Moderate Rally As Trade Worries Linger

The S&P 500 was up 0.22% as the stock market continued its upward momentum from late in the trading session on Monday when Peter Navarro calmed the markets. The Nasdaq and Russell 2000 regained even more of their losses as they were up 0.39% and 0.66% respectively. Press secretary Sarah Huckabee Sanders seemed to support more of what Mnuchin said than what Navarro said when she stated, “As the Secretary said, a statement would go out that targets all countries that are trying to steal our technology, and we expect that to be out soon.” The market is simply waiting to see what the statement says on Friday.

To be clear, Peter Navarro is a proponent of tariffs, so his statement has credibility as well. The good news is that this situation is all a negotiating tactic. The bad news is firms may temporarily pull back on capex until clarity returns. The stock market can rebound easily once a deal is made, but capex will take weeks or months to come back after this potential weakness. I’m not even sure how much capex will be impacted by these tariffs. That’s a second derivative level of uncertainty.

I’m guessing the Trump statement on intellectual property will come out on Friday because that’s what the Wall Street Journal report from Sunday stated. I’m happy the market fell in anticipation of the statement because it shouldn’t be shocked when it comes out. If the statement is what the market expects, there should be a relief rally. There are algorithms which trade based on Trump’s tweets and each news event in this tariff skirmish. However, you can look towards the intermediate term to game this system if you agree with Buffett and Paul Tudor Jones that this will be solved amicably because trade is mutually beneficial.

Treasuries, Dollar, And Oil

The 10 year yield fell slightly and the 2 year yield was flat. This means the curve flattened slightly. As of Tuesday night, the 10 year yield was 2.8784% and the 2 year yield was 2.5404%. This makes the difference between the 2 yields just 34 basis points, which is the flattest of this expansion. The bulls hope that the curve will steepen again if the trade skirmishes are worked out. I think the Fed can easily rescind one of its rate hikes this year after seeing the continued pressure the economy is under because of the tough trade talk.

The biggest call on treasuries I’ve seen in a while was made by Morgan Stanley on Monday. The firm stated the trade skirmishes, the weakness in emerging markets, and the strong dollar will prevent the 3.12% top in the 10 year yield from being breached. On the other hand, Jamie Dimon said in shareholder letter in April that he thinks the 10 year yield will breach 4%. I’m on the side of Morgan Stanley until the trade tensions are eased. After that, I can see yield breaking the 3.12% level, but not hitting 4%.

It’s funny to think about how the financial media was obsessed with the 3% level because it was supposedly going to cause investors to flee stocks a few months ago. The stock market hasn’t done well since the 10 year hit 3%, but that has nothing to do with the weakness. Plus, the 3% level was breached for a short time as it has been below that level for over a month.

The dollar index was flat on Tuesday. You can see in the chart below that the 200 day moving average has started to move up in the wake of this recent bull run. The strong dollar hurts S&P 500 earnings, hurts American exports, and suppresses the 10 year yield which flattens the curve. The bull run has already been bothersome; each handle it rises will cause more pain.

After a brief respite in the $60s caused by the OPEC cuts, WTI is now above $70. The futures were up 26 cents to $70.79 on Tuesday. The biggest catalysts pushing it higher are the Trump administration’s call for allies to cut imports of Iranian oil to zero and the power struggle between the Libyan government and the rebels. Finally, the market is also concerned about the 350,000 barrels per day of production in Syncrude Canada which are uncertain because a transformer blew and shut down an important oil sands upgrader on June 2nd. The repairs will last a few more weeks.

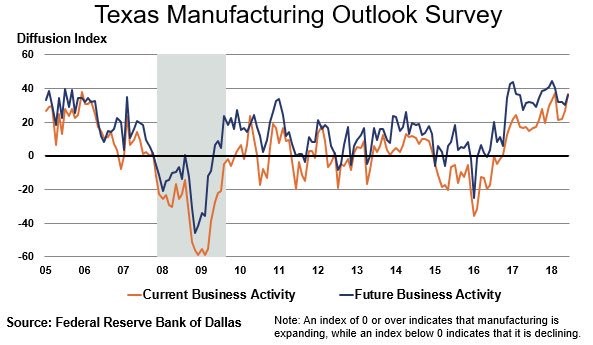

Strong Dallas & Richmond Fed Reports

After a couple of weak regional manufacturing reports, which were the Philly Fed and the Empire State index, there appeared to be signs the manufacturing economy was weakening. The Dallas Fed and the Richmond Fed reports don’t support that narrative. As you can see from the chart below, the Dallas Fed’s general activity index was 36.5 which beat the high end of the consensus range which was 33.6 and the prior report which was 26.8. However, on the negative side the production index fell from 35.2 to 23.3. The new orders index was up 1.9 points to 29.6 which was the highest result this year. Furthermore, the 6 month outlook was up 5.2 points to 33.2. This was the highest the index has gotten in 12 years. It appears the rising oil prices are helping this district.

You can’t say the Dallas Fed report was a one off positive sign because of high oil prices since the Richmond Fed index also showed great results. The headline index went from 16 to 20 which was above the high end of the consensus range which was 16. Shipments were up 2 points to 17 and the volume of new orders index was up 6 points to 22. Capex was up 7 points to 26 despite the worries about tariffs. The 6 month expectations also looked great as the index which measures the expectations for local business conditions was up 15 points to 40. The future estimate of backlogs went up from 15 to 28. As you can see, both regional Fed reports show manufacturing is strong.