Politics Pushes Stocks Around

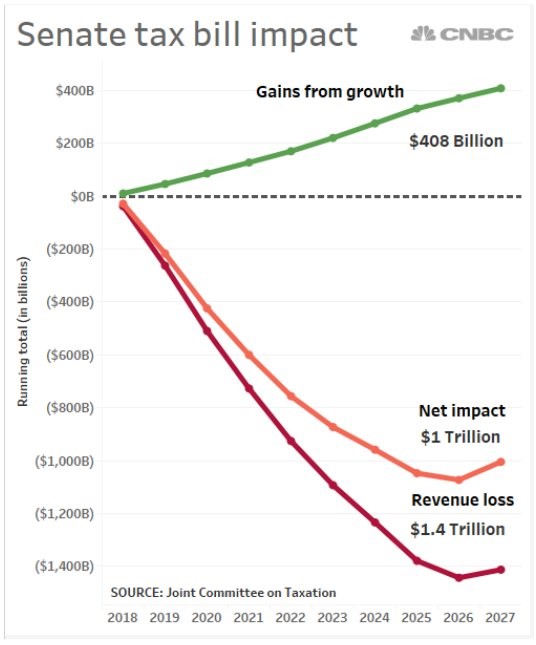

There was a sharp but temporary correction on Friday as it was reported that Michael Flynn will cooperate with Mueller’s special council. As with most political risks, the market shook it off after a few hours as the Dow only closed down 41 points and the S&P 500 was down 0.20%. This is a case of politics giving us a rally because of tax cuts and then taking it away with an investigation. The Senate vote on tax reform was 51-49, meaning it passed. Senate Majority Leader, Mitch McConnell said he had the votes necessary to pass the bill and he was right. Only Senator Corker voted against the plan because it adds to the debt. The next step will be getting the House and the Senate to agree on something. We will get more information on how that will set up in a few days. The chart below shows an analysis of the tax plan broken down by the net impact to the debt. As you can see, the growth will help the net impact become negative $1 trillion. In the end, the market doesn’t care much about how much the government deficits are as you can tell by this bull market occurring with very high deficits. The $408 billion in economic gains are enough to help the stock market lift off in December.

Bond Market Warning Signs

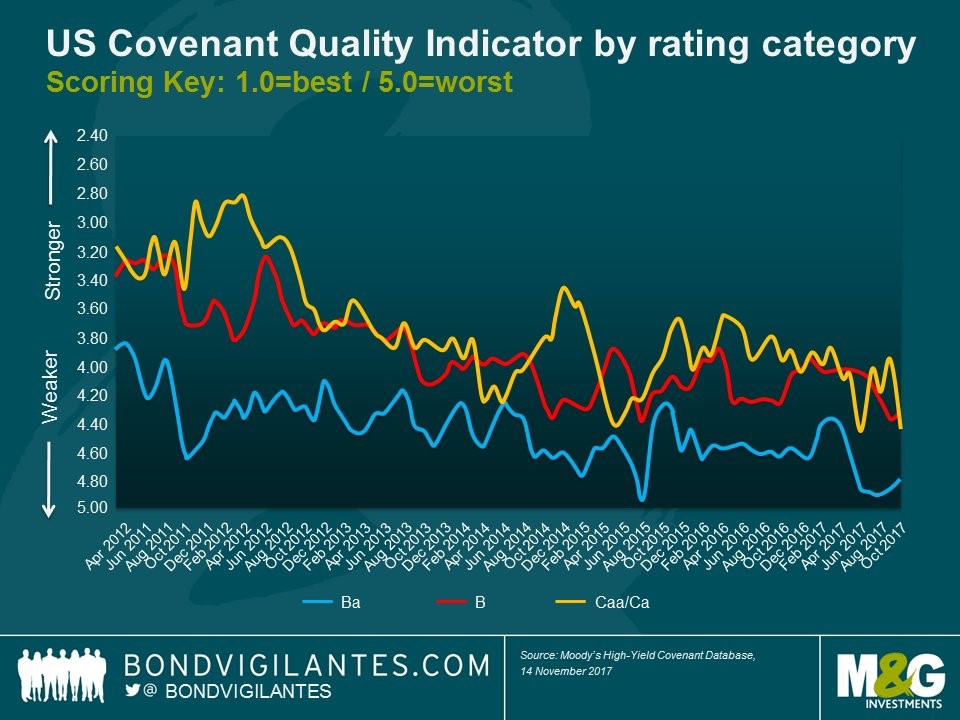

If you asked me to list the biggest risks to the market over the next two years I would say they are inflation, student loan debt, the auto loan market, and the popularity of covenant lite loans. The new way to issue loans is to not have much restrictions on the firms borrowing it. I would rather just buy the stock of the company asking for a covenant lite loan. You can see in the chart below the covenant quality indicator for 3 types of bonds has fallen in the past few years. This is one of the few indicators which has fallen since the economy has recovered in the past 12 months. The reason is this metric isn’t cyclical. There has been a wholesale change in lending standards because interest rates are so low and credit spreads are so tight. The obvious question is what will happen when the next recession occurs. A recession would probably push these standards higher because spreads would widen and rates will probably increase. At that point we’ll figure out if this change was a good idea or not. The hope is there aren’t expansive defaults. The issue is that bondholders probably shouldn’t need to rely hope when it comes to their investments.

Another risk that is necessary to watch out for next year is the financial conditions tightening. The chart below shows the Chicago Fed’s financial conditions index. As you can see, credit is the most loose it has been since 1993. Generally, conditions don’t stay that way. It will be especially difficult for them to stay loose with the Fed raising rates 2 more times, accelerating the unwind, and the ECB tapering its bond buying. I think tightening conditions will increase volatility in stocks. It wouldn’t take much for volatility to go up since this was one of the quietest years ever. I’m not saying these factors will push the market down for the year; I’m expecting 2018 to be more exciting for the stock market.

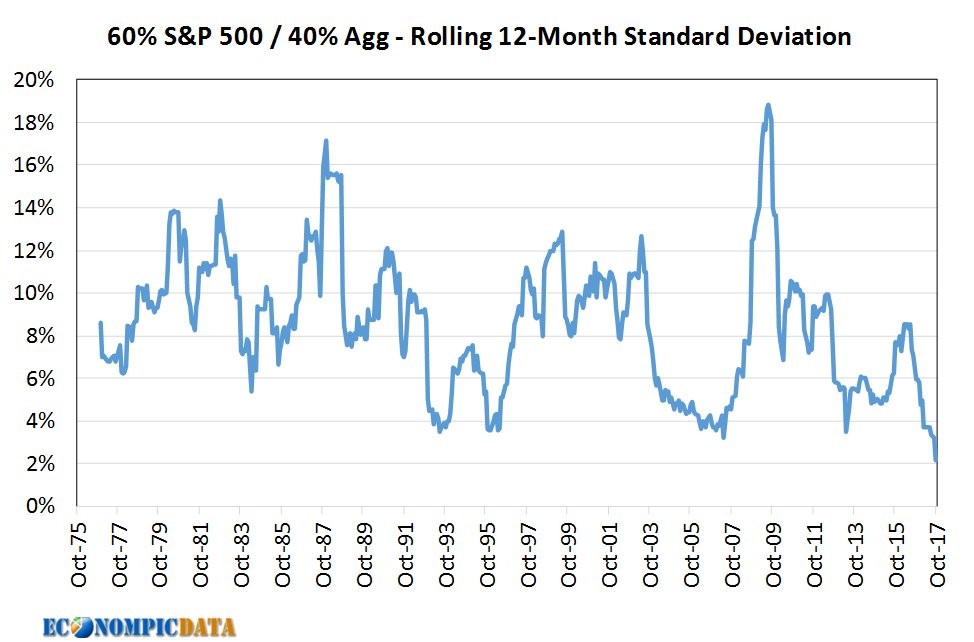

As I mentioned, 2017 has been a quiet year. The chart below provides evidence of that as a mock portfolio with a 60% allocation to stocks and a 40% allocation to bonds has the lowest 12 month rolling standard deviation in the past 32 years. This is lower than in 1993 when the financial conditions index hit its trough of -0.93. I expect there to be issues in both the bond and stock markets if inflation picks up next year.

Fed Ready To Make Another Solid Move

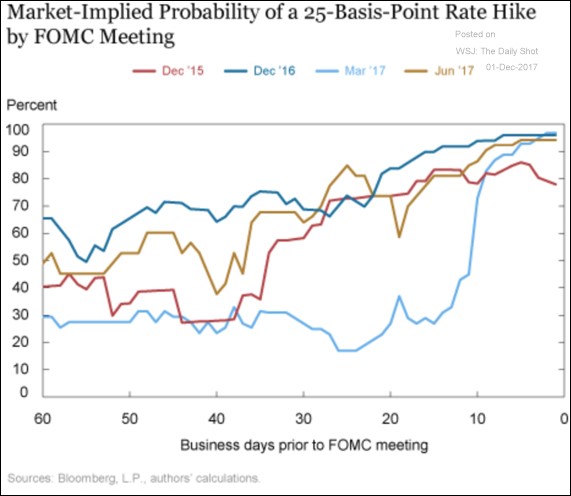

With the way politics effected stocks this week and the way monetary policy seemingly hasn’t mattered in a few quarters, you’d wonder why we bother to discuss the Fed at all. The reason why we discuss the Fed is because it is affecting the markets, just not on decision days because the market gets what it expects. The great thing is the Fed hasn’t made many mistakes recently. 2017 went according to plan in terms of policy although inflation and wage growth missed the mark. The Fed has eliminated uncertainty by doing exactly what the market expects. As you can see from the chart below, the Fed has only hiked rates when the market was sure it would. We’re in the same situation as the last 4 hikes as the market is 100% certain there will be a hike on December 13th. There’s a 92.8% chance of one hike and a 7.2% chance of 2 hikes.

This will be the last hike under Yellen. Her legacy is she started the balance sheet unwind and hiked rates more than half way to the long run expectations. That could change because an increase in inflation can push rates much higher. The deciding factor on whether Yellen and Bernanke were good chairs is the size of the next recession. If it’s large, skeptics will say they created it with QE and low rates. It is a normal recession, Yellen and Bernanke will be lauded for getting us out of the financial crisis and being in charge during very peaceful times for the market.

Conclusion

Politics dominated Friday’s action as the Senate passed the tax cut and Mueller’s investigation into General Flynn was in the news. Ultimately, this period where politics affects stocks will end. What will drive stocks in 2018 will be earnings growth and inflation (along with how the Fed handles it). This final rate hike by Yellen will be like the others in that it’s expected by the market. Hopefully, Powell can lead the Fed in the same fashion. There’s a strong possibility the Fed gives less media interviews under Powell which might mean more uncertainty. That could mean more volatility in stocks.