President Trump Doesn’t Like Powell’s Rate Hikes

President Trump has made his opinions on monetary policy known more than other recent presidents. During the campaign, he criticized low rates for artificially propping up the economy. He selected Powell as Fed chair and appointed other FOMC members, so some are calling this a "Trump Fed". However, since the Fed is independent it won’t always do what is politically expedient for politicians. It was designed this way because monetary policy shouldn’t try to get the best possible short term results while throwing the future under the bus. It would be great if fiscal policy was long term oriented as well, but when parties change, policies change. It’s the con of living in a democracy. The pro is obviously that the people get a say in how they are governed.

The point I’m making here is that even though the President picked Powell, it’s not surprising to see him criticize his actions. Now that Trump is president, he wants low interest rates to stimulate the economy; he’s not happy with the rate hikes as he mentioned in an interview with CNBC on Thursday. Trump also doesn’t want a strong dollar as it hinders American exports. Trump’s opinions on monetary policy won’t affect Powell’s decisions. However, it’s not impossible to imagine Trump getting Powell to resign so he can make a new pick. I’m not saying that’s likely, but since the Fed will be raising rates more this cycle, Trump will only get more irked in the coming months. The Fed’s rate hike decisions are influenced by the market, so it’s not as if Powell is going rogue by hiking rates. A problem could arise in the next 12 months if Powell hikes rates so much that policy becomes contractionary.

Latest Fed Policy Changes

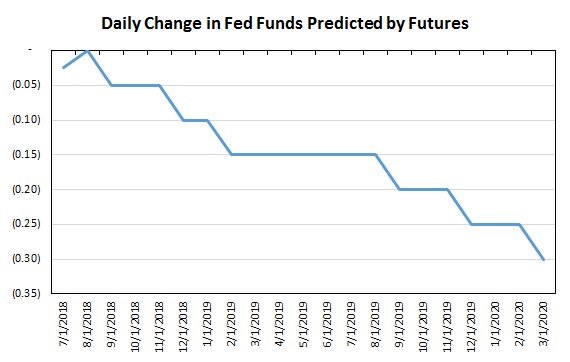

The chart below is interesting because it’s different from the usual ones which show the percent chances of rate hikes in various time periods. The chart shows the change in predicted policy in the past day for every month until March 2020. I don’t focus on 2020 because the CME Group website only shows the odds for policy up until January 2019. As you can see, the daily change was about 10 basis points lower for policy up until the end of the year. The current odds show a 60.1% chance of at least 2 more hikes in 2018. The chart below translates the odds into basis points. There was a pretty big shift in policy expectations for March 2020 as the chart shows a 30 basis point decline. I’m way out in left field on future policy in 2019 and 2020 as I think a slowing economy will halt potential rate hikes. If the Fed hikes 2 more times in 2018, I expect only one hike in 2019 and then cuts staring in 2020.

The Strong Dollar Is A Nuisance

In President Trump’s interview with CNBC, he also expressed his dismay about the strong dollar. A few months ago, the White House was pressed to change its view on the dollar because it looked bad politically to be favoring a weak dollar. Politically, it looks like politicians who support a weak dollar are in favor of the demise of the country. Voters don’t like when they travel abroad, and the dollar is worth less in a currency translation. I’m not saying the White House’s language is the only aspect that affects the dollar. The point here is that ever since that change, the dollar has been rallying. At 8:31 A.M. on Thursday, the dollar hit $95.65 which is its highest point since early July 2017.

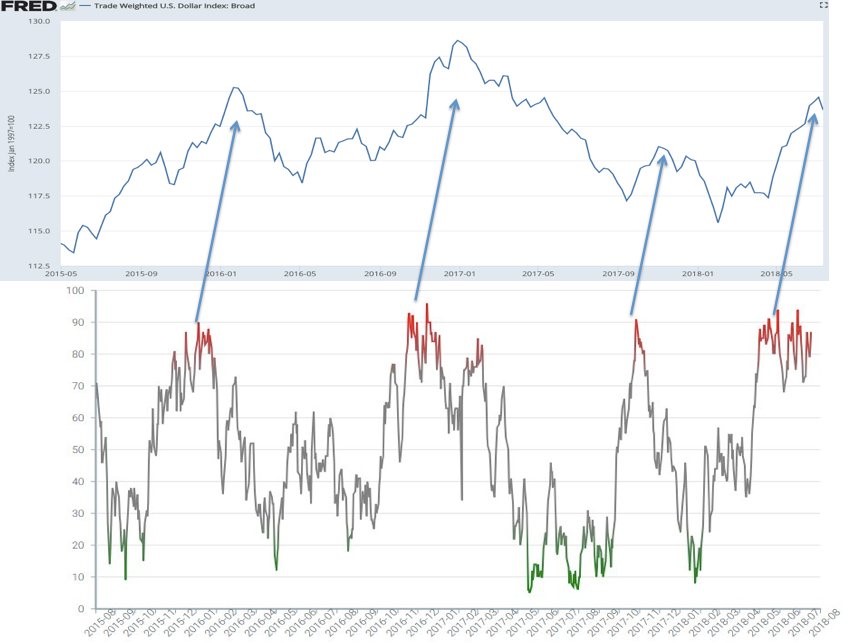

The dollar has been helped by the American economy outperforming other advanced economies and by the fact that the Fed is further along its hike cycles than other central banks. The chart below shows the broad trade weighted dollar index. As you can see, it has rallied just like the dollar index. The bottom chart shows the dollar sentiment index. As you can see, the sentiment is nearly as bullish as it can get, potentially signaling this rally is exhausted. Either the U.S. economy declining in the second half of 2018 or other central banks becoming more hawkish in the next few quarters can catalyze the end of this dollar rally.

Junk Is Doing Well

The latest rally in the stock market along with the confidence in the economy has led the junk bond market to improve. I think the premium yield junk bonds offer over investment grade bonds is too low, but the bears have been saying that for a few years now. The spread is tight, but if the economy remains strong, there’s no reason default rates can’t remain low. The treasury yields have increased since the Barclays high yield rate was at this level 5 months ago, but that’s because inflation estimates, and growth expectations have improved. Increasing rates don’t mean junk bond yields need to spike. The junk bonds in the energy sector like when oil pushes up inflation.

When deciding whether to buy or sell junk bonds or invest in leveraged loans, it’s not enough to say where you think the default rate will go. You need to match up your prediction with the default rate that’s priced in. As you can see from the chart below, the leveraged loan default rate has been increasing slightly in the past few years. It is expected to increase a bit more in the next 12 months. That’s nothing compared to the level seen at the peak after the financial crisis. If you think another recession is coming, you’ll want to bet against junk bonds. If you expect the economy to weaken modestly in the next 12 months, you may not want to put a trade on. As I mentioned, the bears have been expecting a big jump up in default rates for a couple years, but nothing of the sort has occurred.