Hawkish Hike

This was a hawkish hike as the Fed increased its economic projections. We no longer need to review the changes to the FOMC statement line by line, because it has shrunk since Powell has taken the helm as chair.

There was one change, other than the month and policy change. This continued the trend of shrinking the statement. The sentence “The stance of monetary policy remains accommodative, thereby supporting strong labor market conditions and a sustained return to 2 percent inflation” was removed.

In previous articles I stated the Fed would either remove this statement at the September or December meeting. They went with the former.

The main debate over this change is if it was pre-mature because the Fed funds rate is still low. While some can say it is hawkish to say the Fed isn’t accommodative, I think it’s dovish. It signals the Fed is closer to becoming constrictive which is where it will stop rate hikes.

Some at the Fed have even argued to stop rate hikes when they get to the neutral rate instead of making policy constrictive. It’s easy to say this when there isn’t inflation. But if inflation increases, then the Fed will need to hike rates.

There has never been a cycle where the Fed hasn’t gotten too hawkish. While a recession has been avoided for nearly the longest stretch in over 100 years, it’s too idealistic to assume the Fed won’t get too hawkish.

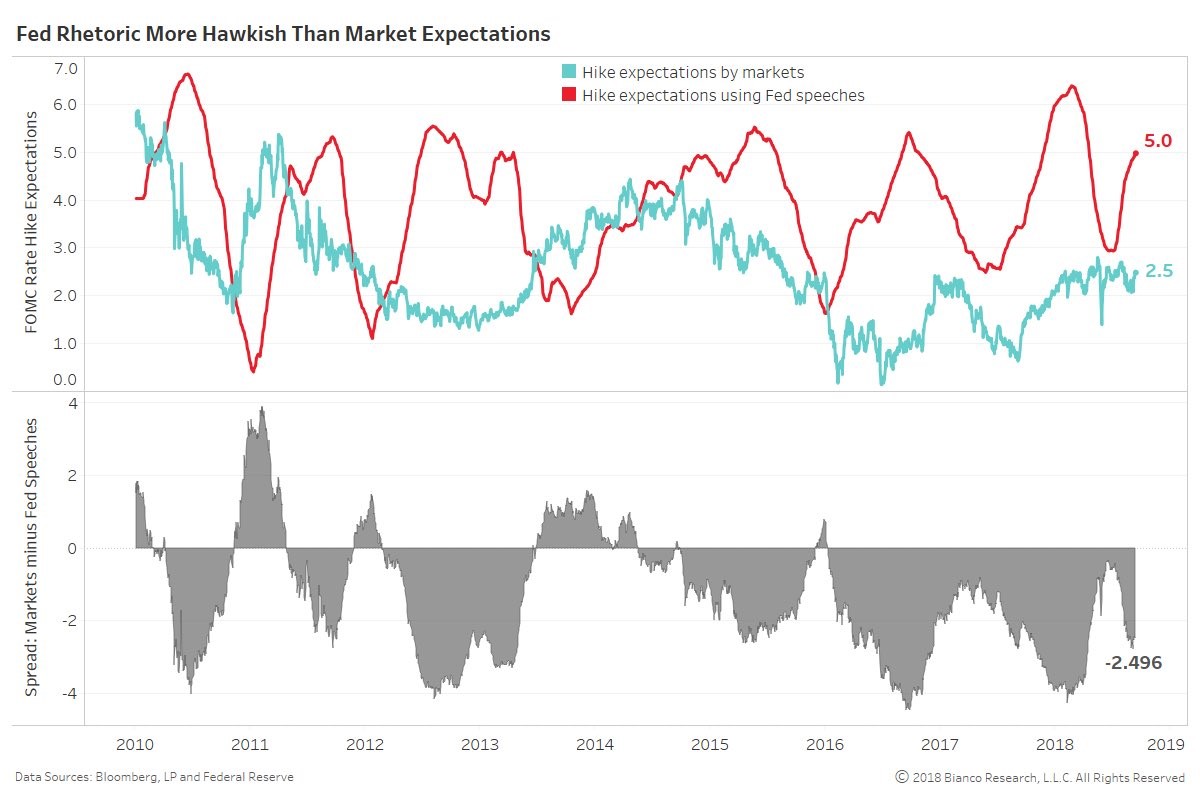

Hawkish Hike - Fed Is Still More Hawkish Than The Futures

In the past few weeks since the Fed’s last meeting, the futures market has increased its expectation for rate hikes and treasury yields have increased.

I have pinpointed the expansion high average hourly earnings growth in August as the catalyst for this increase. We’ve also recently seen a spike in oil prices which will boost headline inflation and has increased nominal yields.

However, even with this increase, the futures market still hasn’t caught up to the Fed’s hawkishness.

As you can see from the chart below, there is a sharp divergence between the Fed’s hawkishness in speeches and the Fed funds futures. The dot plot expects more rate hikes than the futures market.

Hawkish Hike - Fed Hikes Rates, Peak Balance Sheet Reduction

The Fed did what the consensus expected on Wednesday as it raised rates 25 basis points. The pace of the balance sheet unwind will increase for the final time to $50 billion per month in October.

The Fed has been behind its previous targets for the balance sheet reduction, meaning it will really need to increase the reduction to reach that goal.

Even with this increased speed, it will take until 2021 for the balance sheet to fall below $3 trillion. That’s interesting because some economists and policy makers such as Ben Bernanke have suggested that the balance sheet doesn’t need to be shrunk much more.

The goal is for the balance sheet to be between $2.5 trillion and $3 trillion. The debate over the size of a normalized balance sheet will heat up in 2019 as we get closer to the end of the unwind.

If there is a recession in 2020, then the normalization process will end. It’s not clear if the Fed will do another round of QE because many economists have downgraded the effect QE had on the expansion. If it doesn’t boost growth, then why do it?

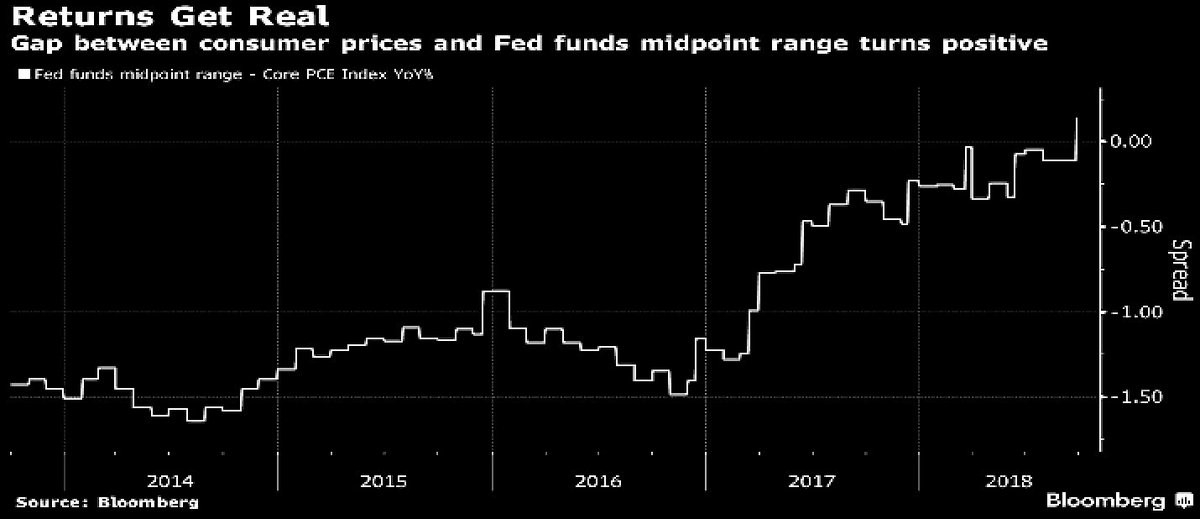

Hawkish Hike - Positive Real Rates

To be clear, while I think getting rid of the term ‘accommodative’ is dovish, the overall meeting was hawkish because of the more optimistic projections.

One of the main headlines out of this meeting is that when deflating real rates by core PCE inflation, they are positive for the first time this cycle. As you can see from the chart below, the real rate has increased since the rate hikes in 2017.

They increased more in 2017 than 2018 because year over year inflation growth fell in 2017 and increased in 2018.

It’s fair to point out that real rates really aren’t positive if you look at core CPI, headline PCE, and headline CPI. The Fed certainly focuses more on core PCE than the other metrics.

It’s possible the Fed got rid of the accommodative stance because rates breached core PCE. Previous recessions haven’t occurred until real rates hit 2%. However, it’s unlikely real rates will get to that point in this cycle. That is, unless inflation falls instead of increases like usually occurs at the end of expansions.

The final point on this is we technically don’t know if real rates are positive. The latest PCE inflation report is from July and we’re in the end of September.

The expectation is for core PCE to be up 2% in August, but as I showed in a previous article, medical prices can cause it to beat expectations.

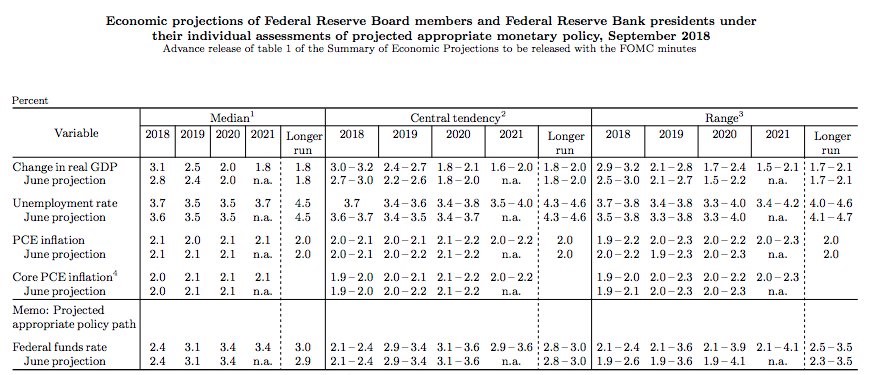

Hawkish Hike - Updated Fed Projections

As I mentioned, the Fed’s future economic projections have gotten more optimistic. As you can see in the table below, the 2018 GDP growth estimate was raised from 2.8% in June to 3.1%.

The 2019 estimate for GDP growth was increased from 2.4% to 2.5%. I agree with the Fed’s expectation for growth to slow next year. The 2018 estimate for the unemployment rate increased from 3.6% to 3.7%. More workers are entering the labor force which is preventing the rate from falling further.

The estimates for 2018 core PCE and headline PCE inflation were stable at 2% and 2.1%. To be clear, headline PCE is expected to be up 2.3% in August and was up 2.3% in July.

The guidance for rate hikes wasn’t changed other than the longer run rate expectation which increased from 2.9% to 3%. With rates currently in between 1.75% and 2%, you can see how real rates won’t get to positive 2% if inflation increases in 2020.

Hawkish Hike - Conclusion

This was an overview of the Fed’s hawkish September rate hike. In subsequent articles, I will review Powell’s press conference and the markets’ reaction to this meeting.

Nothing changed in my opinion, but the markets had a modest reaction as I will get into.