Gary Cohn Resigns

The President’s chief economic adviser, Gary Cohn, plans to resign. This likely means the tariffs will go through in some manner because he was staunchly against them. Cohn brought stability to the economic team and was a big proponent of the tax cuts. Obviously, the tax cuts have already been passed, but this is still bad news because the market doesn’t want tariff supporters to dominate the White House. The market declined in the morning based on rumors of him stepping down. There might be more selling on Wednesday now that the news has been confirmed (pre-market futures declined after the announcement). Either way, this is bad news for the market in the intermediate term because Cohn was a pro-growth economist. His worldview is favorable to the stock market.

Retail Investors Sold In February

Obviously, stocks declined sharply in February. However, it’s useful to get the specifics. The more selling, the better because the euphoria needed to be washed out of the market. Trimtabs stated there were $41.1 billion in outflows in February which is the 3rd most in the firm’s records. ETFs lost $19.6 billion, which is 0.9% of funds, and mutual funds lost $21.5 billion, which is 0.3%. Global funds gained $17.9 billion. I actually agree with this movement because foreign stocks and emerging markets offer more value than America. The outflows mostly occurred in the first week of the month as there were $37 billion in outflows which is a record.

There are many retail investors who have all their money in America. They say they like America’s economic freedom compared to China. It’s amazing how quickly you’ll see that sentiment reverse when America underperforms. While these retail investors pretend to be passive, they will quickly switch to the next hottest market. While America is obviously a sustainable place to put your money, chasing performance makes you no different from speculators in cryptocurrencies. Investing when retail investors have gone ‘all in’ is usually a bad idea.

The other point worth noting is that passive investors shouldn’t be reacting to the market movements. If you have the right portfolio allocation, you won’t get scared out of your positions when there’s volatility. I’m bullish on American stocks this year, but I advocate a high allocation to emerging markets. The chart below shows the retail investor activity compared to the S&P 500. Retail investors get scared and sell out of stocks during corrections. They were bearish at the bottoms in 2011 and 2016. I wouldn’t be surprised to see some more volatility in the next few weeks to shake them all out. Even though the investor movement index has fallen sharply, it’s still relatively high.

Stocks Rally Slightly On Tuesday

It looks like Tuesday was the calm before the storm. Weather-wise the nor’easter last week and the one on Wednesday, should have a big impact on the economic data for March especially since March usually doesn’t have severe winter storms. Politics-wise the fallout from the Cohn resignation will be interesting to watch. The hope for the stock market is he’s replaced with a pro-growth economic adviser.

The S&P 500 was up 0.26% on Tuesday. The Russell 2000 outperformed as it was up 1.04%. Utilities had a sharp 1.36% decline as they corrected from the previous rally. The 10 year bond was flat, but it looks like it will decline on Wednesday if the fallout from Cohn’s resignation sticks. To be clear, I’m not expecting a 10% correction from this Cohn resignation, but it adds fuel to the worries about tariffs which could cause a correction at some point. I’m still not sure what the actual policy will be. The dollar was down 0.6% as it continued its inverse relationship with stocks.

Solid Non-Manufacturing ISM Report

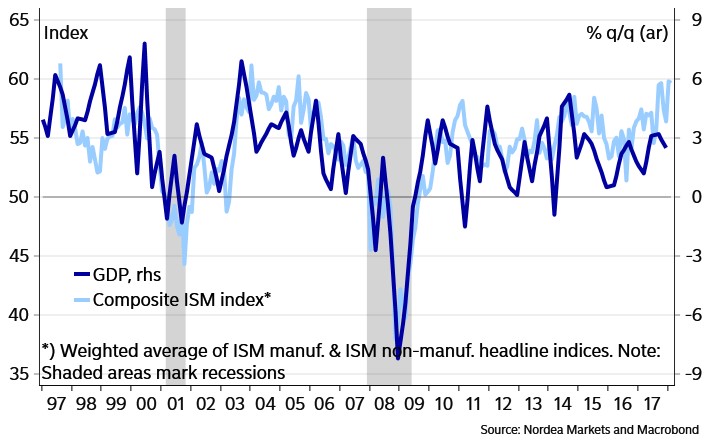

As I expected, the ISM non-manufacturing index beat expectations by 0.7%, coming in at 59.5. As you can see from the chart below, the ISM reports have been consistently above the actual GDP growth in the past 3 years. At this point, I just accept the fact that the ISM report will be overzealous. That being said, I wouldn’t go as far as ignoring it.

The report was 0.4% lower than the 12 month high in January. It was 2.1 points higher than the 12 month average. This report is consistent with a 3.9% GDP growth rate which is probably too optimistic. The prices index declined slightly to 61 from 61.9. As of Monday, the 10 year breakeven inflation rate was 2.13% which is one tick below the 2018 high. The Fed will take this into account when it meets in 2 weeks. The export index went up 1.5 points to 59.5 and the imports index fell 4 points to 50. That’s a good signal for the GDP report. A professional, scientific, and technical services firm stated, "Optimistic outlook due to GDP and tax breaks, tempered by stock market instability." There were two mentions of the stock market in the quotes. I doubt the volatility affected most businesses besides those in financial services. The volatility probably helped Goldman Sachs.

The table below shows that the peak in the manufacturing ISM is meaningless when it comes to forecasting a recession. This data is making the obvious conclusion that the manufacturing ISM is not going to stay at the highest point since May 2004. Manufacturing is an even smaller percentage of GDP than it was in the previous periods listed below. There was manufacturing weakness in 2012 and 2016 without a recession. That being said, a decline in manufacturing in 2019, would be worse than the prior two situations this cycle because the Fed will be much more hawkish. It seems like the market is more focused on negative events in 2018 than 2017. That difference will be magnified next year as the market becomes even more sensitive because the Fed will have rates higher and will be unwinding the balance sheet at a rate of $50 billion per month.