Inflation Data Shows Modest Price Increases

After a few months of acceleration in inflation, the CPI and PCE reports have become the most important economic reports to the market. Investors and economists expect a big pick up in inflation this year. I have switched from being bullish on inflation to being bearish on inflation based on the more optimistic consensus. The Fed is raising rates in a situation where wage growth is still modest because of the continued slack in the labor market. Therefore, it doesn’t make sense to forecast such high inflation this year. I expect more of the same results that we’ve from inflation seen this cycle. The average inflation for 2018 will be higher than 2017, but that’s not saying much.

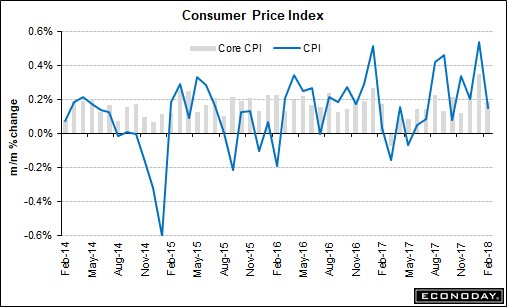

As you can see from the chart below, the month over month change in the CPI was 0.2%. That met consensus and was down from the month over month growth of 0.5% in January. Clearly, January’s growth rate wasn’t sustainable. The year over year CPI was up 2.2% which met consensus and was up 0.1% from last month’s report. The month over month core inflation was up 0.2% which met expectations and was 0.1% lower than the previous report. The core CPI was up 1.8% year over year which missed the consensus by 0.1% and was the same as the last report. As you can tell, this was a middling inflation report which is far from the fears some investors had after the January report. This inflation report was consistent with the wage growth seen in the labor report last week.

Under The Hood Of The CPI Report

Let’s look at the individual components to see the reason behind this relatively mild inflation report. Transportation inflation was flat which was down from the strong gain last month. Energy prices were only up 0.1%. Gas prices were down 0.9% after the seasonal adjustment. Food prices were flat as the price of food at home was down 0.2% and the price of food away from home was up 0.2%. This explains why the month over month change in the core CPI and the headline CPI were the same. Even though the Fed focuses on the core inflation, that doesn’t mean food and energy don’t matter. They are extremely influential on costs. Also, keep in mind, that the Fed has a 2% target for core PCE inflation which is usually lower than core CPI. Therefore, the 1.8% core CPI isn’t that close to the Fed’s target.

Interestingly, apparel was up 1.5% in February after a 1.7% increase last month. That’s the largest 2 month increase since 1990. Apparel has been one of the least inflationary parts of the CPI in the past 10 years, so I don’t expect this trend to continue. There was a 0.5% drop in the cost of new cars and trucks which was the biggest decline since 2009. This might be the result of weak sales. The problems with auto sales might provide deflationary pressure for the remainder of year. Auto insurance increased 1.7% in February and 1.3% in January. Medical costs and used vehicle costs fell month over month. Telecommunications costs fell sharply. Yellen blamed wireless costs for the weak inflation in 2017. If prices fall in 2018, she was wrong about the issue being transitory.

Market Reaction To Inflation Data

If you look at the 10 year bond, the yield started falling before the CPI report came out. It then increased and fell again to close down 2.55 basis points. It’s now at 2.84% which means it has been below the high set on February 21st for 3 weeks. I’m starting to get more cautious on expecting yields to increase because I think Q2 GDP growth will disappoint based on the ECRI data and I expect inflation to come in below the consensus estimate. The technicals are important because there’s huge resistance at the 3% level. I don’t think stocks will fall if it hits 3%, but my expectation for it to hit 3% has diminished after seeing the CPI data. If the 10 year yield doesn’t rise, that’s terrible news for the yield curve because Fed rate hikes have pushed up the short end of the curve.

As of Tuesday night, the difference between the 10 year and 2 year yield was 59 basis points, meaning it has flattened recently. Based on the economic data and the market trends, I expect the odds for rate hikes to fall as I think 2 rate hikes in 2018 are on the table. The odds for rate hikes moved slightly to the dovish side after this report. I am interest to see the Fed’s language in its statement next week as it is coming on the heels of a tepid CPI report. This will be Powell’ first meeting and the first rate hike since December.

Will The Trend Change In Inflation Last?

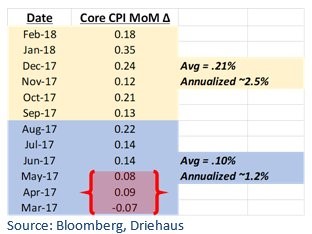

The table below shows the past 12 months of the month over month change in core CPI. As you can see, the average has doubled. February was below the average by 3 basis points. The key is figuring out what the next 6 months of data will be. It’s not a great idea to annualize the month over month data and then assume that will be the year over year data for the rest of the year. There still needs to be steady improvements to get from 1.8% year over year core CPI growth to the estimates for 2.5%. I think there’s a much better chance of core CPI being between 2% and 2.5% than between 2.5% and 3%.

Conclusion

I have been leaning towards thinking the January reports were too hot in the sense that wage growth was too high and inflation was too high. I don’t think those levels are fair estimates for the rest of the year. The market got ahead of itself after the January reports. I think the March data will be rendered useless because of the 3 nor’easters. These storms were powerful and effected not just the northeast.