Fed To End Balance Sheet Reduction In 2019

The Fed released its Minutes from its January meeting on Wednesday. Even though it’s very likely the it won’t raise or cut rates this whole year. There were still many interesting tidbits worth considering.

A headline from this report was Fed plans to end its balance sheet unwind by the end of the year.

It stated, "Almost all participants thought that it would be desirable to announce before too long a plan to stop reducing the Federal Reserve's asset holdings later this year.

Such an announcement would provide more certainty about the process for completing the normalization of the size of the Federal Reserve's balance sheet."

Investors were shocked by this. We thought the it would discuss how it would unwind the balance sheet this year. And also end the program in 2020 or2021.

That was the initial plan. But everything changed after the Fed noticed the stock market negatively reacting to its balance sheet plans.

Powell said these were on autopilot late last year. This comment made the market think the Fed was, "not fully appreciating the tightening of financial conditions and the associated downside risks to the U.S. economic outlook that had emerged since the fall.”

Balance Sheet Is A Tool: It Will Stop Falling At $3.5 Trillion

It's amazing that a plan set to be in place for over a year was scrapped based on one comment. That’s why the Fed chooses its words very carefully.

It takes years for them to carefully introduce hawkish language and policy. It takes a few weeks to switch to dovish policy. To be fair, the size of the correction wasn’t in tune with the economy and earnings. Stocks probably should have fallen 10% to 15%.

I’m surprised the Fed is utilizing the balance sheet to set dovish policy. Just last year it stated it wouldn’t alter the unwind based on changes to the economy.

It's not fair to assume the balance sheet has power over the stock market and economy. Especially just because stocks fell when Powell said the balance sheet unwind was on autopilot. The market may have fallen because the comment made it seem like Powell was ignoring the vicious decline.

Keep in mind that these Minutes are from the late January meeting which was dovish and caused stocks to rally. The Fed extended its interest rate guidance to the balance sheet.

Balance sheet stance solidifies the guidance that the Fed won’t hike rates further this year.

Currently there is an 87.2% chance rates will stay the same this year. There is a 11.7% chance rates are cut and a 1.1% chance rates are raised.

The balance sheet is currently $4 trillion. If the $50 billion per month unwind continues until the rest of the year, it will get to $3.5 trillion.

Wall Street expects about $500 billion of the bonds on the balance sheet to roll off it. To be clear, I had expected the balance sheet to end this unwind between $2.5 trillion and $3 trillion. Now that the Fed gave this guideline, it can’t back out or else it will lose credibility.

That’s why the Fed likes to speak in vague terms because they don’t make themselves beholden to certain policy.

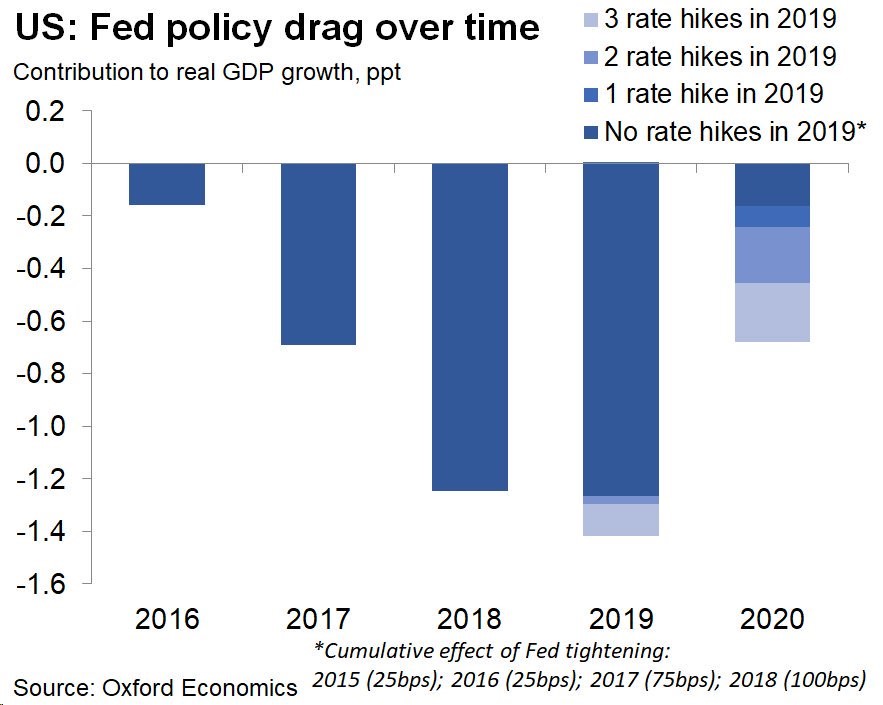

GDP Drag From Rate Hikes

To be clear, the Fed shouldn’t change the dovish stance it started taking in late December if it is following the economy. If it follows stocks, then hawkishness should resume. I think the rate hikes from last year are still being digested.

The effect of the hikes last year will limit GDP growth which is already being hurt by the global economic slowdown particularly in Europe and China. Another few hikes could push America into a recession.

As you can see from the chart below, the cumulative effect of Fed tightening on GDP growth has gotten more negative as the Fed has raised rates.

In 2018, the economy was bolstered by the tax cut which helped it survive the 1.2% GDP growth drag from rate hikes. As the chart shows, 3 hikes in 2019 would push the negative effect to 1.4%. Hikes this year would cause a larger relative drag in 2020. No hikes would hurt GDP by less than 0.2% and 3 hikes would hurt it by over 0.6%.

Fed - Inflation & Future Policy

On future policy, the Fed stated in its Minutes, "Participants pointed to a variety of considerations that supported a patient approach to monetary policy at this juncture as an appropriate step in managing various risks and uncertainties in the outlook”.

Patient was the word which caused much hoopla in the Fed’s January statement as investors decided the Fed wouldn’t hike rates this year. That was different from the previous guidance for 2 hikes. To be clear, the March meeting will include specific guidance on hikes. At this point, I would be shocked if the Fed expects to hike rates even once this year.

The Fed expects to end this patience if uncertainty ends. But it would take a while for the Fed to get the market to start thinking abut rate hikes again. I see this as the open possibility for hikes in 2020.

Fed said it would be reviewing the inflation softness, government shutdown, and fiscal policy path. I could see the Fed hiking rates in 2020 if growth accelerates, pushing inflation higher.

Fed - Balance Sheet Changes Might Not Matter

I think changes to the balance sheet policy don’t affect stock prices as much as people think, but I still need to discuss this in case some readers disagree.

Furthermore, the balance sheet and interest rate policies are intertwined. It’s all monetary policy guidance which is important. The Fed’s Minutes stated primary dealers agree with me; they have little belief that the balance sheet reduction was playing havoc with markets in Q4.

One reaction to a comment about being on autopilot shouldn’t make the market’s reaction to the balance sheet reduction since October 2017 irrelevant.