Stocks Decline On Wednesday

Yesterday, I challenged the market by saying it really wasn’t worried about Powell’s potential hawkishness. I said if stocks were really worried, they would be down more. The market answered the bell on Wednesday by falling at the end of the trading session. The S&P 500 fell 1.11% after being up in the morning. The market ended the 10 month positive streak which was the best since 1959. It was 15 months if you include total returns.

Powell To Speak Again On Thursday

Jerome Powell will be testifying in front of the Senate banking committee on Thursday. I wouldn’t be surprise if the market interprets what he says as dovish and this two-day decline reverses. The statements made are purposely vague. The Fed is far from locking in 4 rate hikes this year. Even if Powell personally thinks the economy and inflation are strengthening, it doesn’t mean the Fed will change its initial stance.

The market has been keying off the data from the labor report which showed increased hourly wage growth in January. Heading into the year, I was focused on accelerated wage growth like the market is now because of the low unemployment rate and jobless claims. However, I have since moderated my stance after looking closer at the underemployment rate and the labor participation rate for workers ages 25-54. I think wage growth and inflation will increase this year, but it won’t meet the now overzealous projections which are causing some analysts to worry about 4 hikes this year.

The latest Fed funds futures, according to the CME Group website, show the chance of 4 hikes is 35.7%. I can’t give a prediction for the percentage chance of a rate hike this year, but I’m still expecting 3 hikes. I’m in agreement with the market, but it doesn’t feel that way when stocks decline every time the odds of 4 hikes increase slightly. The 10 year yield fell 3 basis points to 2.86%. It’s below Monday’s low. With stocks and yields declining, it’s still clear that rising yields weren’t the main driver of the correction.

Next Friday is the monthly jobs report. Since the last report was the catalyst of the inflation fears, it will be critical to the market action in March. The current expectation is for hourly earnings to go up 0.3% month over month and 2.9% year over year. A beat could send the 10 year to 3% and stocks lower.

Q4 GDP Report Shows 2.5% Growth

The biggest current worry about monetary policy is that Powell is too hawkish. Investors wonder if the economy is strong enough to take 4 rate hikes. Some of the weak January data like the durable goods report support this narrative. The 2nd estimate for GDP growth in Q4 2017 was released. Growth was 2.5% which met expectations and was down from 2.6% in the first estimate. Consumer spending showed no change as it was up 3.8%. The inflation estimate fell one tenth from last estimate as growth was 2.3%. The core inflation estimate was revised 1 tenth higher, coming in at 2.2% which is 0.6% higher than the previous quarter.

Stock Market Hope Is Falling

One of the best things for the market would be if the sentiment comes down because of this volatility. Obviously, sharp up and down days are better than a bear market. They get the job done of ridding the market of euphoric sentiment without causing loses. If you sell on the down days and buy on the up days because you’re panicking, you’ll lose more than last year.

The Conference Board consumer confidence data was released on Tuesday along with a slew of other data. It showed consumer confidence was 130.8. This was the best report since November 2000. However, the expectation that stocks will rise in the next 12 months fell the most since March 2007 as the index declined from its record high, which was above 50, to 41.3. Normally, consumer sentiment on stocks is something I don’t care much about. However, the record high made me want to fade the market.

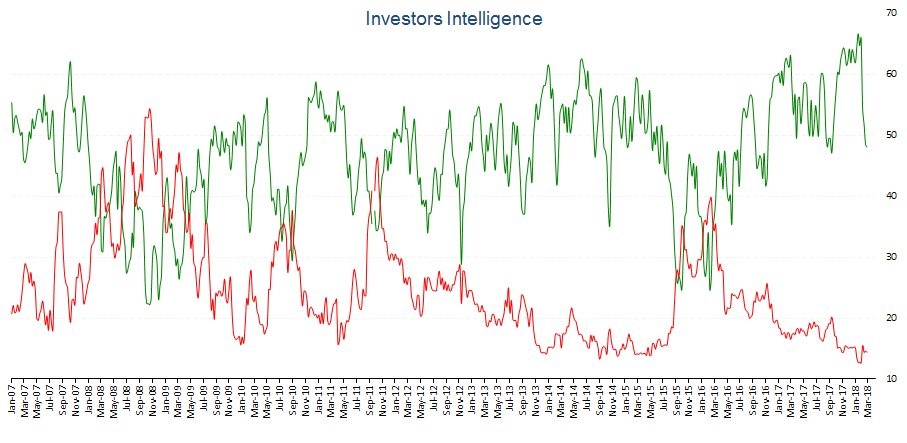

As you can see from the chart below, the Investors Intelligence reading shows the same information as the number of bulls fell from a record high to 48.1%. The number of bears is still very low (14.4%). The percentage of investors who believe this is a correction went from 20.7% to 37.5%. Obviously, it was a correction since stocks fell more than 10%. The key will be if it becomes a bear market.

GDP Estimates Gain Importance

Now that the first 2 months of the quarter are in the books, the GDP estimates for Q1 gain some relevance. On the positive side, the economy is coming off the momentum seen in 2017 and the fiscal stimulus should help growth. On the negative side, the hurricane boost should be over. Some misunderstandings about the tax cut, could hurt consumer spending in Q1. If consumers think they’re going to have to pay more taxes in 2018, then they’ll spend less. Once they figure out the situation, they’ll normalize their budget. The other potential negative is the weather which sometimes pushes down Q1 results. Finally, the government shutdown occurred in February. While the fiscal spending increase could help growth a bit this year, it won’t be felt until next quarter.

With these factors in mind, the blue chip estimates have GDP growth coming in at 2.8%. Many bears are making a big deal about how the Atlanta Fed model went from having growth at 5.4% to now having growth at 2.6%. This is a silly point because that happens very often. The St. Louis Nowcast has GDP growth coming in at 2.74%. The NY Fed has GDP growth at 3.11%. The estimates are much closer than usual. Anything between 2% and 3% would be fine. Investors aren’t worried about a recession. They’re worried about heightened inflation which causes the Fed to hike rates sharply which causes a recession in 2019.