Weak Durable Goods Report Hurt By Auto Supplier Fire

After the weak manufacturing component of industrial production, we are now seeing weakness in industrial production because of an auto supplier fire. On May 2nd, there was an explosion at an auto supplier called Meridian Magnesium Products of America in Eaton Rapids. This plant has annual production of 14,484 tons and is 208,000 square feet which is the size of 2 Target retail stores. Two people were injured and 150 were evacuated.

The good news is April’s reading was revised higher, which will help GDP growth estimates. The bad news is the May report missed the consensus which will bring GDP estimates down. April’s month over month new orders fell 1% instead of falling 1.7%. Excluding transportation orders were up 1.9% instead of 0.9%. Finally, core capital goods orders were up 2.3% month over month instead of up 1%.

The May report had across the board weakness as the new orders were down 0.6% month over month which met estimates. Excluding transportation orders were down 0.3% month instead of up 0.5%. Core capital goods orders were down 0.2% instead of up 0.2%. Because of the fire, vehicle orders were down 4% and vehicles shipments were down 4.4%. Last month’s report was hurt by the volatile aircraft orders which declined 30.3%. The May report was also hurt by aircraft orders which fell 7%. Even after you exclude these temporary issues with transportation goods, the orders were still down 0.3% which means this wasn’t a great report.

The primary metals and fabrications were down after there was a burst in buying because of the tariff announcements. You can say this is a temporary decline caused by tough month over month comparisons which won’t be faced again. Specifically, primary metals orders fell 0.4% after they increased 2.4% in April and 4.7% in March. Fabrications orders were down 1.2% after they were up 3.3% in April and 1.3% in March. These two components are over 20 % of total durable goods orders. This means the headline decline likely won’t continue in June.

Unfilled orders were up 0.5% which is following a 0.6% build in April and a 0.8% increase in March. This is the best performance in 4 years. Finally, durable goods inventories were up 0.3% for the 2nd month in a row.

Atlanta Fed Nowcast Updated

The Atlanta Fed Nowcast hadn’t been updated in 8 days, so this update, which saw the GDP growth estimate fall from 4.7% to 4.5%, includes many changes. We’re near the end of the quarter, but most of the data from June still hasn’t been reported yet. This means we’re far from certain where GDP growth will be despite Secretary Mnuchin’s claims we are headed for a big report. GDP growth will probably be above 3%, but that’s not a lock.

There were a few changes to the Nowcast. Specifically, the estimate for real residential investment growth fell from 2.9% to 0.6% because of the existing home sales report last Wednesday and the new home sales and costs report this Monday. The durable goods, inventories, and international trade in goods reports, which were released Wednesday, caused the estimate for inventory investment growth to fall from 0.87% to 0.46% and the estimate for net exports to rise from 0.46% to 0.66%.

Even though Q2 is over this week, these estimates will continue until the advanced GDP report next month. The final estimate for Q1 GDP growth will come out on Thursday. The expectation is for GDP growth to remain at 2.2%. The CNBC GDP rapid update which looks at the best Q2 GDP growth models, shows the average out of 11 estimates is for 3.9% growth and the median estimate is for 3.7% growth.

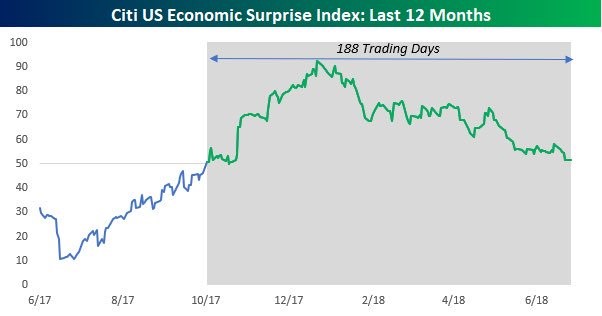

Citi Surprise Index Declining

You may have noticed that many economic reports are missing estimates. It’s not that more economic reports are missing than beat estimates; it’s that there are more misses than a few months ago. As you can see from the Citi Surprise index in the chart below, the beat rate has fallen since the beginning of the year. The index peaked at about 90 and now it is at about 50. It’s notable that Q1 GDP growth was 2.2% and Q2 GDP growth will likely be above 3%. This reinforces the point that beat rates aren’t 100% correlated with growth rates. If expectations are very high and reports miss them, but are still good, you can get strong growth and a low beat rate. The Citi Surprise index can be used as a second derivative expression of the direction of the economy. It certainly reflects the recent stock market performance which peaked around when this index peaked and has mostly followed it lower.

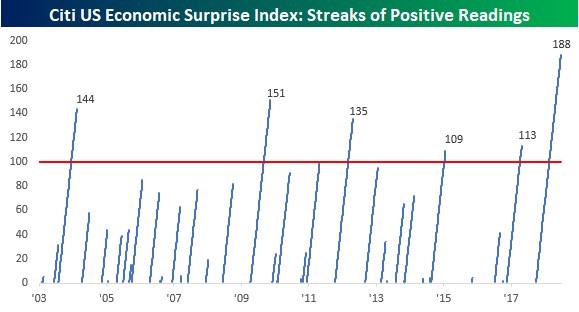

The chart below shows that the current positive streak is 188 days which is the longest since at least 2003. If the index ends this streak, it means the near term performance of the stock market could be weak. The end of similar streaks led to slightly negative performances in the next 1 month and 3 months. Performance improves in the next 6 months because these streaks are all about managing the expectations game and only partially about the rate of change of economic growth. That being said, the end of the streak in Q3 will probably coincide with a deceleration in GDP growth based on the NY Fed’s Q3 Nowcast and the ECRI leading indicators report.

Keep in mind, the monthly leading indicators don’t show any negative results are coming. However, that can easily change. Q3 won’t be a recession, but it might include slower growth. The recent decline in the stock market is a negative factor which will probably prevent the June leading indicators report from reaching a new high in June. Remember, new high readings give bulls a high level of confidence that there won’t be a correction in the near term. As you can see we are entering a situation were a correction is actually more likely than average rather than less likely.