July Empire Fed Index - Big Rebound

There was a major bounce back in the July Empire Fed Index. So, calling for a recession based on some sentiment reports from June was always a dubious proposition. Trade hurt sentiment.

In some surveys, the early June trade spat between America and Mexico had a negative impact on results. In July sentiment readings, firms will know about the deal with Mexico and the negotiations with China.

Businesses aren’t going to make the investments they were holding back on because of the tariffs just because there are now negotiations.

There will be increased optimism.

July Empire Fed Index - Positive outlooks become reality. When markets see optimism, they rally which leads to easy financial conditions. If firms see their competitors are mildly optimistic, they will be slightly more aggressive.

We aren’t at a point where uncertainty is gone and the slowdown is over. But investors expect business sentiment readings to be stronger in July than they were in June.

One of the first July business sentiment reports was the manufacturing Empire Fed survey.

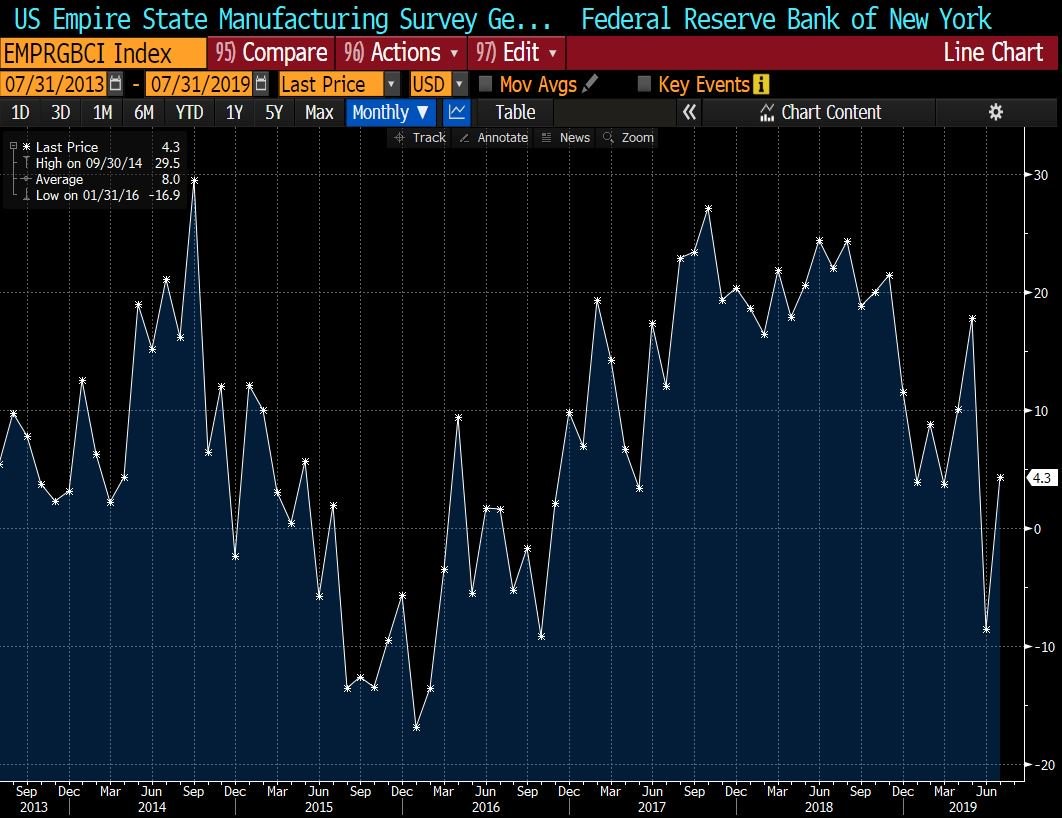

As you can see from the chart below, this index had a big increase in July as it went from -8.6 to 4.3. That beat estimates for 0.8, but it didn’t beat the high end of the estimate range which was 7.

It appears many economists anticipated a bounce back from the terrible June reading. Economists have been too optimistic as the Citi economic surprise index has been cratering. Maybe that index will rebound in July.

July Empire Fed Index - Details Of Empire Fed Index

Since the general business conditions index increased 12.9 points, it’s no surprise the details were mostly good. New orders index was up 10.5 points to -1.5. Unfilled orders index was up the most as it increased 10.7 points to -5.1. Inventories index fell 5.6 points to -10.9 which is the lowest reading since late 2017.

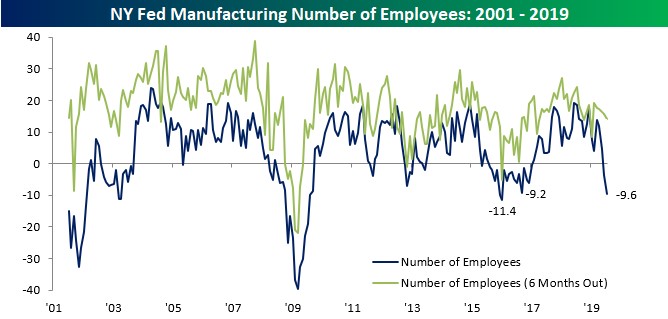

In this report, employees worked longer hours and the number of employees index fell sharply. Average employee workweek was up 6 points to 3.8.

As you can see from the chart below, the number of employees index fell 6.1 points to -9.6. As you can see, that’s the worst reading since 2016. Interestingly, the 6 month expected number of employees index wasn’t that weak. It fell 1.4 points to 14.2 which is only the weakest reading since the start of the year.

6 month expectations index was strong just like the overall index.

July Empire Fed Index - The 6 month expected business conditions index was up 5.1 points to 30.8 which is near the strongest reading of the year.

New orders index was also strong as it increased 7.6 points to 35.4. Capex rebounded solidly and technology spending was just ok. Capex index was up 8.5 points to 19 and the technology spending index was up 1.8 points to 14.6.

This report doesn’t include a quotes section. But it's safe to say sentiment improved probably because of trade news. This is good news for the ISM PMI. It was slightly better than the average of the regional indexes in June.

Specifically, the ISM-like weighting of the components of the Empire Fed index increased from 48.4 to 49. We haven’t even gotten the June industrial production report yet to find out the truth. It comes out on Tuesday morning at 9:15 AM.

Personally, I think this report will support the narrative that the economy is in a slowdown. But there’s no evidence of a recession. Consensus is for 0.1% monthly production growth and 0.2% manufacturing growth.

Fed Drives Returns

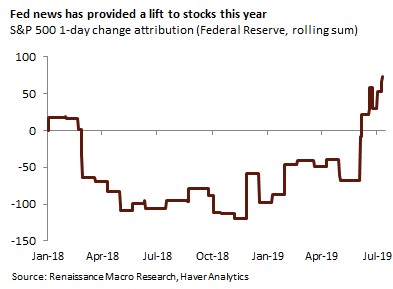

July Empire Fed Index - The stock market is pricing in the best case scenario for monetary and trade policy. It is pricing in that the slowdown won’t transition into a recession.

As you can see from the chart below, the rolling sum of the 1 day change attribution to Fed policy has spiked since June. The stock market thinks the Fed will cut rates 2-3 times in 2019. Also hat there will be a trade deal soon or at least no more new tariffs, and that the economy will rebound.

I believe the Fed will cut rates twice. Also that there will be some sort of trade deal later this year. And finally, that the economy will slightly rebound in early 2020.

There’s a theory that President Trump is trying to play up the trade war to get the Fed to cut rates. Then, after the Fed cuts rates, he will make a deal. He definitely wants rate cuts. But I don’t believe that theory as it was the Chinese who backed out of negotiations in May.

July Empire Fed Index - Back To Normal

Earnings growth is probably going to go back to normal in Q4 because the comps will be easier. According to FactSet, if earnings estimates are beaten by the average amount, earnings growth will be 1%.

That’s much lower than the long term trend, but it’s not a disaster. Stocks have rallied this year. They got very cheap last year when they fell and earnings rose sharply.

As you can see from the chart below, Q1 2019 was the bottom for earnings revisions. Estimates fell sharply in January and February. Mostly because of the tightening of financial conditions and the increased expectations for a recession late last year.

Both of which were partially caused by the hawkish Fed. Q2 earnings revisions weren’t as terrible. The bar hasn’t been lowered as much which is a good thing.

It would be bullish if Q3 estimates only fell mildly as a result of Q2 earnings season. I will be tracking this closely.

July Empire Fed Index - Conclusion

The July Empire Fed index bounced back which signals the trade news may have encouraged some manufacturing firms. It will be critical to see how weak industrial production was in June when the report is released on Tuesday.

If the report is solid, the soft data reports were much to do about nothing. Trade news seems to be hurting sentiment more than actual business, although sentiment often becomes reality.

Q2 earnings season should be solid. I will be looking at the banks’ earnings this week.