Hawkish Cut

A Hawkish Cut ended up surprising many investors. Fed’s rate cut on Wednesday included hawkish guidance. Even though the Fed stated it would end the unwind of its balance sheet in August. That's 2 months earlier than it previously stated.

End of the unwind isn’t nearly as important as rate decisions. Rate cuts are the principle stimulus throttle that will be pulled in the next few months. There isn’t evidence of the Fed going through with another round of QE.

That would be weird since it is ending QT in August. There might never be another round of QE or the Fed might wait for clear signs of a recession to do so.

Mid-cycle Adjustment

Hawkish Cut - Fed watchers have Fed language down to a science, but sometimes the Fed throws a curve ball. Key term from this meeting was “mid-cycle adjustment.”

That means this was a one time rate cut rather than the start of a cutting cycle. Most investors never thought the Fed was going to guide for more rate cuts this year. But we thought it would leave the door open for them. That language shuts the door on future cuts.

While, that doesn’t mean the Fed won’t change its mind. It does make it tough for the Fed to cut rates in September.

Hawkish Cut - Unless something changes, next rate cut is more likely to occur in October than September.

If it happens at all. In May, the Fed claimed it was going to maintain rates and be patient.

It couldn’t cut rates in June even though Bullard wanted to. Especially because it just said it wouldn’t cut rates for some time. Now it will have a tough time cutting in September because it called the July cut an adjustment.

Difference between cutting in September and October doesn't matter much. But the lower chance of 3 cuts in 2019 in favor of 2 cuts does matter.

Keep in mind, I have predicted 2 cuts and the market was at 3. If it wasn’t for the market pricing in future cuts, I would say the Fed won’t cut rates again this year. Especially based on its statement and Powell’s press conference. That’s if you take them at face value which can be a mistake as it was in May.

Specifically, Powell stated, “We’re thinking of it essentially as a mid-cycle adjustment to policy."

Hawkish Cut - "That refers back to other times when the FOMC has cut rates in the middle of a cycle. And I’m contrasting it there with the beginning of a lengthy cutting cycle. That is not what we’re seeing now, that’s not our perspective now.”

On the one hand, this makes sense because the U.S. economy still has a solid labor market and a strong consumer. On the other hand, I don’t see this adjustment as doing much.

Why do it at all? If there’s such a great case for cuts, then cut rates and be open to more if the data supports a cut. Why close the door on more cuts without having new information? Fed usually makes mistakes when it closes the door on future policy.

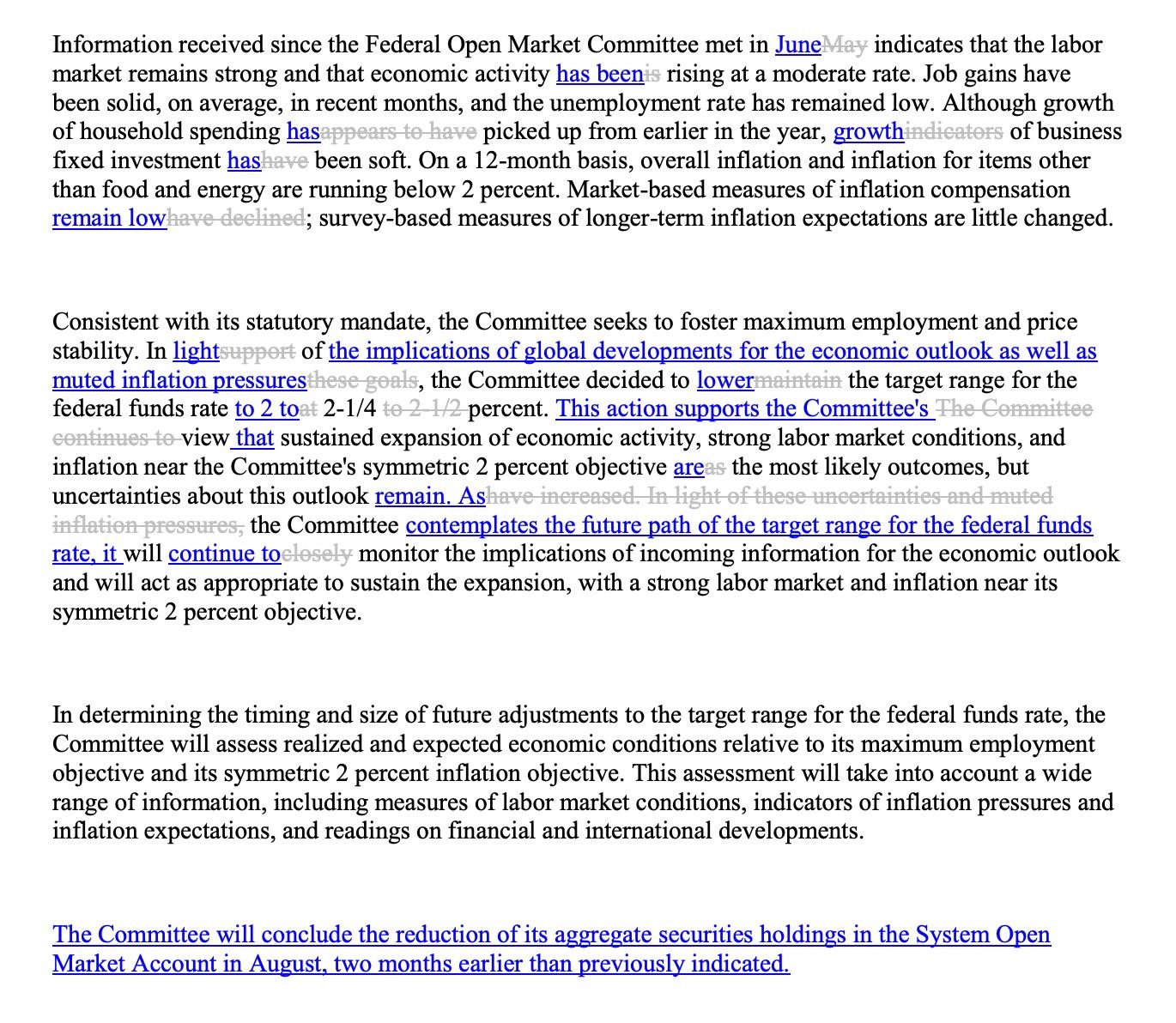

Hawkish Cut - Changes To Fed Statement

The image below shows the changes to the Fed’s statement. First, it’s notable that Ester George and Eric Rosengren voted against the rate cut as they felt the Fed shouldn’t have cut rates. That in itself makes this a hawkish cut.

First change to the statement was the Fed said, “household spending has picked up” rather than “appears to have picked up.” Fed was correct to be optimistic on consumer spending. Its June meeting as consumption growth was 4.3% in Q2.

Fed stated, “market-based measures of inflation remain low” rather than “have declined.” That signals the Fed has room to cut rates further. However, as we have learned from this statement and press conference, just because the Fed has room to cut, doesn’t mean it will.

Fed added the point that it is cutting rates because of “the implications of global developments for the economic outlook as well as muted inflation pressures.”

We knew that would be the reason for the rate cut along with the trade tensions. However, we didn’t know it would only be enough to cause one cut called an adjustment.

Additional Powell Quotes

Hawkish Cut - Many find it interesting that Powell stated this is a mid-cycle adjustment. Expansion is already the longest since the 1800s. Fed clearly doesn’t see a recession coming.

Maybe they are right that this is a mid-cycle slowdown. We will see in the next 6 months. Powell stated, there is “definitely an insurance aspect to this cut.” Maybe the Fed would have cut rates in the 2016 slowdown if they were higher.

Maybe this cut is like QE 2 and QE 3 which aimed to help a slowing economy. It’s possible the economy avoids a recession for a few more years, making cuts during minor slowdowns more popular.

Powell added, “What you’ve seen over the course of the year as we’ve moved to a more accommodative policy, the economy has performed about as expected with the gradually increasing support. Increasing policy support has kept the economy on track and kept the outlook favorable.”

Powell is giving the Fed credit for helping the American economy avoid a recession in the wake of global weakness and trade worries. It’s a fair point because financial conditions have remained loose, and the U.S. economy certainly isn’t in a recession.

The economy would be in much worse shape if the Fed would have hiked rates 2-3 times this year. On the other hand, if the Fed doesn’t keep easing, financial conditions might tighten. 1 cut might not be enough.

Hawkish Cut - Conclusion

In a shock to me and the market, the Fed went with a hawkish cut as it claimed this was a “mid-cycle adjustment.” That implies the Fed won’t cut for the rest of the year.

However, I still see another cut in October or December as probable. In my next article, I will describe how the market reacted to this decision and guidance.