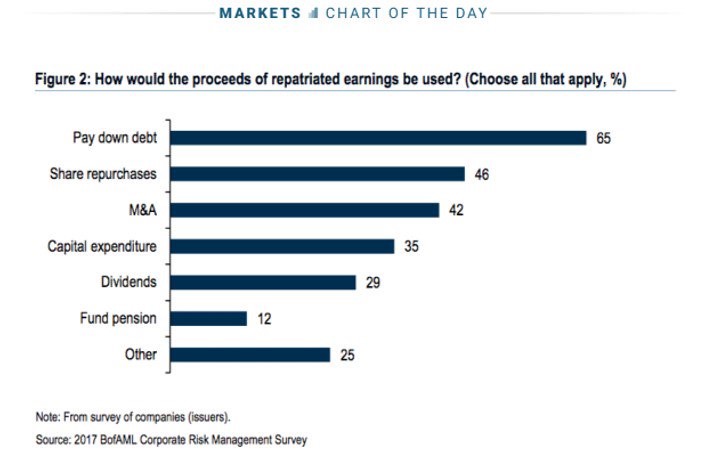

What Will Firms Do With The Extra Cash?

With the tax cuts passing today, there have been some firms announcing pay increases and investments. It’s easy to get caught up in anecdotal evidence from headlines. The chart below gives you a more complete picture of what firms are likely to do with the extra money. It shows what firms said they would do with the repatriated cash. Clearly, some mentioned a few options because the results add up to more than 100%. It’s not surprising to see funding pensions at the bottom of this list because unlike public pensions which are a disaster, private ones are well funded. The decision to pay down debt being at the top might signal that firms feel they have too much debt. The other way to rationalize this is firms have been issuing debt backed by the capital overseas to avoid paying high tax rates. Now that the cash can come back, firms are ending this process by paying back the debt they only issued because they couldn’t bring their earnings back home.

The GOP is hoping firms put money into capital expenditures like they are saying in this poll. The issue is whether firms have a place to invest the capital they are bringing back. That’s where regulation cuts come in. Less regulations will allow some firms to invest in places they couldn’t previously. Because the economy is growing quickly, it makes sense firms would reinvest capital back into their businesses.

Investment Grade Yields Can Increase

The analyst earnings expectations in the past few years up until this one all fell throughout the year. This was the first year where earnings came close to meeting estimates. As I mentioned previously, 2018 is looking even better as expectations have been increasing in the past few weeks. One thing to consider, which counters the narrative that S&P 500 earnings will be over $10 higher because of the tax cuts, is that higher yields mean firms will need to borrow at higher rates. This could cut into profits. A few months ago, it was questionable if firms like Apple would repatriate their cash because they pay such low rates on their debt. The situation still looks phenomenal for firms borrowing money, but the question is if it will go from great to good in the next year. BBB corporate bond yields have increased from 3.39% on September 7th to 3.63%. This is a small move, but if it keeps going higher like I expect, it will encourage more firms to repatriate their cash and use the money to pay off debt. Investment grade bonds should follow the increase in Treasury yields. As I mentioned previously, the 30 year bond has a lot of excess speculation in it on the long side.

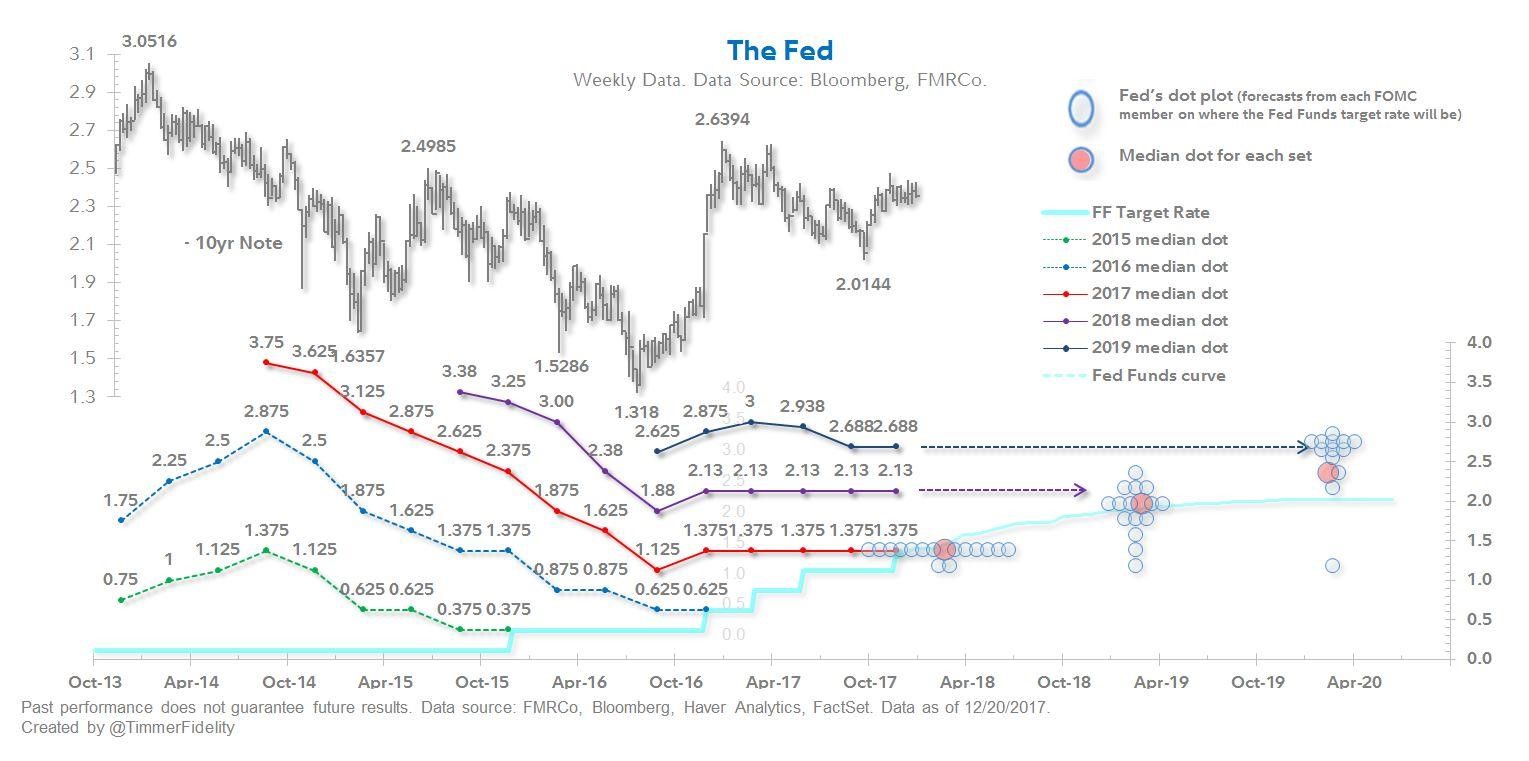

Fed Has Been Consistent Lately

Just like I mentioned how analysts have been consistent in the past few months because corporate earnings and guidance have been strong, the Fed has also been consistent with its expectations. The chart below shows the historical changes in the median dot plot in the past few years. As you can see, the 2016 and 2017 dot plots saw big declines in 2015 and 2016 as the economy was weak. Now that it is strong, the dot plots have been remarkably stable. The Fed stuck with its guidance for 3 rate hikes in 2017. It’s tough to understand what the long term Fed funds target rate means because it hasn’t changed recently. The 2018 median rate is now higher than the long term target. This could be implying the Fed will cut rates again in the next recession. The Fed funds rate getting above the natural rate means the financial conditions should tighten in the next few quarters.

Amazon Could Single Handily Limit Long Term Inflation

Technology improvements lead to deflation because products can be made cheaper and the cost cuts are passed down to the consumer. It’s interesting to see large competitors exert their full force on the market, causing prices to decrease in the overall economy. We saw it with Wal-Mart suppressing core inflation by 0.2% and we have seen it with Amazon which has suppressed core inflation 0.1%. If Amazon continues its trajectory, it can suppress inflation over the long term even more than it has.

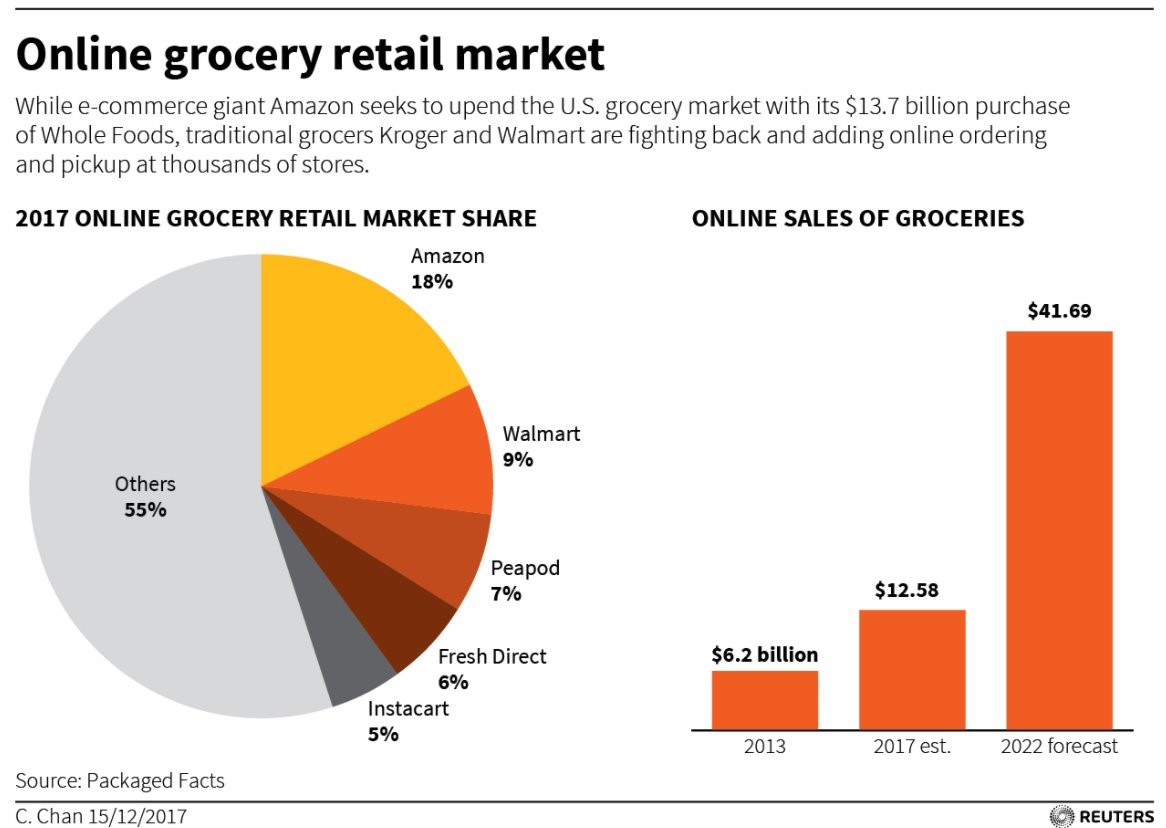

The chart below looks at the grocery business which Amazon has gotten more invested in with the acquisition of Whole Foods. As you can see, Amazon has an 18% market share in the online grocery market. That is double its nearest competitor which is Wal-Mart. The shuffling of market share points doesn’t matter as much now as it will in the future as the online grocery business expands rapidly in the next few years. As you can see, the market is expected to go from $12.5 billion in sales to $41.69 billion in the next 5 years. Amazon could be in a situation where it grows its market share in the online category and sees the only category take share from brick and mortar stores. This will suppress food price growth as Amazon is more efficient than other firms; it’s also willing to have low margins in some businesses which it makes up for with its highly profitable cloud business.

Going off on a quick tangent, this market share battle that Amazon is winning versus brick and mortar stores is a threat to Google. While Google will always be a search leader for information, when it comes to buying products, many people will sidestep Google’s search function and go directly to Amazon.com. If purchases occur less from clicks on Google ads, its profits dry up.

Conclusion

High borrowing costs will crimp margins in the next few years. Tax cuts lessen the blow, but they also are part of the reason why interest rates are going up as the economy starts to grow faster than its potential. It’s great to see the initial pickup in hiring, buybacks, and wages from this tax cut. Hopefully, these anecdotal results start to show up in the overall data in 2018.