Bear Market Repealed Almost Fully

Bear Market Repealed on Another solid rally on Friday that brought the S&P 500 very close to its record high in September. And it fully repeals the quick bear market.

Investors feared the worst in December. But now it’s clear America is only in a slowdown and is outperforming most of the rest of the world. Even so, I’m not on board with this rally because stocks have gotten expensive.

That’s what happens when earnings growth is in the low single digits and stocks rise 11.84% in slightly more than 2 months.

Friday was important to technicians. It was the first time the S&P 500 closed above 2,800 since November. It was up 0.69% and closed at 2,803.69.

S&P 500 is only down 4.3% from its record September close. There have been 3 failed mini rallies since September when the S&P 500 closed near this level.

With today’s close, the S&P 500 has surpassed one of them. It needs to rise slightly over 10 points to surpass the highest one.

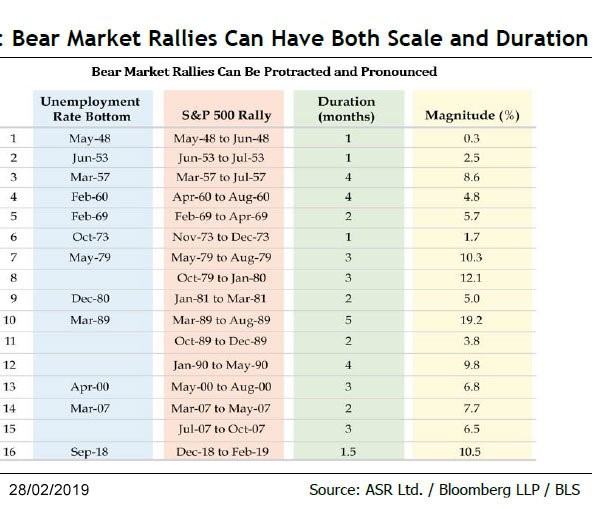

The table below shows a list of the most pronounced bear market rallies. S&P 500 is within a few percentage points of no longer being in a bear market.

As you can see, the longest bear market rally was 5 months where it increased 19.2%. The point of this chart is to show it’s possible this is still only a bear market rally. I don’t agree with the concept that the September 2018 unemployment rate was the bottom.

The rate is up 3 tenths since that low, but the labor participation rate has increased. Also, the unemployment rate was boosted by the government shutdown last month. The unemployment rate’s increase is only an issue, in my opinion, if the labor force participation rate starts to fall.

Bear Market Repealed - Huge Winning Streak Brings Us An Overbought Market

The stock market is extremely overbought. It’s rallying with mixed economic data at best and the leading indicators turning down.

Plus, earnings estimates signal low single digit estimate growth in the next 3 quarters. I’m not bearish enough to call it an earnings recession, but multiples are expanding rapidly.

This doesn’t seem like the ideal scenario to go overweight stocks, but they keep levitating higher.

CNN fear and greed index is now at 72 which signals greed. It is a few points away from hitting extreme greed. Only the subcomponent which measures momentum by looking at the S&P 500’s 125 day moving average signals fear.

AAII investor sentiment poll has bulls at 41.6% and bears at only 20%.

That's the lowest percentage since January 2018 which will undoubtedly be the sentiment top. Bulls hit about 60% then, so only the bear figure is close to the extreme level in January. It’s still not a good sign to see the shorts leaving the market.

On Friday, the Nasdaq was up 0.83% and the Russell 2000 was up 0.89%. Russell 2000 is now up 17.88% year to date.

As you can see from the table below, the Nasdaq is on a 10 week winning streak which isn’t necessarily bad for near term returns.

Median returns in the following 3 months are 8.44% which is quite impressive. Eventually, the momentum wanes at the one year mark as median returns are just 6.17% after a year which is below average. Unsurprisingly, stocks can’t rise at an accelerated clip forever.

Best 2 sectors were energy and healthcare which increased 1.81% and 1.41%. Worst 2 sectors were materials and consumer staples which increased 0.16% and 0.17%.

Kraft Heinz stock is down 33% since February 21st. Obviously, accounting irregularities are a one off issue, but many consumer staples names in the food industry are facing similar declines in brand loyalty. These firms were once consistent growers, but now below market multiples are justified as they lose market share quickly.

Bear Market Repealed - Terrible Q1 GDP Growth Coming

The difference between S&P 500 returns are GDP growth is going to be stark if Q1 continues at its current rate. Atlanta Fed Nowcast projects 0.3% Q1 growth.

CNBC rapid recap has the median of 6 estimates at 1.4%. The chart below shows the Atlanta Fed usually goes through weak spells in March and April and then recovers. There have been a bunch of weak first quarters in this expansion, but that doesn’t excuse the current weak situation.

St. Louis Fed Nowcast is once again the most optimistic as it expects 2.32% growth. NY Fed’s Q1 Nowcast fell from expecting 1.2% growth to just 0.88% growth.

Housing starts, wholesale inventories, and real PCE metrics were the biggest reason why growth estimates fell. It’s notable that wages and salaries growth was solid in December and January. All isn’t lost, but this is still a period of weakness.

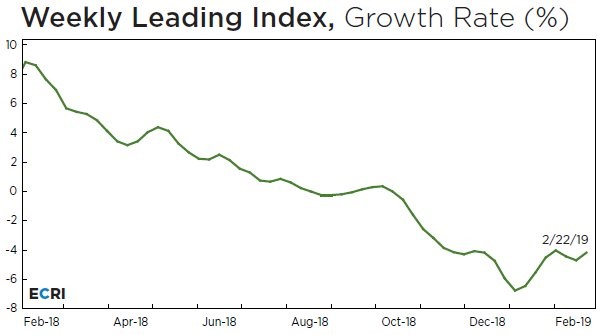

Bear Market Repealed - ECRI Leading Index Improves

ECRI leading index increased 0.7 to slightly over 144. Year over year growth rate increased from 4.7% to 4.2%. Growth has been in a tight range for about 5 weeks.

It’s not ideal to see this because yearly comparisons are getting much easier. If the index increases slightly, it could reach positive growth in March because of how easy the comparisons get. This leading index isn’t good enough yet for me to say the economy will recover in the 2nd half and that buying stocks is a no brainer.

Stocks are leading a this index which is supposed to be 6 months ahead of the economy. Keep in mind, that last statement is only true if this index actually rebounds which is far from certainty.

Bear Market Repealed - Conclusion

This is one of the strongest rallies many investors, including myself, have ever seen.

Stocks are rallying even though Q1 GDP growth is about to be below 2% and possibly will be negative. Many indicators signal stocks can continue to increase even though they have excessive momentum. But I’d rather stay away from a euphoric market when earnings growth is small and the leading indexes still show economic growth will worsen in the coming months.