S&P 500 - The Incredible Rally Continues

The rally this year has been relentless and unbelievable. It has wiped out the shorts who were calling for a recession in 2019. The S&P 500 is now up 6.54% year to date as it has surpassed many year end forecasts within the first month.

On Friday the S&P 500 was up 1.32%, the Nasdaq was up 1.03%, and the Russell 2000 was up 1.04%. The VIX only fell 1.44%. This pushed the CNN fear and greed index out of the fear category for the first time since October. It increased from 44 to 51 as it is now at neutral.

The S&P 500’s 14 day relative strength index increased to 57.77 which puts it close to being overbought. I think the market is extremely overbought, and I now recommend shorting stocks. I think stocks have a high likelihood of being lower in the next month.

S&P 500 - Broad Based Extreme Rally

The stock market has gotten a lot more expensive in just the past 3 weeks. S&P 500 started the year with a 13.92 forward PE multiple and now has a 15.11 PE multiple.

The stock market started the year anticipating a recession in 2019 and quickly took it off the table. While I don’t see a recession occurring soon, stocks have rallied too far too quickly.

25 stocks in the S&P 500 have rallied 20% or more this year. 177 are up at least 10% and 468 are up this year. This has been a situation where a rising tide has lifted almost all ships.

The best sector this year has been energy as it is up 11.19%. The financials are up 9.03% on decent earnings. The utilities are only up only 0.43% because the risk on trade has dominated.

On Friday, every sector was up. The best 2 sectors were industrials and energy as they increased 1.86% and 1.93%. Industrials likely rallied because of the great industrial production report I discussed in a previous article. All 3 of the major indexes have had 4 straight weeks of gains. They have had the biggest 4 weeks of gains since October 2011.

S&P 500 has had the best 13 trading day start to a year since 1987.

In 1987, the S&P 500 increased 11.1% in the first 13 trading days. It was up 5.1% last year. Last year is a perfect example of how the start to the year doesn’t always mean the whole year will be great. The 14% decline in Q4 took away all the 2018 gains.

As of early Friday afternoon, the S&P 500 was up 13.4% in the past 20 days. Those returns are in the 99th percentile since 2009. That’s probably the best argument in favor of shorting stocks. I usually, look at the fundamentals and price action to formulate my opinion, but when stocks move way too far too quickly, they always correct regardless of the fundamentals.

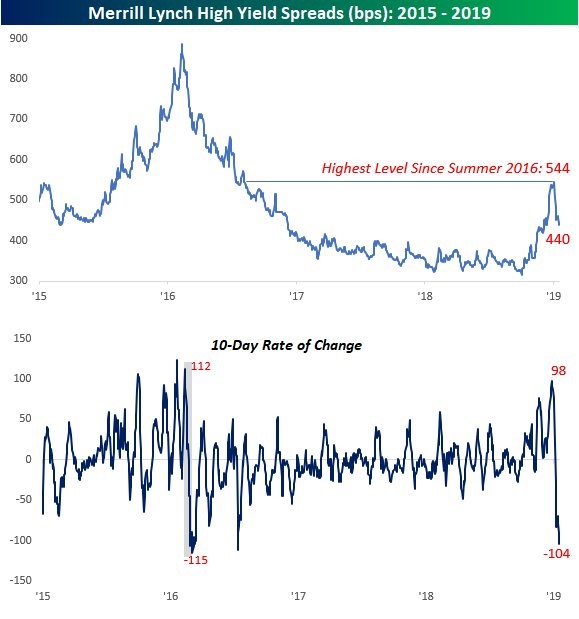

S&P 500 - Major Reversal In High Yield Spreads

As you can see from the chart below, high yield spreads have tightened from 544 basis points to 440 basis points.

Even though the yield spread never got close to where it was in 2016, the 10 day rate of change was almost the same. It recently fell 104 basis points and it fell 115 basis points after the peak in early 2016. The peak to trough in the 10 day rate of change was almost the same as well.

It’s interesting to see how the yield spread came nowhere close to the peak in 2016 even though stocks had a larger correction. Investors were worried about small caps because of rising yields and rising spreads, but both turned out to be false scares as yields have fallen sharply and the spread has tightened.

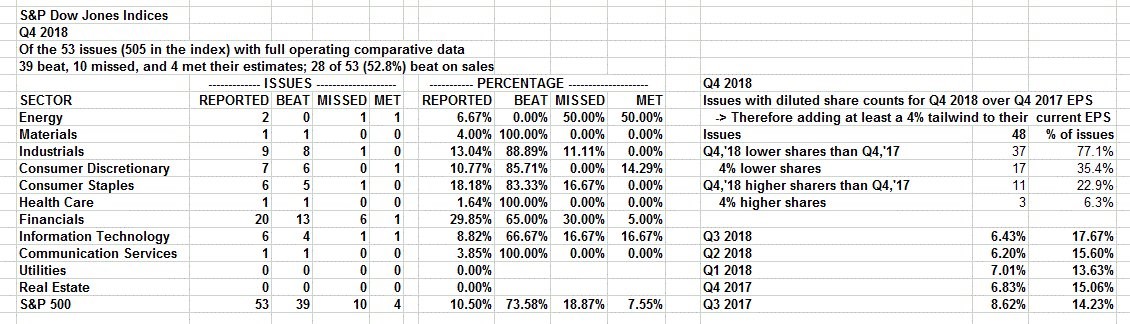

S&P 500 - Latest Q4 Earnings Results

This was an important week for the financial sector’s earnings. Next week starts the barrage of earnings where we test the latest rally.

So far, stocks have done well after they have reported earnings. Even though Netflix missed revenues and reported very weak guidance, the stock only fell 3.99% which is nothing compared to its rally since Christmas Eve.

The table below reviews the latest earnings results. It includes 53 companies out of 505 which is 10.49%. As you can see, 29.85% of financials have reported results. 65% of them beat estimates which is below the overall average of 73.58%. The record buybacks in 2018 are a big tailwind to EPS growth as 77.1% of issues have lower share counts in Q4 2018 than Q4 2017.

Only 52.8% of firms have beaten sales estimates which isn’t great. As I have mentioned often, guidance is even worse. Earnings reports I will be watching next week are Intel and Starbucks on Thursday and DR Horton on Friday. Major internet names report the week after that.

S&P 500 - Potential Trade Deal In The Works?

The main reason stocks rallied so heavily on Friday even though they were overbought is because it appears America and China are closing in on a trade deal.

This news explains why I think shorting stocks makes sense. A big reason to avoid shorting stocks was this potential positive news event. Now that the genie is out of the bottle, it’s ok to short. I don’t see any way stocks rally if the government shutdown ends because it has had no effect on stocks so far.

Specifically, China is promising a 6 year import boost of American products that eliminates the trade deficit by 2024. China plans to buy a combined $1 trillion worth of American goods.

The trade deficit with China was $323 billion in 2018. Other big news is China’s top trade negotiator is going to visit the White House on January 30th for 2 days of trade talks.

That’s right before the Chinese New Year on February 5th. Personally, I think there is a 0% chance the trade deficit is eliminated in 6 years. However, this doesn’t matter for stocks in the short term. The most important thing for stocks is there is a deal which opens up trade between the 2 countries.