Fed Turns Hawkish - Very Odd Statements By Fed Members

Fed Turns Hawkish and was extremely inconsistent on Thursday and Friday. It confused just about everyone following along. Heading into Thursday, we thought the Fed could cut rates twice. But it was only about a 20% to 30% possibility.

Then, Clarida and Williams made the dovish statements I discussed in a previous article. Next, as I mentioned in that article, the NY Fed walked back Williams’ statements. On Friday, Bullard further walked back those dovish statements and then Rosengren said the Fed shouldn’t even cut at all.

This all happened right before the blackout window starts on Saturday. That's where the Fed can’t make any public statements until after the meeting. Fed members appear to wildly disagree with each other.

NY Fed seems to disagree with its own President. Let’s now review the statements made by Bullard and Rosengren on Friday.

Bullard & Rosengren End Talks Of A Double Cut

Fed Turns Hawkish - In response to the idea of the Fed cutting rates by 50 basis points. Mostly due to slower global growth, lower inflation, and trade war worries, Bullard made a statement.

“I guess I would listen to arguments along that line, but at least sitting here today, I just don’t think the situation really calls for that aggressive of a move.”

Bullard was a dove at the June meeting as he called for a rate cut then. Now he states, a 25 basis point cut “would push us in the right direction and we can wait and see how things develop going forward.”

Bullard has actually been consistent in arguing against a double cut. However, it’s confusing to Fed watchers because of the discussions by Clarida and Williams on Thursday.

Fed Turns Hawkish - Boston Fed President Rosengren took his rhetoric a step further than Bullard

Especially since he doesn’t see the need for a rate cut yet. That’s a bombshell ahead of a meeting where there is a 100% chance of a cut as of Friday and there was over a 60% chance of a 50 basis point cut on Thursday.

Now the chance of a 50 basis point cut is just 22.5% which means it won’t happen. Specifically, Rosengren stated, “So, given that the economy is quite strong, given that I do think that inflation is going to be very close to 2%, and given that the growth in the economy is satisfactory, I think that’s an environment where you don’t have to take a lot of action.”

Rosengren stated the data has been good in the past month. Clarida just mentioned yesterday how the data has been bad in the past 6 weeks. That’s because Rosengren is looking domestically, and Clarida is looking abroad.

Ahead of this meeting where the Fed will definitely cut rates, Rosengren joins Kansas City Fed President Esther George as the only FOMC members not calling for a cut. I actually agree with them. U.S. economy is in solid shape. And I think there will be a trade deal by the end of the year. There is no need for the Fed to react to international economies.

An Unusual First Of The Decade Cut

Fed Turns Hawkish - This rate cut is unnecessary because 99% of the rate cuts since 1960 occurred with the unemployment rate higher. If rate cuts are meant to help the labor market, then they are unnecessary.

65% of the rate cuts occurred with higher inflation and 92% of the cuts occurred with higher rates. There isn’t much room to cut rates if there is a recession. To be fair, I don’t see a deep recession coming. Households haven’t taken on too much leverage this cycle.

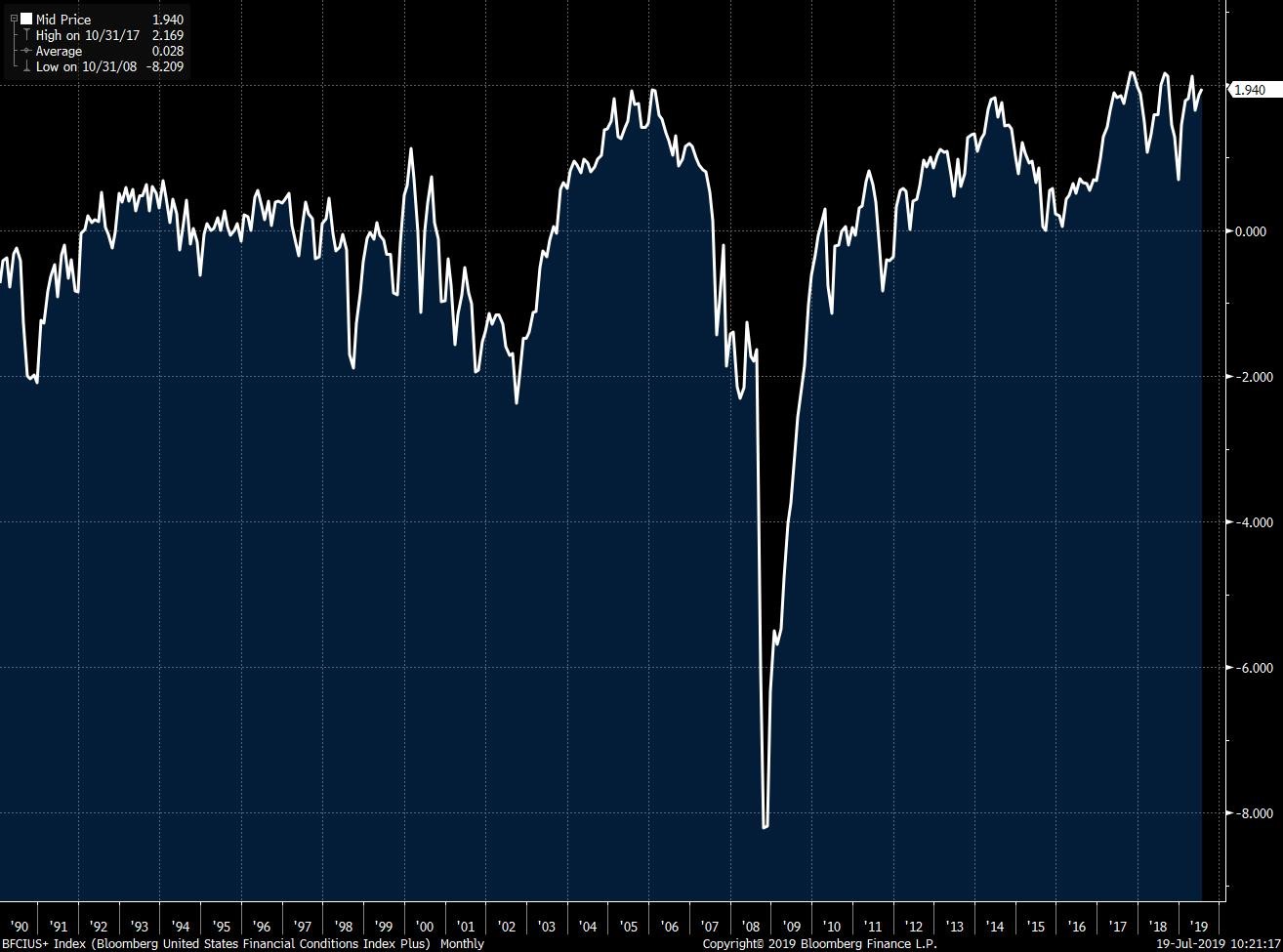

As you can see from the chart below, financial conditions are very loose. Since 1990, Fed hasn’t cut rates with the financial conditions index above zero and now it is near 2.

Fed Turns Hawkish - Weak Leading Index

Now let's explain why the even though Fed shouldn’t cut rates, leading economic indicators fell for the first time this year. Economic growth is in a slowdown. But I don’t see the need for rate cuts.

Fed didn’t cut rates during the 2015-2016 slowdown when the economy was weaker. The Fed actually raised rates in December 2015. This slowdown is similar in the sense that the Fed hiked rates in December 2018 and the market got worried.

One major difference is economic growth is stronger. Wells Fargo sees a very solid 3.4% growth rate in personal consumption expenditures in Q2.

In June, the leading economic index fell 0.3% monthly which missed estimates for 0.1% growth.

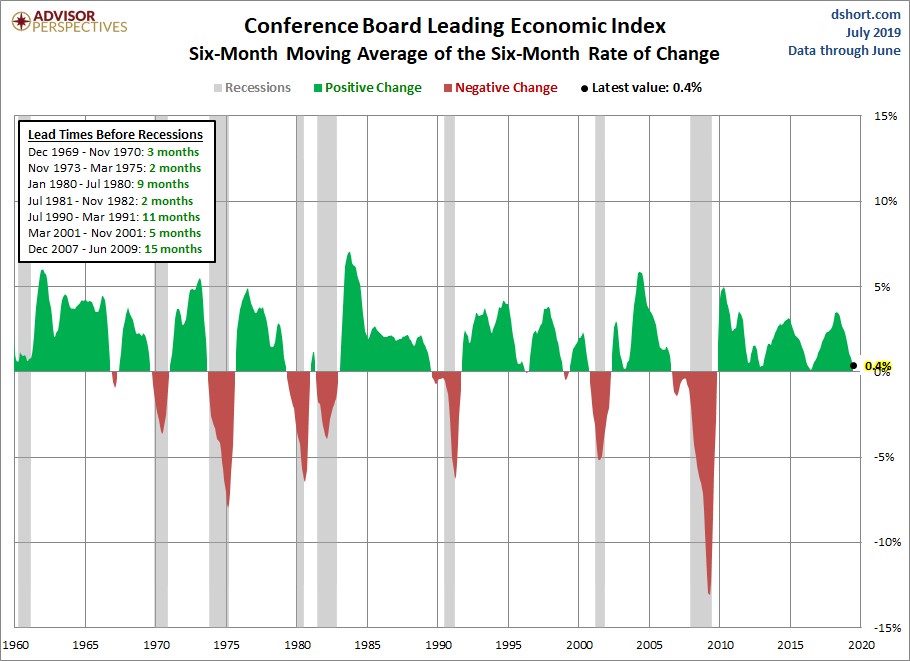

As you can see from the chart below, the 6 month moving average of the 6 month rate of change is up 0.4% which is near the lowest point of the cycle. When the index goes negative, recessions start between 2 months and 15 month later. Although, there have been some false alarms.

This index was weak in June. Because of initial jobless claims, housing permits, and new orders in the ISM manufacturing index.

Obviously, this is a weak reading. But I see a rebound in the future. Empire Fed and Philly Fed manufacturing reports rebounded. Every week in June the 4 week moving average of jobless claims rose. And in July it has fallen 2 straight weeks. Stocks are up 1.18% month to date which is another positive.

Conclusion

Fed Turns Hawkish - Many investors didn't see the need for a rate cut and expected 2 cuts this year. So we were all surprised to see such dovish statements on Thursday.

The statements on Friday, brought us back to reality. Fed, particularly Clarida and Williams were very ineffective in communicating guidance. Either they were clumsy or they disagree with the consensus.

Even still, if I disagreed with the consensus and believed in a double cut, I would preface my statements. Mostly by saying it won’t happen to avoid spooking the markets. This week explains why the July Fed meeting will at least be the most interesting one since last December.