Beat Expectations, Stock Falls Anyway

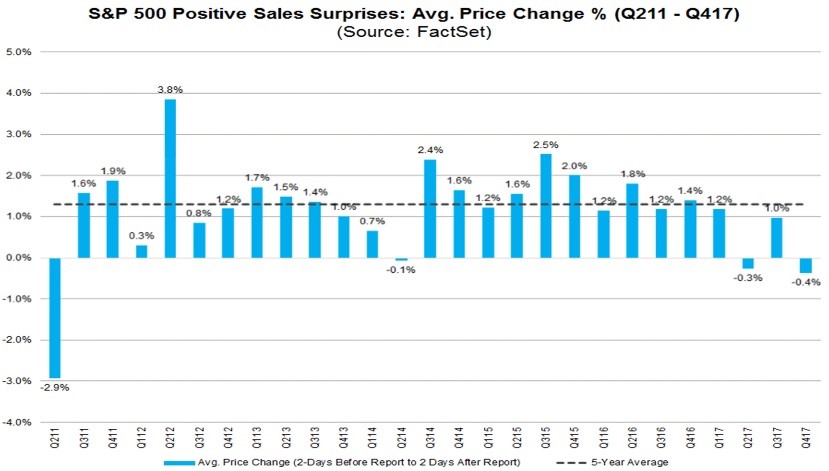

In the Q2 2017 earnings season, the market was acting weirdly. Stocks were falling when firms were beating sales expectation. My guess was that stocks priced in great results, so investors weren’t enamored after results were beat. In the Q1 2018 earnings season we’re seeing the same phenomena occur. As you can see from the chart below, the 4 day movement (2 days before report and 2 days after report) on stocks which beat revenue estimates was -0.4% this quarter. The 5 year average gain is 1.3%. The firms which missed estimates saw their stocks decline 1.2% which was 0.1% worse than average. Essentially, it was an average quarter for firms that missed, but way below average for firms that beat. My guess on why this occurred is that this quarter was a throw away one as investors were more focused on next year’s results which should be helped by the tax cuts.

Another possibility is that the market simply did bad when firms reported. The market fell because the short volatility trade unwound as traders temporarily ignored the great earnings results. During the correction 41% of companies reported results. Keep in mind, the metrics on firms missing results is much less useful than other quarters because so few missed. 77% beat sales guidance which is the best since FactSet started the calculation in Q3 2008. FactSet also cites the high price to sales ratio, which was 2.2 during the quarter and 2.1 now, as a reason stocks did poorly after beats. My contention with that metric is firms have very high margins which justifies the high sales multiple. Some investors, particularly those who follow the Shiller PE, believe margins always mean revert, but clearly stocks will only fall until there’s evidence of declining margins.

Earnings Will Drive Stocks Up

It’s critical to recognize that earnings don’t cease to be important out of the earnings season. If an investor is looking to start a position in an individual name, the first aspect he/she will review is the recent earnings results. Sometimes short term noise gets in the way of the fundamentals, but in the long run, earnings are what matters. It’s very easy to get caught up with the news of the day. It can be important to your life, but ultimately you need to ask the tough question of whether it will impact earnings results.

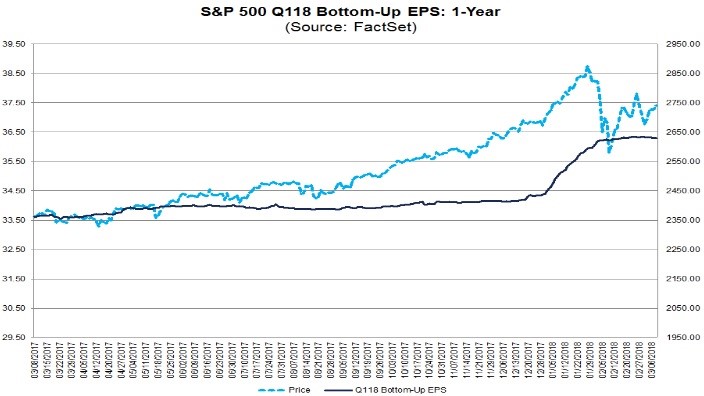

My thesis for this year continues to be stocks will rally, but less than the earnings growth in 2018, meaning there will be earnings compression. Secondly, I expect earnings results to be lower than the current estimate of 18% growth. Since last week, the FactSet calculation for 2018 earnings estimates has gone up 7 cents to $158.07. As you can see from the chart below, the Q1 bottom up EPS estimates have fallen slightly. Some bears act as if knowing that estimates will fall is some sort of tradable knowledge. It’s not an edge, just like how knowing earnings usually beat results is not an edge. Stocks can rise with declining expectations because the estimates started high and then were raised in January and February due to the tax cut.

Merger Mania & Geopolitical Issues

In the next 1-2 months, I think the biggest catalysts which can move stocks are news out of the White House, the inflation data, and the Fed meeting in March. Most recently, President Trump struck down Broadcom’s purchase of Qualcomm due to national security concerns. That makes investors second guess the M&A landscape. This is important because M&A is expected to heat up this year. Ultimately, I think this isn’t a major long term issue because Trump blocked a deal where an international firm was buying an American firm. I think this is a one off issue that was made for defense reasons. The chart below shows the M&A activity where American firms are buying domestic and cross border targets. On another note, the fact that the total American M&A activity in the first 2 months and 6 days is the most since 2000 probably isn’t a great sign for the economic cycle. Previously, M&A activity has peaked right before recessions. The activity was high in 2000 and 2006. Keep in mind, the stock market peaked in March 2000, so up to that point in the year, everything was going great.

The other market moving news that will come out of the White House is President Trump’s meeting with Kim, the North Korean leader. The meeting is expected to occur by May. In 2017, the stock market reacted briefly to the North Korean missile launches. I don’t think there’s any way to predict what will come of this, but it should affect the market when it happens.

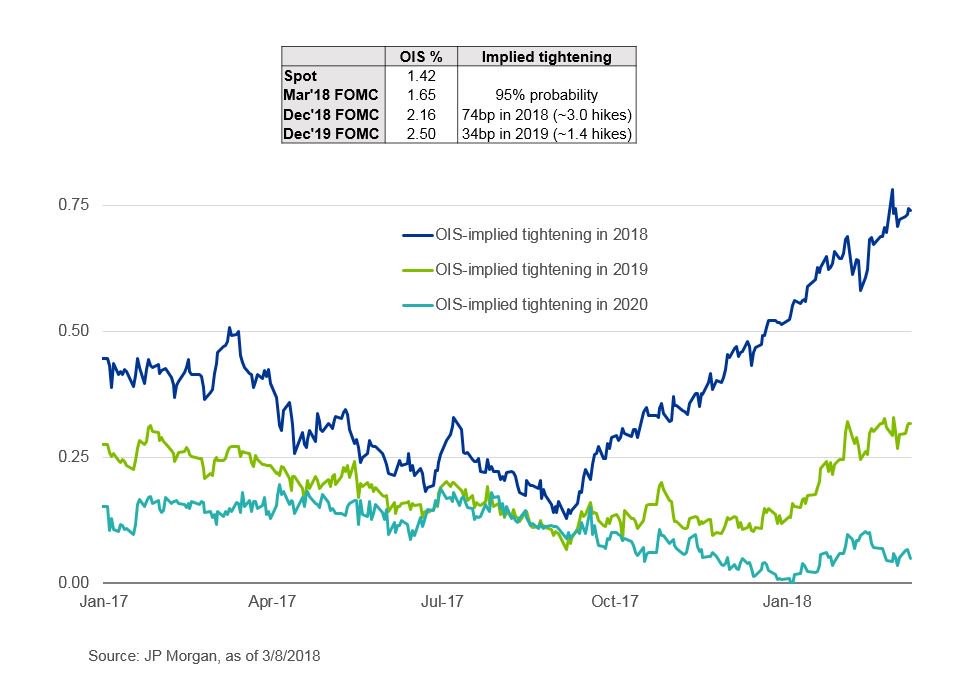

Fed Policy Expected To Be Stable In 2019

I’ve mentioned in previous articles that the Fed will be hawkish at the end of this year or the after the first hike in 2019. It’s important to point out that the Fed is expected to slow down its rate hikes next year. The Fed might be mostly done with its hikes in 2018 if inflation stays near where it is now with a slight increase in the next few months. As you can see from the chart below, the Fed is expected to hike 3 times in 2018 and 1.4 times in 2019. It will be interesting to see if the Fed inverts the yield curve with these hikes. I think 4 hikes would do it which is why the market gets squeamish when the odds of 4 hikes increases. It’s worth noting that the combined unwind of the Fed’s balance sheet in 2019 will be much higher than in 2018 as it will be operating at the $50 billion per month peak rate. Some are blaming the volatility in February on the Fed’s unwind and the ECB’s tapering. If the only result of the QE unwind is a normal correction in stocks, the Fed will be very happy. In fact, the Fed is probably happy the euphoria was released from the stock market.