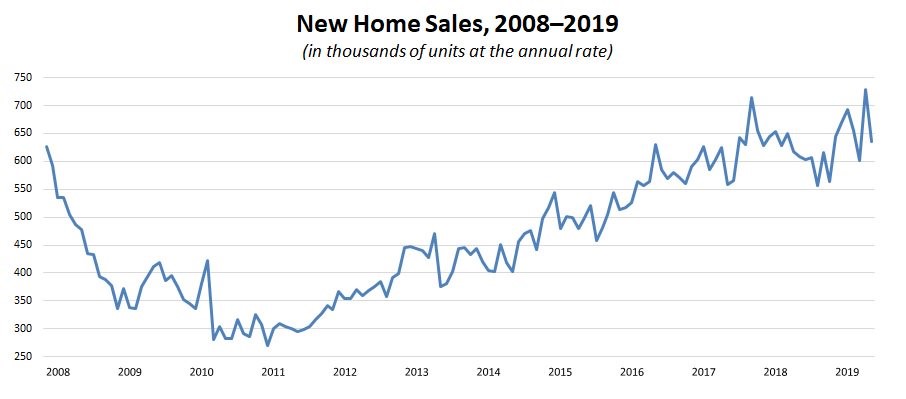

This sharp revision to the June new home sales report sounds almost too good to be true. It might be revised lower in future reports. The June new home sales reading went from 646,000 to 728,000.

As you can see in the chart, that’s a new cycle high. Some macro investors use the number of months since the cycle peak as a recession indicator. In other words, the fact that the November 2017 new home sales reading wasn’t surpassed for 19 months was a recession signal.

Recession calls obviously gets stronger if new home sales trend lower rather than stay range bound like they have. Because new home sales were relatively close to the peak, the recession call was always flimsy. However, the June reading can also be revised lower. At least it’s an older report, rather than a new one hitting a record high. A new one would be subject to one more revision. It would be less likely to be accurate.

New home sales weren’t that great in July which made economists wonder if this should be considered a good report. Specifically, new home sales were 635,000 which missed estimates by 10,000. Since the June revision was higher than that miss, I’d say this was a good report.

Also, the new record high made the recession call go away. Because this report has been so volatile recently, the 3 month moving average actually fell from 663,000 to 655,000. The 3 month average peaked this year at 670,000 in March and April.

There was a 1.2% increase in the number of new homes on the market. It was 337,000 which equates to 6.4 months of supply. The median price of new homes was $312,800 which is a 2.2% monthly increase and a 4.5% yearly decline. Sales were up 4.3% versus last year. It seems like price and sales are inversely correlated as sales fell monthly and were up yearly, while prices were up monthly and fell yearly.

Powell’s Jackson Hole Speech

Powell’s Jackson Hole speech was upstaged by President Trump’s hawkish trade tweets. In fact, Powell mentioned trade in his speech before President Trump made his latest statements. Powell stated, “Trade policy uncertainty seems to be playing a role in the global slowdown and in weak manufacturing and capital spending in the United States.”

That’s a reiteration of the obvious. 5 of the 11 comments in the Kansas City Fed manufacturing report mentioned tariffs. They weren’t positive!

Powell wants to have his cake and eat it too because he wants to cut rates to support the economy, but he doesn’t want the rate cuts to scare people into thinking a recession is coming. Cutting rates and then telling people there is nothing wrong doesn’t inspire confidence.

As evidenced in the University of Michigan consumer confidence report, the Fed’s July rate cut caused consumers to become more uncertain. If that made them nervous, they will get even more nervous in the next few months because the Fed will likely be cutting rates multiple times.

The Fed is cutting rates because of the decline in global growth. Morgan Stanley sees global growth falling to the lowest point of this expansion in Q4 2019, but doesn’t see it falling below 2.5% which is considered the recession threshold.

On global risks, Powell stated, “We have seen further evidence of a global slowdown, notably in Germany and China. Geopolitical events have been much in the news, including the growing possibility of a hard Brexit, rising tensions in Hong Kong, and the dissolution of the Italian government.”

Latest flash August Markit data from Germany actually was strong. I’m not saying Powell is wrong because July industrial production growth was the weakest since the financial crisis. However, the flash composite PMI increased from 50.9 to 51.4 which was a 2 month high. It was driven by manufacturing which increased from 43.2 to 43.6.

Services PMI fell from 54.5 to 54.4. Hong Kong protests are partially related to economics. Its housing is unaffordable causing a drop in fertility. As you can see from the chart below, Hong Kong is by far the most unaffordable city with at least 1 million people in the world.

Interestingly, Powell spoke positively about the U.S. economy. He stated, “Our economy is now in a favorable place, and I will describe how we are working to sustain these conditions in the face of significant risks we have been monitoring.”

It’s odd to see a Fed chair speaking glowingly about the economy while cutting rates. His perspective that the U.S. economy is outperforming the rest of the world might be off because America’s latest PMI was lower than that of Europe.

The Fed is being pushed to cut rates by the strong dollar. The situation might work itself out without action if Europe improves while America weakens. That would create a different reason to cut rates. Obviously, the most ideal situation is a global cyclical upturn where America participates, but doesn’t lead growth higher.

To keep the dollar from hitting record highs, we’d also need to see global central banks not as dovish as the Fed. The dollar is a catch 22 because a strong dollar hurts the economy, but the dollar is strong because the economy is doing relatively well. We haven’t fully seen the ramifications of the strong dollar on corporate profits yet. We will during Q3 earnings season in a couple months.