Stocks Anticipate - Slight Rally As The S&P 500 Inches Closer To A New Record

On Monday, S&P 500 increased 0.1% which was enough to hit a new closing high for 2019. It is inching closer to the September high. It's about 23 points away from that threshold. It made sense that the market was quiet Monday because the next 2 weeks will be the busiest of this earnings season. Usually markets are quiet before big events.

VIX increased 2.73% to 12.42 even though stocks rose. That didn’t stop the CNN fear and greed index from increasing 1 point to 71.

As you can see from the chart below, Nomura has a similar calculation of investor sentiment. The chart shows optimism is the highest since September 2018 when the market was at its record high. Optimism is just below the January 2018 peak. This level of optimism is causing some analysts to predict a triple top in the S&P 500. I see a mild correction coming in the next few weeks rather than a new bear market.

Stocks Anticipate - Small Caps Have Underperformed

Nasdaq increased 0.22% and the Russell 2000 fell 0.36%. Russell 2000 underperforming large caps is nothing new.

As you can see from the chart below, the Russell 2000 divided by the S&P 500 is falling. The ratio fell from the market peak in September to the trough in December.

In the beginning phases of this rally up until late February, small caps outperformed. Small caps have underperformed since then. Some view small caps as a leading indictor for stocks and the economy. It’s certainly possible this indicator is correct, but it’s not like small caps are down on the year.

This is similar to how consumer discretionary stocks underperformed utilities earlier in the year. Both were up, but utilities were up more. This isn’t an issue with the dollar as the dollar index hasn’t moved much in the past 6 months. It is at $97.30 which is the high end of its recent range.

I think this big cap outperformance is occurring because international and tech stocks have been doing well. During the earnings estimate collapse in the first 2 months of the year, investors feared the worst about the global economy and tech earnings. Now that those fears have ended, tech and multinational firms are trouncing the Russell 2000.

Stocks Anticipate - Energy Rallies With Oil

Speaking of sector performance, energy and communication services were the biggest winners on Monday as they increased 2.05% and 0.72%. Energy loves the increase in oil prices as WTI crude oil is now at $65.58. Oil increased on Monday because America ended all of Iran’s sanction exemptions.

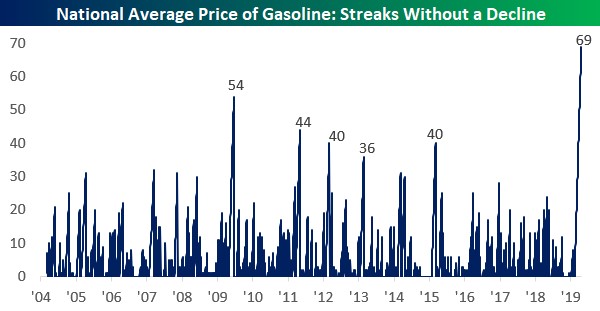

As you can see from the chart below, the average national price of gas has increased 69 straight days. That’s the longest streak ever by far. The two worse decliners were real estate and materials which fell 1.05% and 0.67%. Even though this was an up day, 7 sectors fell and only 4 rose. Selling was broad based and the rally was heavily focused.

Stocks Anticipate - Next 2 Weeks Are Crucial

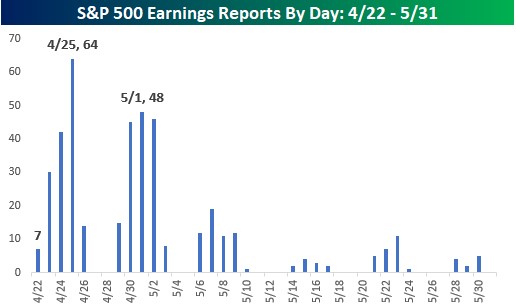

As you can see from the chart below, the next 2 weeks of earnings season are the biggest of the quarter.

It’s not a surprise stocks barely moved because Monday wasn’t one of the big days. The most important day will be Thursday when 64 firms report results. 86 firms have reported results so far. 77% of these firms have beaten EPS estimates. EPS growth is 5.32% which is impressive for a quarter that was supposed to show declines.

52% of firms have beaten sales results which is below average, but understandable because revenue estimates were challenging. Sales growth is 2.88% which is below FactSet’s blended results.

Earnings Scout data has higher EPS growth than revenue growth, implying margins increased. FactSet has higher revenue growth, implying margins fell. Either way, it’s safe to say this has been a solid quarter so far. If it continues, stocks should have a great 2 weeks in which they potentially reach new record highs.

Stocks Anticipate - Fed Funds Rate Increases

Fed is 8 days away from its next meeting in which it will likely not make any changes to the Fed funds rate. The CME Group website shows there is a 99.5% chance rates stay the same.

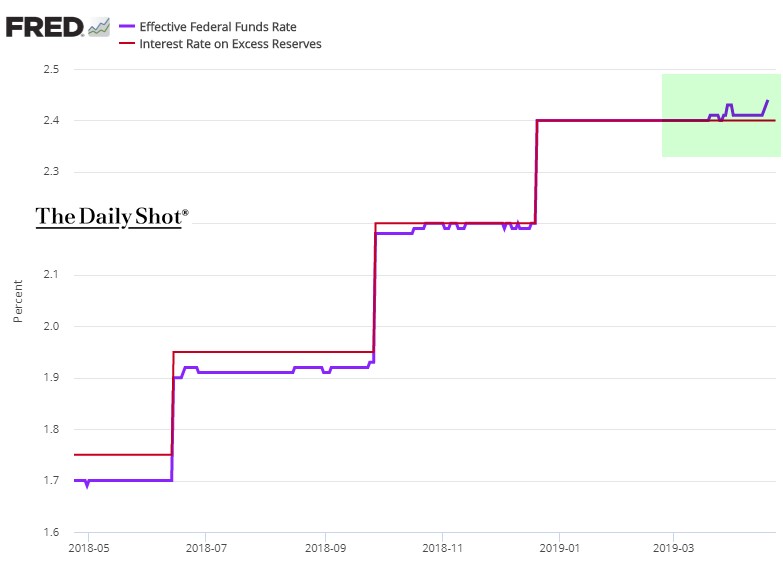

That being said, the chart below shows the effective Fed funds rate has increased recently. It had been at 2.4% for a few months ever since the last rate hike. However, recently it has increased from 2.41% to 2.44%. Fed is losing control of the Fed funds rate. It is supposed to be in a range between 2.25% and 2.5%.

Although it’s very unlikely, it would be big news if this rate gets above 2.5%. The Fed could mention this in its statement or silently change the control mechanisms that affect the rate. Reporters will probably ask about this, but the Fed might not respond.

Stocks Anticipate - Housing Starts & Permits Miss Estimates

Even though the MBA applications report shows housing applications are increasing at a solid clip, the March housing starts and permits were very weak.

Housing starts were 1.139 million which fell from 1.142 million and missed estimates for 1.23 million. Housing permits were 1.269 million which fell from 1.291 million and missed the consensus for 1.3 million. Two of the most important stats from this report were that single family completions increased 11.9% monthly to a rate of 938,000 and that single family permits fell 1.1% monthly and 5.1% yearly. Every region had negative yearly starts and permits growth.

The housing market is usually the first area of the economy to turn before a recession hits. With this weak data being released, it’s fair to say the recession warning is still in play. That being said, the housing market isn’t nearly as important as it was last cycle and there’s less room for it to fall.

Without the yield curve inverting fully, this indicator is alone in calling for a recession sometime in 2020-2021.