Powell Statement - Huge Rally On Powell’s Speech

Powell’s speech followed along with what the vice chair stated earlier in the week. It wasn’t a policy change. But the stock market accepted it as a dovish turn.

Predicting how markets react to Fed statements is tough. If I would have had the speech a few hours in advance, I wouldn’t have been able to make a high confidence prediction either way.

The S&P 500 rallied 2.3% which pushed the CNN fear and greed index up 4 points from 19 to 23. It’s still barley in the extreme fear category.

It’s amazing to see that reading with such positive momentum in the past few days. It may be because the stock market is still acting like it’s in a correction or bear market. There have been wild swings.

Some investors think the stock market is solely responding to Powell’s statements. Remember, it fell after his hawkish statement in October. That’s like looking at the market with blinders. There are obviously other factors that impact stocks.

Nasdaq increased 2.95%, and the Russell 2000 increased 2.51%. VIX fell 2.79% to 18.49. It was a traditional ‘risk on’ day where investors piled into stocks. The Fed supposedly became dovish.

Technology and consumer discretionary stocks exploded higher. These sectors were up 3.44% and 3.23%. Utilities were down 0.12% as you’d expect.

Powell Statement - Didn’t Change Much

Sometimes the market action makes no sense. This is one of those times. The Fed usually doesn’t make big changes to its policy in its speeches. The Fed makes small alterations which sometimes cause wild swings in the market.

Many prognosticators assumed Powell ‘blinked’ or changed policy because stocks went up. That’s certainly why stocks did well, but the logic doesn’t make sense.

Those saying Powell ‘blinked’ claim he said the Fed funds rate is just below neutral. However, Powell actually said rates are just below a broad range of estimates of what neutral is.

No one knows what the neutral rate is. The FOMC has a range of estimates for the neutral rate. In September, the Fed got rid of the point in its statement where it claimed policy was accommodative because rates are close to the range of rates which could be considered neutral. Powell made the same point in his speech.

Powell Statement - The market acted as it he suddenly became a dove.

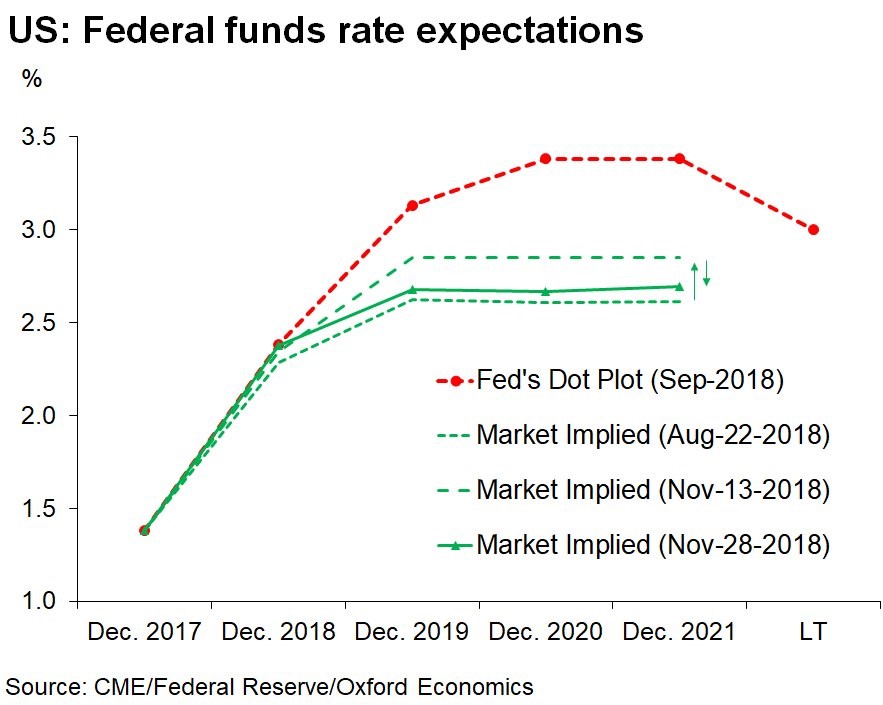

Range of rates the Fed considers neutral is from 2.5% to 3.5%. Since rates are now between 2% and 2.25%, it’s accurate to say rates are just below the range of estimates which FOMC members consider neutral.

Fed is 3 hikes away from the middle of the range and 5 hikes from the top.

Therefore, no reasonable person should expect the Fed to be done with its hikes after December based on Powell’s speech.

To be clear, it’s possible to believe the December hike is the last one. But that’s not what Powell stated.

As you can see from the chart below, the market is still expecting fewer hikes than what the dot plot projects.

Powell Statement - Fed Fund Futures & Treasuries

The Fed funds futures market gave the chance of a rate hike in December higher odds after Powell’s statement.

Stocks rallied on a dovish speech. But the futures market sees it as slightly hawkish.

One way to look at this speech is to say Powell didn’t make a change, but the stock market’s rally made a hike more likely. The only news here is the stock market’s exuberant reaction to no policy change. Chances of a rate hike increased from 79.2% to 82.7%.

The 10 year bond yield is now at 3.05% and the 2 year bond yield is 2.8% which makes the difference between them 25 basis points. That’s 3 basis points of steepening.

It remains in the range it has been in for a few months. The closest the differential came to inverting was 18 basis points in August.

Powell Statement - Stocks Won’t Make New Highs

This huge rally on Wednesday doesn’t mean the fundamentals have changed.

The same cyclical weakness is in place as before this big rally. I think this rally is unjustified. It’s not even like stocks rallied because America made a trade deal with China. That would justify a rally more than no change in Fed policy.

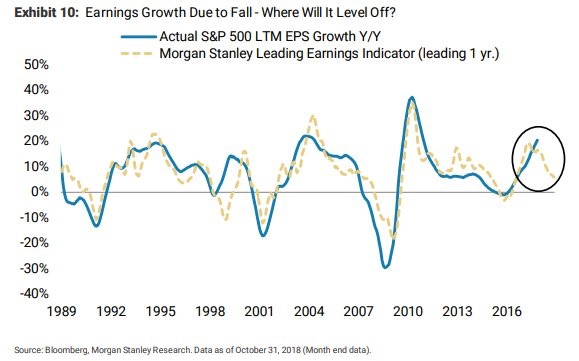

As you can see from the chart below, the Morgan Stanley leading earnings indicator expects earnings growth to slow rapidly. This is consistent with the recent decline in earnings estimates.

It’s also like the ECRI leading index which is down 3.7% year over year.

Powell Statement - Good MBA Weekly Applications

The MBA mortgage applications index for the week of November 23rd showed strength.

However, this is a volatile report, so don’t think of this as a shift in the trend. Existing home sales posted the slowest year over year growth since 2014 and new home sales posted the slowest year over year growth since 2011.

Week over week purchase applications were up 9% on top of a 3% increase last week. The refinance index was up 1% on top of a 5% decline last week. Overall, the composite index was up 5.5% after it declined 0.1% last week.

Unadjusted purchase applications were up 2% year over year. The seasonally adjusted data had a large adjustment because of the Thanksgiving holiday. Meaning, this data isn’t as reliable as it normally would be.

Refinancing’s share of mortgage applications was down 0.6% to 37.9% which is the lowest reading in 18 years. Average interest rate on a 30 year mortgage fell for the 2nd week in a row. It fell 4 basis points to 5.12%.

Powell Statement - Conclusion

Stocks were wrong to rally based on Powell’s speech because he didn’t make any changes.

The Fed is now even less likely to keep rates unchanged at its December meeting now that stocks increased sharply. I expect a rate hike in December.

The more rate hikes we get in 2019, the greater chance the yield curve will invert, and the economy will fall into a recession in 2020.