Very Wild Monday

Monday was the worst day of the year for stocks as the most interesting week for markets was followed by the most interesting day. Last week was the worst week of the year for stocks. I’m not saying these past few days have been interesting because of the declines. It’s because of the news on the trade war front which I will review in this article.

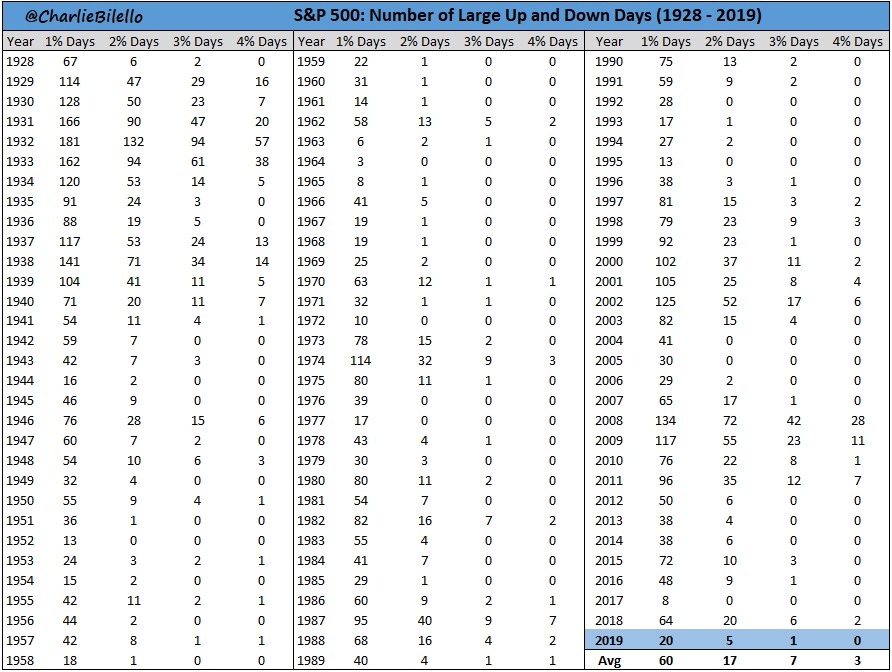

The S&P 500 had its 6th straight day of losses as it has quickly moved from being overbought to oversold. This was the 4th quickest 5% pullback since the start of the bull market in 2009. In total the market is down 6% which isn’t massive at all. As you can see from the table below, the S&P 500 has only had 5 down days of 2% or more this year which is below the average of 17. Since the year is halfway over, volatility is below average. The market was overdue for at least a minor correction.

Sector By Sector Performance

The S&P 500 fell 2.98%, the Nasdaq fell 3.47%, and the Russell 2000 fell 3.02%. The Nasdaq’s 6 day losing streak is its longest since late 2016. The VIX was up 39.64% to 24.59. It is now elevated. It should come down in the next few weeks. As I mentioned, stocks are very oversold. The CNN fear and greed index fell 14 points to 22 which is extreme fear.

CNBC ran the infamous “markets in turmoil” program on Monday which seems to suggest stocks are close to a bottom. I wouldn’t buy stocks because of that program, but there is certainly a lot of fear in the market. Because the $300 billion tariff tranche will have a big effect on consumer products, the XRT retail sector ETF fell 2.22% on Monday. It has had a very rough few days as it is down 7.15% since July 24th. It is at a very technically important level as its low of $40.05 on May 31st is 5 cents lower than Monday’s close. If the index breaches that low, it will be at the lowest level since December 2018. Nike stock fell 2.67%; it down 11.75% since July 15th.

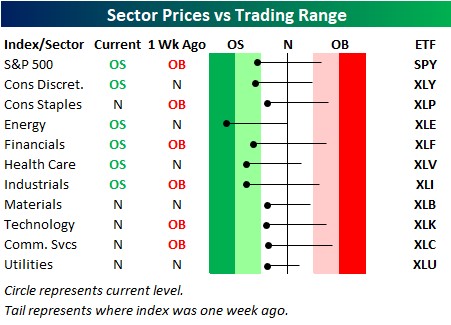

Only 11 stocks increased on Monday which is the lowest amount since December 24th, 2018. Every sector declined as it was a bloodbath. Tech did the worst as it fell 4.07%. Its decline was led by Apple which fell 5.23%; Apple will be hurt by the new tariffs and escalating tensions. Chinese consumers might not want to buy American products such as iPhones to support their country. It’s an act of solidarity. The financials also cratered as the sector was down 3.25% because rates are expected to be cut further as I will get to next. As you can see from the chart below, 1 week ago 5 sectors were overbought and now 5 sectors are oversold. The financials and industrials went from overbought to oversold. Energy is the most oversold.

Fed’s Mistake

The treasury market continued its epic rally as the 10 year yield fell 14 basis points to 1.71% and the 2 year yield fell 14 basis points to 1.57%. I was wrong to suggest the yield curve would invert if the 10 year yield fell further. That’s because the market is deciding for the Fed that it will cut rates in September and December. If the Fed states it’s not cutting rates in September, the stock market will immediately fall 5%. This would make it a real correction.

There is a 100% chance of a rate cut in September. The odds of a 50 basis point cut occurring went from 1.5% to 26.9% on Monday. Before this correction is over, I wouldn’t be surprised to see these odds get above 50%. The Fed would lose all credibility if it cut 50 basis points because it would signal this is the start of a cut cycle instead of a midcycle adjustment.

The market’s most likely scenario is 3 more rate cuts this year. That’s 4 total cuts this year. There is a 54.9% chance the Fed cuts rates at least 3 more times. In that case, the Fed will have used about half of its rate cut ammo unless it cuts rates below 0. The Fed’s best hope to avoid more than 1 more cut this year is for there to be a trade deal. I see a trade deal coming by the end of the year still. This latest action makes me more confident that there will be one.

China’s Reaction To Trump’s Tariff

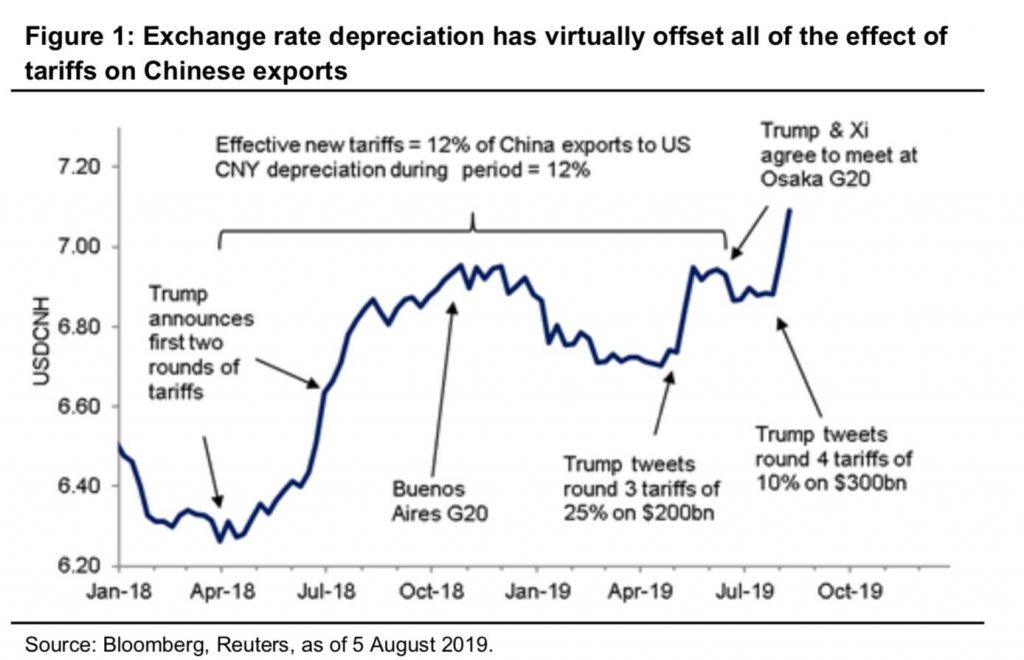

Stocks fell sharply on Monday because of China’s reaction to the 10% tariff. First, China let its currency fall below 7 to the dollar. This is its lowest level versus the dollar since 2008. As you can see from the chart below, the yuan’s depreciation has offset all the effect of the tariffs on Chinese exports. In reaction to this, the Trump administration labeled China a currency manipulator.

Secondly, China is halting all U.S. agriculture purchases. This aspect isn’t clear because Trump claims he issued the 10% tariff because China wasn’t buying the agricultural products it promised. If you follow Trump’s claim, China isn’t making much of a change. Thirdly, China might clamp down on American companies operating within its nation. There is anecdotal evidence China has created an undesirable entities list. This will hurt firms like Apple.

Conclusion

China reacted negatively to Trump’s tariff which shouldn’t be a huge surprise. This situation has been going on for a while. In the past 2 years, when the markets have reacted sharply, we have seen some sort of mini-resolution which allows for a relief rally even though nothing gets done. I think this volatility will lead to a mini-resolution in the next few days. More importantly, I see an intermediate term détente occurring within the next few months because President Trump wants the economy to be strong during his re-election bid next year. Neither side has the incentive to increase trade tensions enough to catalyze a terrible global recession.