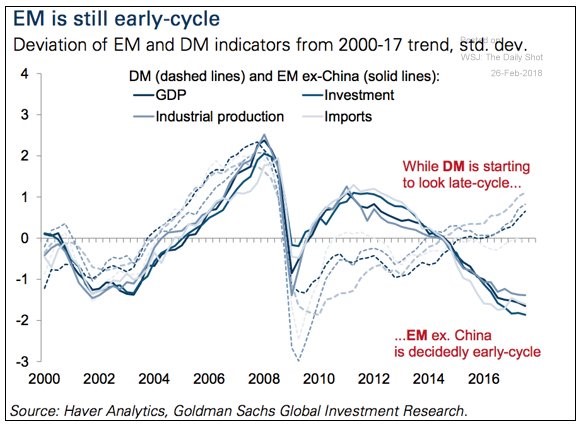

Cycles Not In Tune

The developed markets are likely a couple years away from the end of their business cycle, while emerging markets are just recovering from their recession. India and Brazil had weak economies in 2017. They’re looking to see acceleration in 2018. The countries which export commodities are probably going to have a good next couple years because prices are increasing partially due to demand from developed markets and partially because of supply constraints. As you can see, China isn’t included in the group of emerging market economies. China had a relatively strong 2017, but will probably resume its multi-year growth deceleration in 2018. China provides demand for the commodities that most emerging markets produce. Its weakness in 2018 could limit these countries’ growth. It could also limit the cycle peak in emerging markets in the next few years. However, that’s immaterial now because they are at their trough.

Since developed markets will also be weakening, it will be interesting to see how that effects emerging markets in the next few years. In 2018, developed market demand should still be strong for commodities, so emerging markets will accelerate. Once developed markets decline, it will be interesting to see if emerging markets can still improve. Developed markets stagnated a bit when emerging markets were collapsing. While weak emerging markets hurt trade growth, developed markets were helped by cheap commodities. I’ll be watching this interplay as the two groups head in opposite directions.

It’s important to point out that this interplay between emerging and developed markets isn’t the only factor that affects growth. Low unemployment and increasing inflation mean developed markets are a couple years from the end of the cycle. American stocks are very expensive, so the risk on cycle should end soon. Monetary policy in most of the developed markets is also tightening.

America Emerging & China Developed?

One other factor I think is interesting is that America has some qualities of an emerging market and China has some qualities of a developed market. No one would consider America as an emerging market economy and China as a developed market economy because of their income per capita stats. China’s income per capita is far too low to be developed and America’s is far too high to be emerging.

However, China’s population is rapidly aging like many other developed markets. Its median age is 37.3 which is up from 23.6 in 1985. Its population growth in 2018 will be 0.39%. The country’s GDP growth is all about bringing people from poverty into the middle class. Because China is transitioning to a services economy and deleveraging its debt, the GDP growth is expected to be 6.5% in 2018. However, many peg growth much lower because they don’t believe the government stats. High debt and slowing growth sounds similar to developed economies. The big differences are China’s growth is still in the mid single digits versus the low single digits for other developed economies, China’s economy is still based on manufacturing, and it has a command economy. China is supposed to be transitioning to a democracy, but that doesn’t look to be the case as the Communist party just abolished term limits for the president allowing President Xi Jinping to lead China for life.

America is like other developed nations because of its high debt and high income per capita. However, America is ahead of the curve with its monetary policy tightening as the Fed has raised rates 5 times, unlike Japan and Europe which have negative rates. America’s demographics look relatively healthy. The median age is 37.8, but the population growth rate is 0.71% which means its population is increasing unlike Italy and Japan which are in decline. The biggest reason America is like an emerging economy is its commodity resources. America has become the largest producer of oil in the world.

Leading Indicators

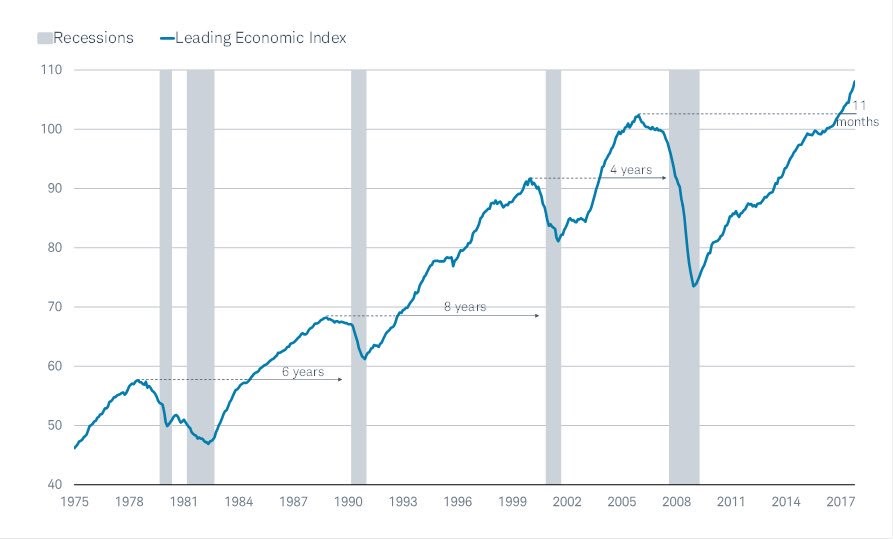

This expansion has been very long and very weak. This makes for an interesting situation where analysts call for a recession often because growth is so close to falling into the negatives, but a recession is so far away because it is taking a while to regain what was lost in the previous recession since it was so sharp and the economy is growing so slowly. Because there have been two 50% crashes in stocks since the turn of the century, it has been common to call for another one. However, this has the exact wrong call as there has been a steady bull market. The chart below is somewhat shocking because there is a temptation to forecast a recession in the next few years since this is about to be the 2nd longest expansion since 1854. However, as you can see from the chart below, the leading indicators index has only been above the previous peak for 11 months. The average time spent above the previous peak in the past 3 cycles is 6 years.

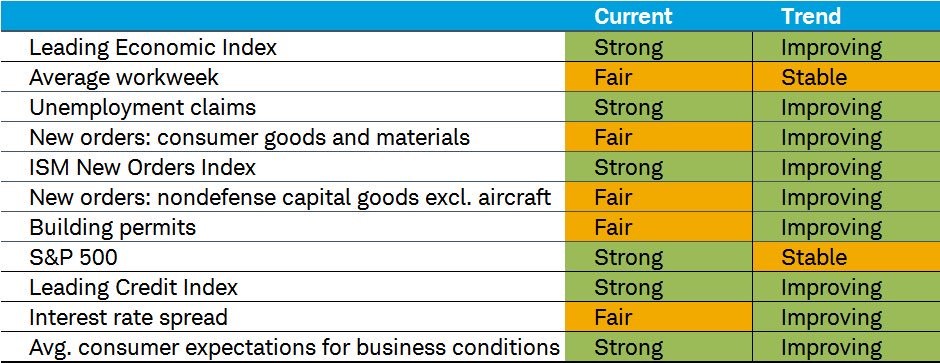

I am still in the camp that expects a recession in the next 2-3 years because of the yield curve, monetary policy, the labor market, and the output gap. This data reinforces the notion that a recession this year is very unlikely. The table below shows the breakdown of each of the metrics in the leading indicators report. As you can see, the current reports and trends are either positive or neutral. There may be some moderate GDP weakness in the first half of 2018 as forecasted by the ECRI report, but there’s nothing that indicates an impending end to the cycle.

Conclusion

I discussed the scenario where the developed economies fall into a recession in 2-3 years and the scenario where growth continues for the next few years. When you’re investing, you need to have an economic world view for the next 12 months. However, you can be open to a few possibilities when discussing the next few years. It’s difficult enough to predict where the economy is headed in the next 12 months. There’s no reason to pigeon hole yourself into a thesis on where the economy will be in 3 years. This is why I discuss both the bullish and bearish perspectives.