$1 Trillion Doesn’t Matter

Alphabet reported great earnings on Monday afternoon as the stock increased 3.53% on Tuesday. Heading into the earnings report, the stock was up 13.19% year to date. The S&P 500 technology sector was up 12.64%, meaning it didn’t provide investors much outperformance. That’s especially not great for a member of the famous FAANG names. Alphabet has been my favorite name in the acronym for years.

The most useless detail about this quarter is that the market cap is at $866.9 billion which means it is in the race to be the first company to hit a $1 trillion market cap. The media loves to discuss this because it is a fluff story which gains interest from people who don’t know much about finance. I think Apple will probably be the first to hit $1 trillion as it has a $948.6 billion market cap. Either way, it doesn’t matter much. The only thing that matters is the profitability outlooks of these major firms.

Revenues & EPS Beat Estimates

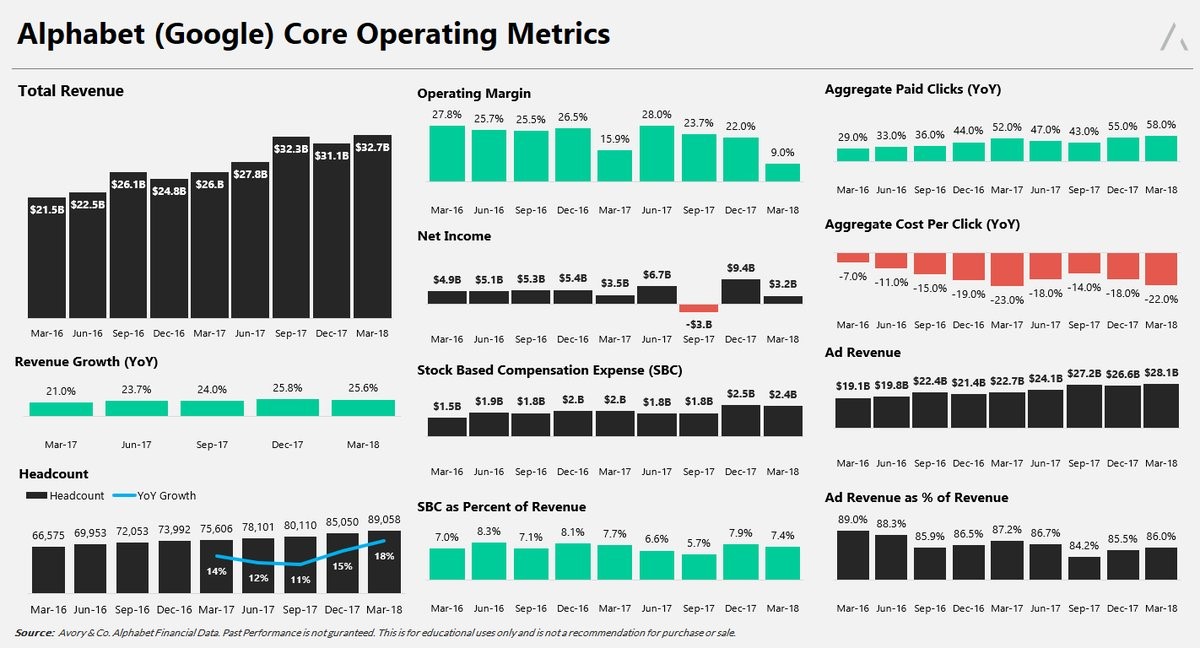

Adjusted EPS was $11.75 which beat estimates for $9.59. Revenues of $32.66 billion beat estimates for $32.17 billion. There was a $5 billion fine for its anti-competitive practices by its Android software in Europe. That means non-adjusted EPS was $4.54. Investors appear to be looking at fines as merely temporary costs of doing business. It’s like an additional tax for being a huge company. To be clear, monopolistic practices aren’t the only concerns from Europe. There are also concerns about privacy which could affect the major internet names in Europe. These risks generate a lot of headlines, but investors aren’t concerned about their effect on long term profits probably because America seems to be lax for now. A one two punch of regulations and fines from Europe and America would be impactful.

As you can see from the chart below, the ad revenue was $28.1 billion which was up 23.9% from last year. This represents 86% of total revenues. For all the discussion about new businesses in the ‘other bets’ category, the bread and butter of the firm is still ads. Keep in mind, this includes YouTube ads as well. The operating margins and net income were hurt by the one time charges I just mentioned.

Other Revenues & Other Bets Drive The Future

The firm’s ‘other revenues” category, which includes the cloud business and hardware products such as the Google Home smart speakers, hit $4.4 billion which was an increase of 36.5% from last year. This is why the overall revenue growth of 25.6% was above the ad revenue. Investors want to know where future growth will come from, but make no mistake about it, Alphabet will be an advertising company for the next few years. To be clear, the “other revenues” category includes stable profitable businesses, while the “other bets” category includes Alphabet’s risky investments into the future. “Other bets” include businesses such as the healthcare company Verily, the internet service provider Fiber, and the self-driving car company Waymo.

A few years ago investors shirked at the idea of investing in money losing businesses, but now growth investing is more popular which has allowed Alphabet to gain credibility in its bets on the future. It’s popular to believe investing in growth is important to avoid dying. Investors will take present losses which will be exchanged for future gains in some of the businesses. Alphabet has become a modern day Berkshire Hathaway. Specifically, the “other bets” category had $145 million in revenue which is up from last year’s $87 million in revenue. However, operating losses also increased from $633 million to $732 million.

Spending to grow has worked for Netflix and now it is working for Alphabet. Disrupting healthcare and driving could be huge businesses if execution is done right. Typically, investors favor startups to disrupt big firms because big firms like to stick to what they know. The entire life-cycle of firms can be disrupted if firms like Alphabet can find the next big businesses which aren’t its main expertise. To be clear, Alphabet investing in self-driving cars is much different than its acquisition of YouTube and DoubleClick.

YouTube Has Been A Huge Success

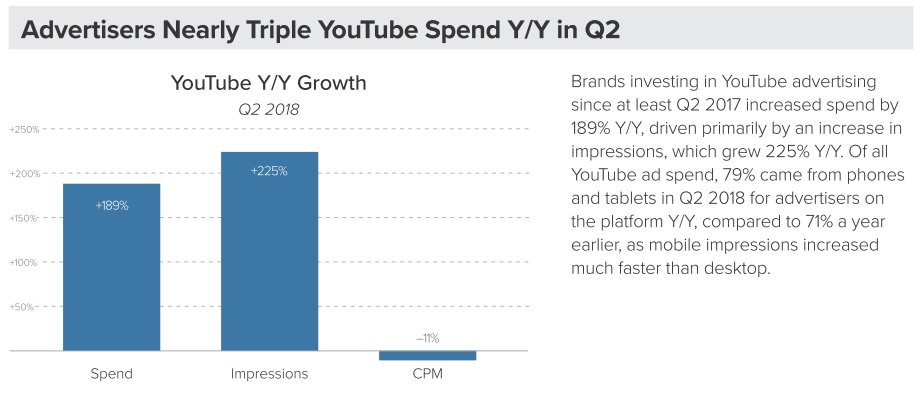

As I mentioned, the purchase of YouTube was a natural progression for the business. It has worked out amazingly as online video has taken over images and text. This is why Instagram launched IGTV. Facebook wants to take some of the online video pie away from YouTube. Despite the backlash YouTube has gotten from advertisers about some inappropriate videos, YouTube is still doing well because it is the only game in town. It has such high market share, there are not many other options. As you can see from the chart below, advertisers have increased their spending on YouTube by 189% in Q2 compared to last year. Impressions are up 225% and CPM, which is the cost advertisers pay to service a video 1,000 times, is down 11%. Not surprisingly, 79% of the ad spend was from phones and tablets which is up from 71% last year.

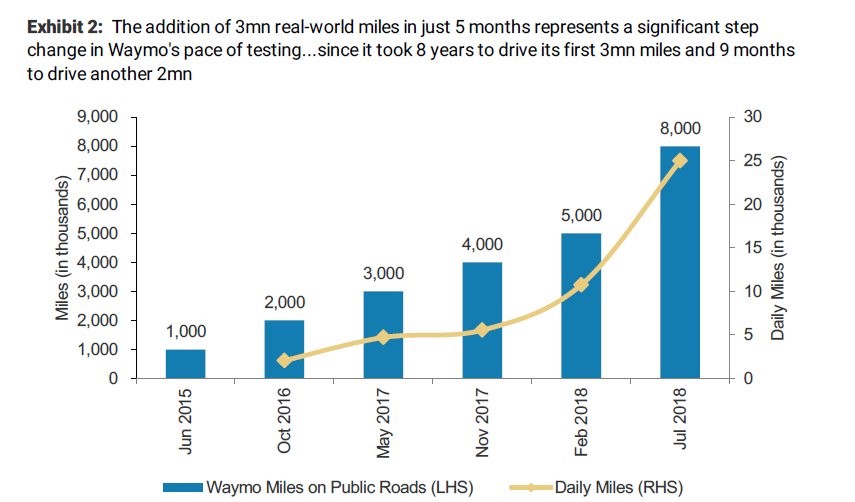

Waymo Increasing Testing

Waymo is all about the future which means the lack of profits in the present is meaningless. Investors are ready to pay up for metrics other than profits and revenues. In this case, the number of miles tested is a key tell as to how the business is progressing. The chart below, shows the number of daily miles and total miles the self-driving car technology has been tested. Waymo is trying to beat out Uber, Apple, and Tesla. It’s tough to say if this is a zero sum game or if there will be a few dominant players. I think the ride sharing business will have one winner because people like convenience more than price shopping when deciding to make a trip. There’s no question being first to market will be important for self-driving cars. The issue is being first will bring intense scrutiny as has already been seen by Tesla and Uber.