Redbook Same Store Sales - Big Tuesday Rally

Redbook same store sales - If the market’s goal is to rally past the September record high without getting too overbought, the market is acting smartly. Corrections in early March and last Friday took some froth out of it. CNN fear and greed index is only at 54 which is neutral. Yet S&P 500 is only down about 1.3% from its high on Thursday.

At its high, the CNN index was getting close to extreme greed. To be clear, if stocks increase at the pace they have since Christmas Eve, they will become expensive regardless of whether there are healthy corrections. S&P 500 increased 0.72%, Nasdaq increased 0.71%, and Russell 2000 was up 1.01%. VIX fell 10.10% to 14.68.

Redbook Same Store Sales - Sector Performance

Every single sector was up. The best 3 sectors were energy, financials, and consumer staples as they increased 1.45%, 1.13%, and 0.85%. Financials rallied because treasuries had a modest correction to their recent explosive rally. Consumer staples did well. Investors are still fearful of a recession even though the ‘risk on’ trade dominated Tuesday’s action.

We are seeing a pleasant sector rotation where the consumer staples and utilities do well, but everything rallies. Since Thursday March 7th, the XLP consumer staples ETF is up 3.69% while the S&P 500 is up 2.53%. This outperformance is typical for the market after the yield curve inverts.

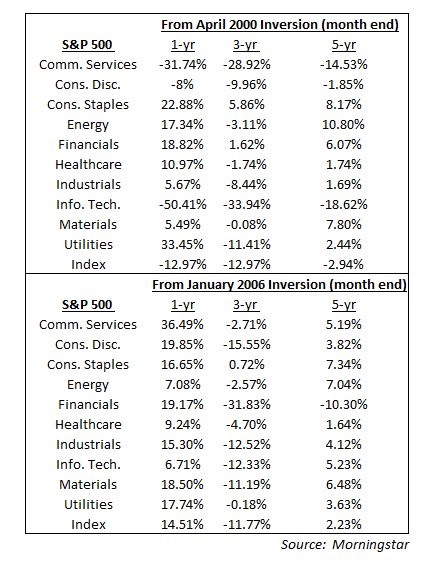

As you can see from the chart below, consumer staples is the only sector that had positive returns 1 year, 3 years, and 5 years after the past 2 inversions.

Financials like a steepening yield curve. The financial crisis is an outlier because the banking system nearly fell to its knees. In the year following the past two inversions, the utilities sector increased 33.45% and 17.74%. It’s a double whammy for the curve to invert and for yields to fall. This explains why utilities are up 13.36% year to date.

Redbook Same Store Sales - Update On Treasuries

Treasuries sold off on Tuesday, but let’s look at the latest pricing which includes Tuesday night. The 10 year yield is at 2.41% which is only 1 basis point more than the Fed funds rate. 2 year yield is at 2.24% which is a remarkable 16 basis points below the Fed funds rate.

Just 2 weeks ago, I thought it would be impossible for the 2 year yield to fall below 2.3% without the Fed signaling for rate cuts. The Fed funds futures market is fairly certain there will be a rate cut this year as it shows there is a 67.4% chance of at least one cut. I need to see more economic weakness to change my mind as I still think the Fed will keep rates the same.

If the economy follows the ECRI leading index’s yearly growth rate at the start of the year, there will be a severe slowdown which narrowly misses recessionary territory in Q2 and Q3. ECRI leading index’s growth rate fell below any reading in the 2015-2016 slowdown and some even consider that to be a mini-recession. The saving grace for the economy in Q2 2019 is that low rates should help the housing market and increasing real wages should help the consumer.

Redbook Same Store Sales - Revives Itself

The Redbook year over year growth reading showed the consumer picked up spending in late March. The yearly growth rate in the week of March 23rd increased from 4.9% to 5.3%. When the yearly growth rate was 4.2% at the start of March, I was beginning to get worried. It didn’t make sense to see spending growth falling so rapidly given the strong wage growth. But that doesn’t make it impossible.

Keep in mind, both 4.2% and 5.3% are solid readings. The problem was the speed at which growth was slowing. Now that it has stabilized, we can look for solid consumer spending growth heading into Q2. This March is expected to be weak for retailers because Easter is late this year as it is April 21st.

That shouldn’t matter to investors as the total year results won’t be affected by this. If your stock lives and dies off the timing of Easter, you are investing in a weak company.

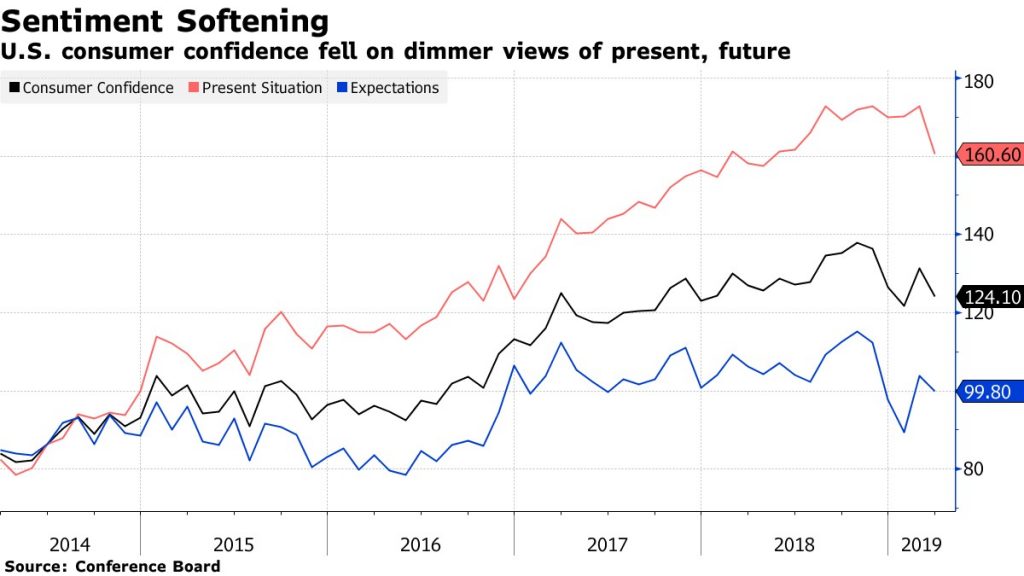

Redbook Same Store Sales - Consumer Confidence Falls

The Conference Board consumer confidence reading fell unlike the University of Michigan reading. This weakness is actually in tune with Redbook’s report because the cutoff date for this survey was March 14th and Redbook showed same store sales growth was the weakest at the beginning of the month.

As you can see from the chart below, the index fell from 131.4 to 124.1 which missed estimates for 133 and the low end of the expected range which was 130.

Present Situation index decreased from 172.8 to 160.6 and the Expectations index decreased from 103.8 to 99.8. The only good news from that is the difference between current and expectations fell. However, that’s not the way we want to see that spread decline. There was a 2.5% increase in the percentage of respondents who said the economy is bad; it resides at 13.6%.

Redbook Same Store Sales - Biggest news from this report was the change to the assessment of the jobs market.

Percentage of consumers saying jobs are hard to get increased 2% to 13.7% and the percentage of consumers saying jobs are plentiful fell 3.7% to 42%. The labor differential fell to the lowest point since July. Some analysts only follow this part of the report. They believe the only thing consumers know about is the labor market; the rest is conjecture they say.

This weakness confirms the poor February jobs report which showed only 20,000 jobs added. However, jobless claims remain low. The March BLS reading will be the most important employment report in a while.

Buying plans improved even though consumers said the labor market got worse. There was a 1.7% increase in those saying they plan to buy an automobile. That’s interesting because the auto industry has been very weak this year.

Buying plans for housing increased 0.7% to 6.1%. That increase may have been spurred by the collapse in rates. Finally, inflation expectations increased 0.2% to 4.5% which is weird because bond yields have been plummeting.