Financials Rally - Stocks Finally Rally

Financials Rally as we finally see the stock market rally. The 4 day decline wasn’t much of a losing streak. There was only bad day out of the four. The decline ended on Thursday.

S&P 500 increased 0.38%. Unlike Wednesday, this time the gains were maintained. Nasdaq increased 0.73% and Russell 2000 had an amazing day as it increased 1.9%.

Since the financials is the largest sector in the Russell 2000, it’s no surprise they were up big. KBW regional bank index increased 1.5%. It’s up 10.64% year to date. Which is underperformance this year because of how great the year has been.

VIX fell 2.41% to 15.82 and the CNN fear and greed index actually fell 1 point to 47 which is neutral. Every sector increased on Thursday except energy which fell 0.79%. Best sectors were the financials and real estate which were up 0.92% and 0.73%.

Financials increased after hours

Financials Rally - This happened because the big banks passed the Fed’s stress test and are offering bigger dividends and buybacks.

Specifically, Goldman Sachs increased its dividend from $0.85 to $1.25 and is doing a $7 billion buyback which is up from $5 billion in 2018. Its stock increased 1.17% on Thursday and 2.49% after hours.

JP Morgan raised its dividend by 13% and its buyback by 29.6%. Its stock increased 1.8% after hours.

G20 To Effect Stocks Shortly

Financials Rally - G20 summit is now underway which means Presidents Trump and Xi are negotiating a deal on trade. It appears China is insisting America lift the Huawei ban as part of the trade deal.

It seems obvious that would occur because a deal would put the two sides on friendlier footing. As of Thursday afternoon eastern standard time, there isn’t news on how the summit is going. We might need to wait until the weekend to figure out if anything was solved.

You’d think if a couple meetings were all it took to get a deal done, it would have happened already. On the other hand, it’s clear Trump has negotiated and postured in a way that made this summit important.

It all depends on if each side thinks it is getting the best possible deal now or if a further trade war will get one side a better deal in the end. Trade news/speculation will determine where stocks go in the next few trading sessions.

Jobless Claims Rise Slightly

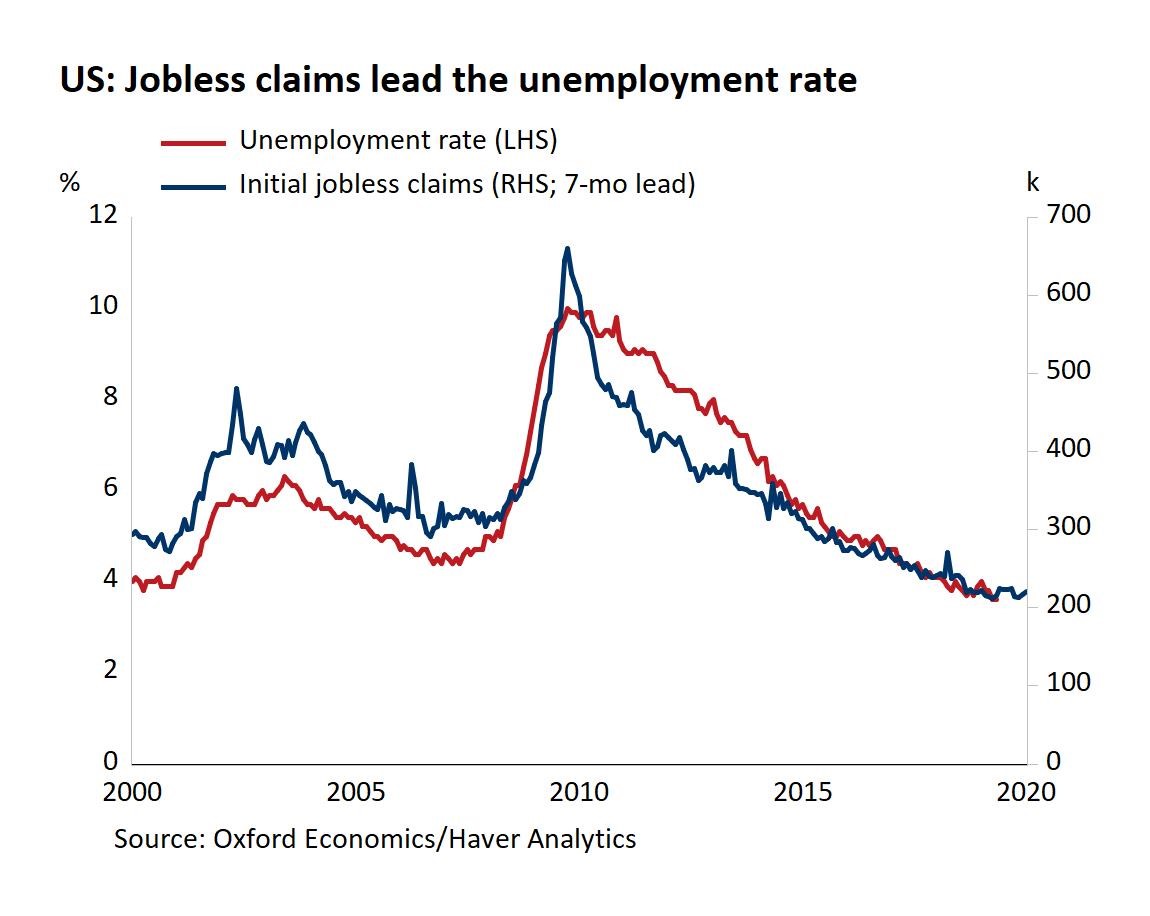

Financials Rally - Jobless claims rose from 217,000 to 227,000. As you can see from the chart below, this is a small move. This was above the consensus of 218,000 and the high end of the estimate range which was 222,000.

The increase was probably related to the end of the school year. It’s nothing to worry about. The 4 week moving average increased from 219,000 to 221,250. That’s the 8th straight week it has been in between 215,000 and 225,000. Continuing claims rose 22,000 and the 4 week moving average rose 6,500 to 1.687 million. That’s still very low.

Oxford Economics is predicting the unemployment rate will fall 0.1% to 3.5% in June.

Financials Rally -I see the May jobs report being revised higher and the June report showing about 100,000 jobs created.

Usually the ADP report isn’t followed closely. But this time investors will be focused on small business job creation in this report. If small businesses don’t create jobs, the bears will feast. I don’t know if that will hurt stocks at all. But it will cause a stir amongst the bears. Always follow the ADP report, but the BLS report takes precedent.

Kansas City Fed Index At 0

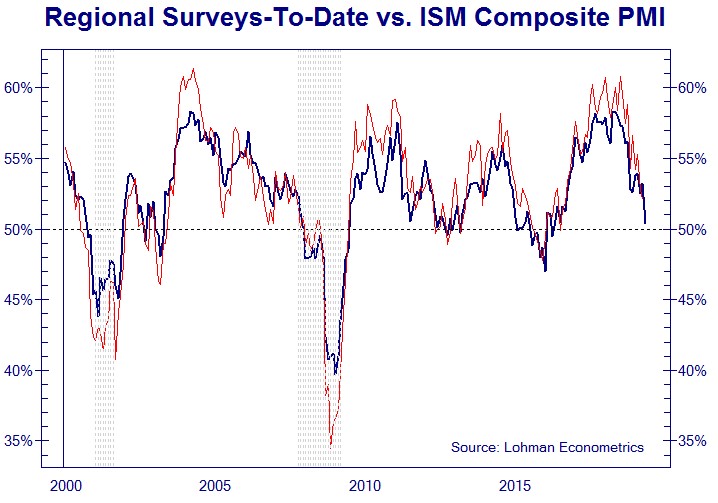

Financials Rally - Kansas City Fed manufacturing index fell from 4 to 0 which missed estimates for 3. With all the regional Fed manufacturing reports in, I think the manufacturing ISM PMI will fall from the 52.1 reading it had in May. The report comes out next Monday.

As you can see from the chart below, the regional Fed surveys are highly correlated with the PMI. They are consistent with a PMI of slightly above 50. If the PMI falls below 50, it will cause investors to sell stocks.

Production index fell from 2 to -3 and volume of shipments index fell from -2 to -7. New orders index increased from 4 to 5. There appears to be a bottleneck in shipments in this Fed district as well as the supplier delivery time index fell from 9 to -3. Inventories for finished goods and raw materials, however, fell from 8 and 0 to 6 and -3.

Financials Rally - Expectations index didn’t see much of a decline like it has in other reports

The 6 month expected composite index fell 1 point to 11. Production index was up 2 points to 22. Volume of new orders index was up 4 points to 16. Tied for the biggest decline was capex as it fell from 27 to 11.

Now let’s look at the comments from this report to see why the current index fell modestly. Out of the 11 selected comments in this report, 4 mentioned China or tariffs.

One firm stated, “Tariff threats lead to instability and we are always looking for a stable supply of product and raw material. China is a question mark and some sourcing now comes through Mexico or even Europe.” This index, like others, would increase if there was a trade deal.

Financials Rally - Conclusion

Financials will rally on Friday because of the dividend and buyback boosts many of the biggest players made because they passed the Fed’s stress test.

Goldman Sachs had a massive increase in its dividend. That will support its stock if it falls in a bear market.

The G20 summit will dominate the headlines in the next few days as we find out if a trade deal is more or less likely. Anyone who pretends to know what will happen isn’t telling the truth. No one has an edge which means the playing field is level.