Recessionary Fears Catapult Higher

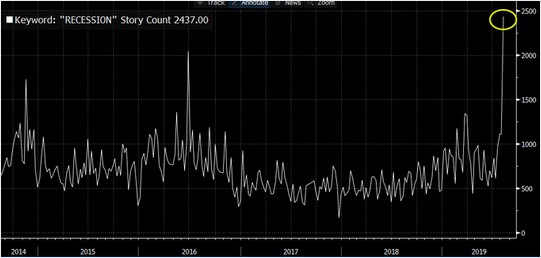

Every stock market correction prices in some recession fears. It’s normal to expect an uptick in expectations for a recession after declines. The larger the decline, the more fear ramps up. A prime example was late last year when stocks fell 20%. This latest correction is different because the 10-2 year treasury spread inversion exploded recession fears despite stocks falling modestly on tariff fears and the weak manufacturing data. As you can see from the chart below, recession news stories hit the highest total since at least 2014. Discussions of the yield curve inversion hit the mainstream. Personally, as someone who has been following the yield curve for years, it’s surreal to hear non-finance people discuss it. I’m not sold on the recession thesis especially with the solid retail sales report, recent rate cut, and potential for a trade deal.

Fund Managers See A Global Recession

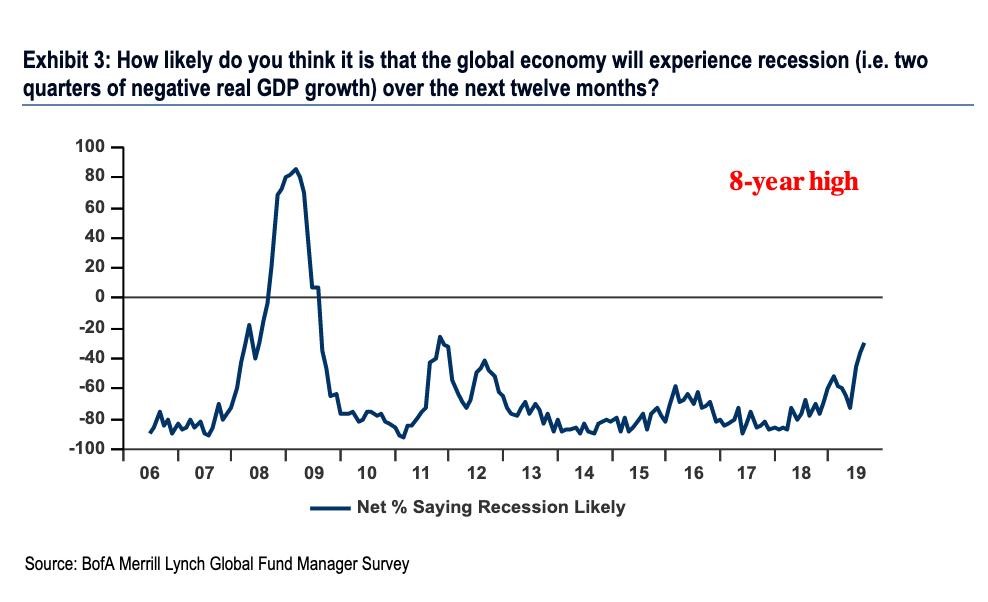

As you can see from the chart below, it’s not just non-finance professionals seeing a recession. In the August Merrill Lynch survey, the net percentage of fund managers seeing a global recession was the highest in 8 years. I find the title of the graph to be weird because it states a global recession is 2 straight quarters of negative GDP growth. That’s not the definition of a recession. It’s also very rare for the global economy to have negative GDP growth on a yearly basis. Since 1961, only in the year 2009 was yearly GDP growth negative. Global growth is lower now than it was in the 1960s and 1970s, but it would still take a significant negative catalyst to push it negative.

The global services PMI actually improved in July as it went from 51.9 to 52.5. If the trade war is resolved, then the manufacturing economy can turnaround. Regardless of whether this current below trend global growth period is called a recession is becoming less relevant as I see an upswing next year with the increase in monetary stimulus and a potential trade deal in the works.

August Philly Fed Index Beats Consensus

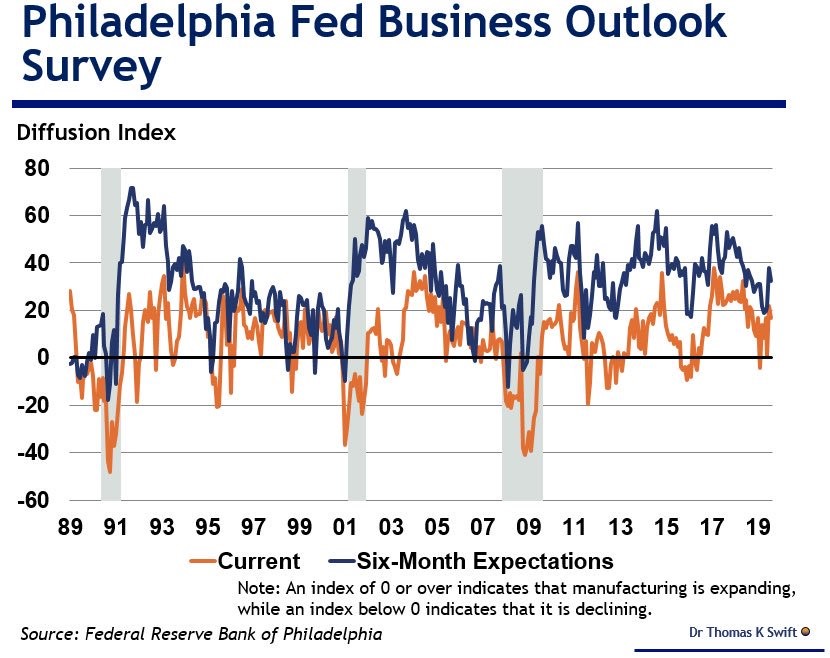

The August Philly Fed manufacturing index was relatively strong even though it fell from last month. It beat the high end of the estimate range which isn’t consistent with the weakness in the July industrial production report. Comparing the July Philly Fed index with the latest industrial production report (which is apples to apples) shows an even bigger difference as the index was 21.8. It fell to 16.8 in August as you can see from the chart below. That beat the consensus of 11.1 and the high end of the expected range which was 16.4.

The August new orders index actually improved from 18.9 to 25.9. The headline index fell partially because the shipments category fell from 24.9 to 19. The number of employees index also hurt the general business conditions index as it cratered from 30 to 3.6. The July BLS report showed there were 16,000 manufacturing jobs added which more than tripled estimates for 5,000. On the other hand, the workweek calculation was consistent with the BLS report. The workweek index fell from 23 to 6.8. In the July BLS report, the workweek length fell from 40.7 hours to 40.4 hours. This category is much higher than the overall average which was 34.3 hours.

The 6 month expectations index fell similarly to the current index; it was down from 38 to 32.6. The new orders index fell slightly from 45.7 to 44.1. Unlike the current index the number of employees and average workweek indexes barely changed. The shipments index was up from 41.3 to 43.5. This report isn’t consistent with the manufacturing decline show in the industrial production report. As I mentioned in a previous article, just as the weak July industrial production and strong retail sales reports came out, the reverse was shown in the subsequent August soft data reports.

Empire Fed Index Improves

The August Empire Fed index wasn’t as strong as the Philly Fed index, but it improved which means the two converged. The general business conditions index rose from 4.3 to 4.8 which beat estimates for 2.5. Similar to the Philly Fed index, the new orders index increased 8.2 points to 6.7. The shipments index was up 2.1 points to 9.3. The employees indexes were correlated with the July BLS reading since the number of employees index was up 8 points to -1.6 and the workweek index fell 5.1 points to -1.3.

The 6 month expectations index fell 5.1 points to 25.7. It didn’t improve like the current index. New orders fell 3.7 to 31.7. The good news is shipments, capex, and technology spending were all up. They increased 1.6, 4.2, and 2.8 points to 31.1, 23.2, and 17.4.

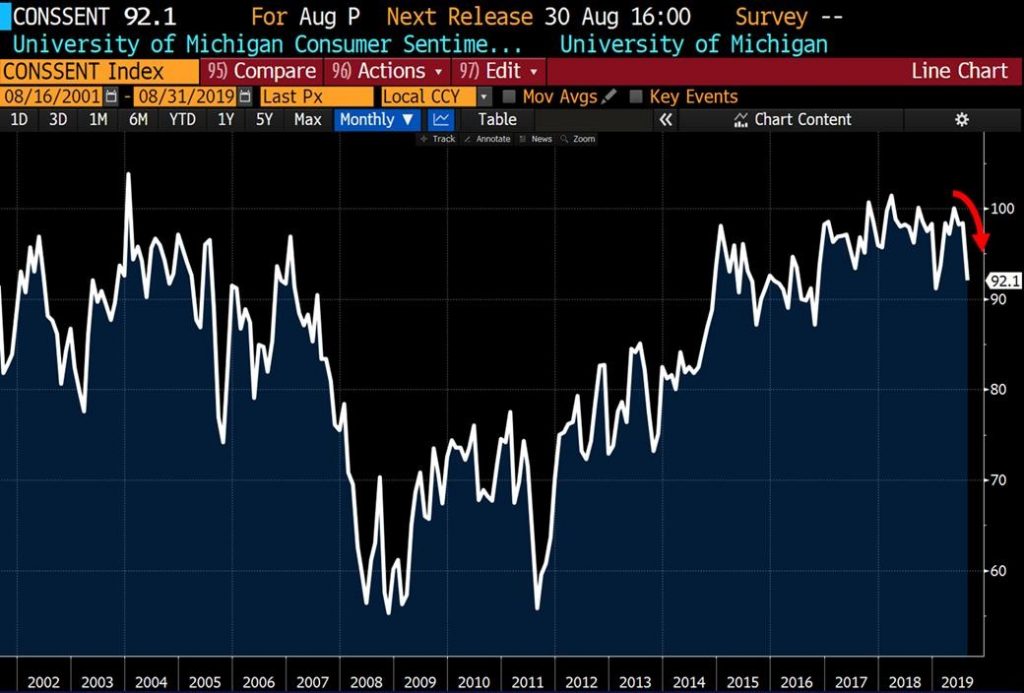

Consumer Confidence Falls

Concluding the theme of soft reports reversing what hard reports showed, the August preliminary consumer sentiment reading went against the strong July retail sales report. The index fell from 98.4 to 92.1 which missed the consensus for 97.5 and the low end of the estimate range which was 95.1. This was the weakest report of 2019 as you can see from the chart below. This weakness was caused by the trade war and monetary policy which caused the expectations index to fall sharply. It fell from 90.5 to 82.3 while the current index only fell from 110.7 to 107.4. The expectations index was down 5.5% yearly and the current index was down 2.6%. The current index was the weakest since late 2016.

In this survey, 33% of consumers spontaneously mentioned tariffs which was just below the recent peak of 37%. I don’t think the delay of certain tariffs until December 15th will help the consumer. I think it will just confuse the consumer which isn’t a positive. This report also showed consumers followed the Fed’s lead in expecting a recession. The goal of a rate cut is to ease financial conditions, but since consumers know the Fed cuts rates when the economy is headed for a recession, they became more apprehensive because of the cut.

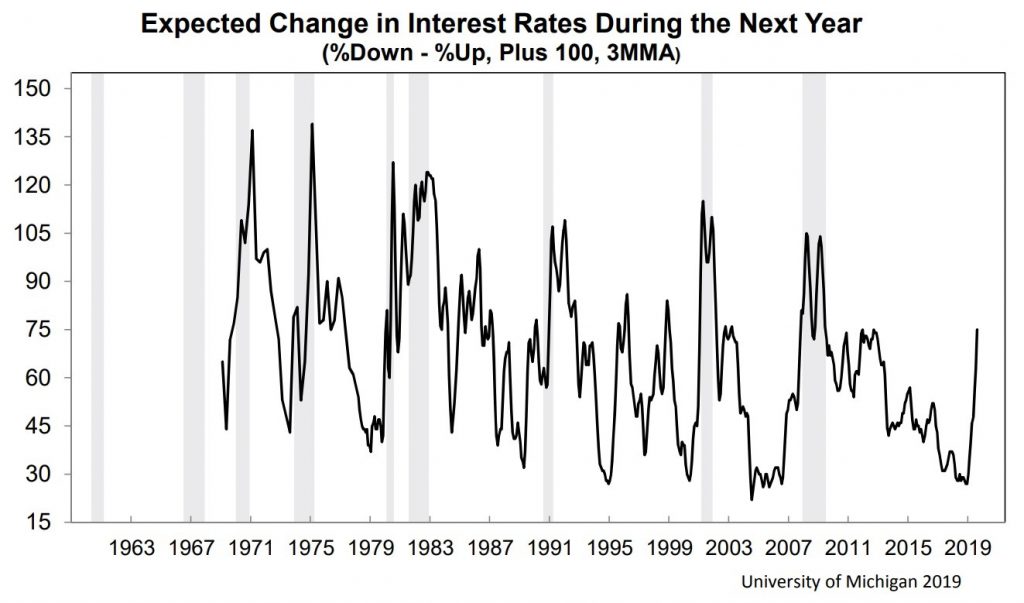

The chart below shows consumers expect rates to fall usually around recessions, but there are some false alarms. The University of Michigan survey suggests a recession probably isn’t coming soon though because of the strong labor market. The hope is the strong labor market quells the concerns caused by the tariffs and the rate cuts.