Powell Spoke On Thursday

In the midst of the uncertainty surrounding the potential tariffs on steel and aluminum, Fed chair Powell spoke to the Senate Banking Committee. It clearly wasn’t focused on as much as the Tuesday testimony. However, it was still important in my opinion. As expected, there were some quotes which were dovish. I strongly disagree with the notion that we should just look at one sentence on Tuesday as the market did instead of reviewing the whole testimony on Tuesday and Thursday. I like to take a holistic approach to understanding Powell’s thinking.

The market is driven by algorithms. There are times when I think the market takes things out of context. The 10:30 AM statement where Powell said the FOMC would take another look at the dot plot and the Trump administration’s plan to implement a tariff are two examples of this. Over time the market properly digests information, but new shocks can lead to an overreaction. This is normal behavior. 2017 was abnormal in that nothing phased the market.

Some Dovish Statements

Let’s review some of the quotes from the Thursday testimony. When asked about whether the Fed would avoid hiking rates too much because some workers haven’t gotten a wage increase yet, Powell said, "We don't see any strong evidence yet of a decisive move up in wages. We see wages by a couple of measures trending up a little bit, but most of them continuing to grow at two and a half percent. Nothing is suggesting to me that wage inflation is at a point of accelerating. I would expect that some continued strengthening in the labor market can take place without causing inflation."

This statement is very dovish. Some indicators like the ECI report have been steadily accelerating. The Atlanta Fed wage growth was strong in 2016, but in the past year, it has rescinded. Wage growth is the ultimate indicator which will signal it’s time to raise rates significantly. The fact that Powell doesn’t see wage growth means to me that he won’t raise rates sharply. It’s interesting that some are saying the door is shut on 2 hikes in 2018 and open for 4 hikes. Factually, that’s incorrect because the market is pricing in an equal chance of 2 hikes and 4 hikes.

Next Powell said, “By continuing to gradually raise interest rates over time, we're trying to balance those two things and achieve inflation moving to target but also make sure the economy doesn't overheat. There's no evidence that the economy is currently overheating. But that's really the path that we've been on. My expectation is that that will continue to be the appropriate path as long as the economy continues to perform this way." I think it’s bizarre to conclude Powell is hawkish when he says there’s no evidence of overheating. The Fed is gradually hiking rates in the middle of its hike cycle. The economy is still having a weak expansion unless 2018 sees acceleration. There’s no reason for the Fed to overshoot on rate hikes and cause a recession if inflation is manageable. Investors who are spooked about 4 hikes are getting ahead of themselves.

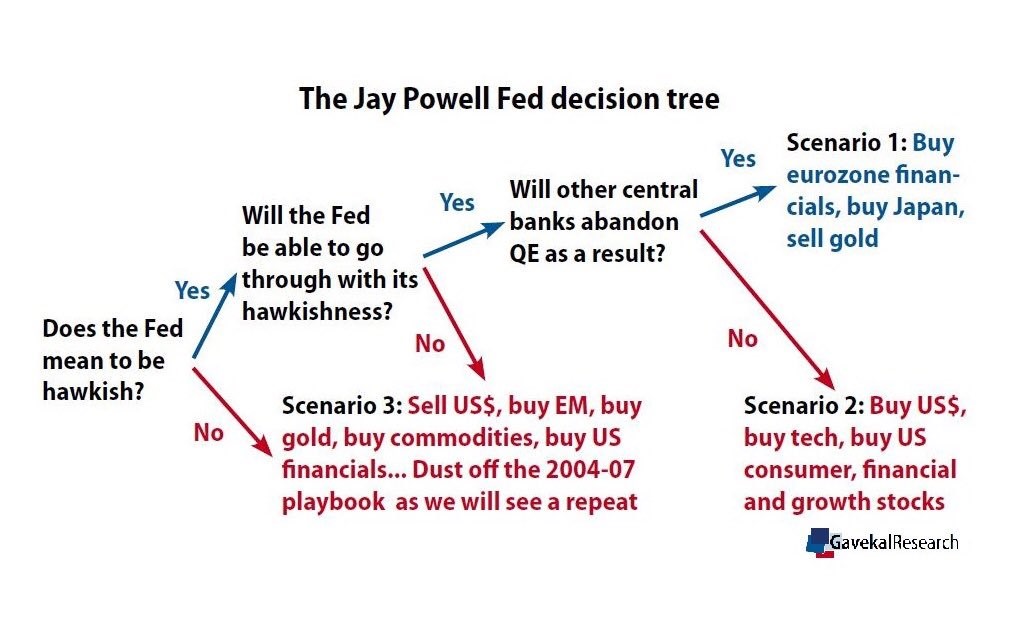

Powell Decision Tree

The image below reviews what investors should do in three monetary policy scenarios. I don’t believe the Fed means to be hawkish. This scenario means investors should sell the dollar, buy emerging markets, buy gold, buy commodities, and buy U.S. financials. It says we’ll see the 2004-2007 market probably because inflation will increase. To be clear, this situation won’t last for 4 years like that period. It’s tough to see where the Fed will put rates in 2019 and beyond. I don’t want to risk sounding like a Pollyanna, but it looks like the Fed did a great job this cycle. It didn’t see fast growth, but it has been a very long cycle and I don’t see massive problems in the system which could create a collapse like in 2008. That will likely be the biggest recession for many decades.

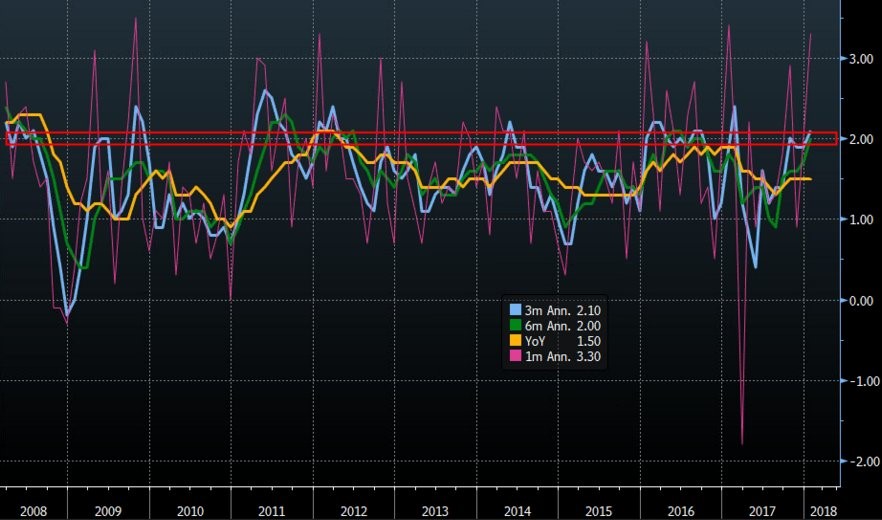

Inflation In Different Time Scales

On Thursday, the year over year PCE growth was released. The January data showed 1.5% year over year core PCE. That met expectations. The month over month core inflation also met expectations at 0.3%. At this point in the cycle and the way the market has been reacting to inflation, meeting expectations is great because it means the economy isn’t overheating. This is partially why treasury yields fell.

The chart below shows the year over year, 1 month annualized, 3 month annualized, and the 6 month annualized core PCE. This may seem like overkill, but it’s useful because the year over year data is in a relatively rare stretch where it’s the lowest out of each period. Because the year over year data is the lowest, this can be considered cherry picking. The fact that the 3 month over 3 month annualized PCE is at 2% further supports the inflation narrative. This is important because I had been citing the PCE report as going against the other regional Fed reports. In summary, this report had something for everyone in that it met targets, but also showed signs of acceleration.

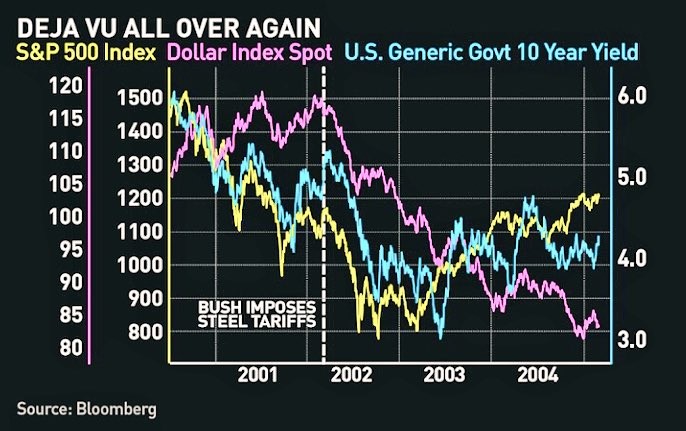

Past Example Of A Tariff

Speaking of cherry picking data, the chart below does just that. While it’s important to review past patterns to see if they will repeat, don’t get too overzealous. The chart shows the changes in the dollar, the 10 year bond, and the S&P 500 after the 2002 steel tariffs were imposed. This is interesting, but you can’t assume the same reaction will occur again because we are in a different economy now. In early 2002, the economy was just exiting a recession and the tech bubble was near the end of its burst. Stocks were already in a downtrend. It’s wrong to blame the steel tariffs for the decline in stocks. Don’t expect a bear market because of these potential tariffs. The best mindset to have to is to review the previous examples of tariffs to see how foreign nations will react.