The chart below is in keeping with the previous article about how stocks rallied on the hopes of a tax reform plan passing the Senate as early as November. As you can see, the companies that benefit the most from the plan, the high taxed firms, outperformed the overall market. When you break out the companies that do the best in a low tax environment, it gives you a proxy for the betting odds of it passing. It’s tough to argue with the odds because political issues are tough to get a grasp of. The GOP is definitely highly motivated to get something done because at this rate they don’t have any major accomplishments to show the voters in 2018. The issue is paying for the tax cuts. Any rational person wouldn’t try to lower taxes before cutting spending since the deficit is already high, but politics is a tough business.

There’s three legs: doing what you believe, doing what the voters want, and listening to what you political opponents are willing to give up. The 3 legged stool hasn’t been functioning this year. Some are saying that this will be tougher to get done than healthcare reform; that’s another way of saying it won’t happen. Personally, I think politicians only get things done when their backs are against the wall, so I think we’ll see tax reform right before the election. The worst thing for the odds of the tax cuts is that the GOP has won all the special elections. Those wins won’t motivate them to act. However, even with those wins, they don’t have enough control to pass legislation easily because those elections replaced Republicans with Republicans.

The chart below does a great job of explaining the confusing headlines from the business news websites. They seem to describe every rally in stocks as being caused by tax cuts. However, the companies that benefit from tax cuts are down for the year. That means the market is rallying because of great earnings, great global growth, and a dovish Fed, not tax cuts. If cuts were made, stocks would be even higher.

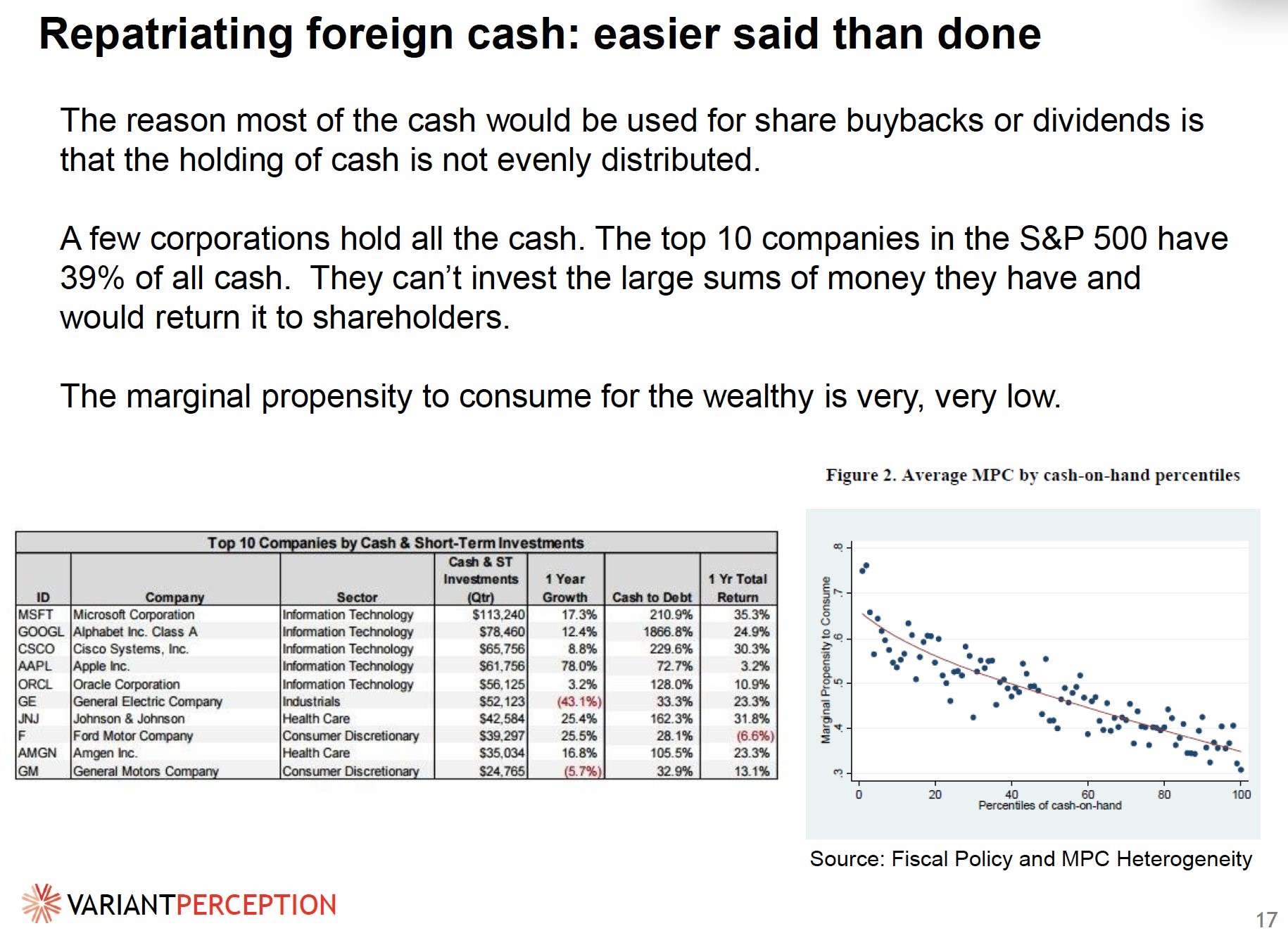

The chart below does an interesting analysis of the possibilities the repatriation tax holiday has. There is a lot of moving parts such as the tax rates and the decisions made by the individual companies. The slide below shows how the cash in the hands of a few companies. 39% of the cash is held by the top 10 companies in the S&P 500. The argument this slide makes is that the marginal propensity to consume is low for these wealthy companies, so they’ll use the money for buybacks. That’s a plausible conclusion, but it could be turned on its head if one or two companies use the money for an acquisition or a big investment. Percentages can easily be inaccurate when you’re talking about small numbers. It could make sense to do an analysis of each of the 10 companies to get a better idea of what will happen instead of looking at it from the top down. That’s a type of analysis that can be done after the plan is solidified. That means the articles about which company AAPL might buy will sprout up again.

The top economic news on Wednesday was the U.S. durable goods orders which rose 1.7% in August which was above the 1% increase expected by analysts. This was led by the 4.9% increase in bookings for transportation equipment. This positive result occurred in spite of the hurricanes hurting activity. The Commerce Department said it couldn’t isolate the effect of the hurricanes to determine what the report would have been without them. The great report helped push the odds of a December rate hike up to 83.1% which is the highest ever. The Fed will finally get its initial 3 hike guidance in, even though inflation has disappointed for much of the year.

The 2 year bond has the highest yield since 2008 because of anticipated rate hikes. The non-defense capital goods orders were up 0.9% in August on a month over month basis after being up 1.1% in July. They were up 3.3% on a year over year basis. The dollar index rallied to $93.59 on the news. It’s up significantly from the bottom of $91.35 on September 8th. I had been talking about a potential counter trend rally in the dollar because it has been oversold. I think if it wasn’t for the hurricanes, the economic data would be better and the dollar would be in the mid-$90s. It’s tough to say if the tax cuts are good or bad for the dollar because they blow a hole in the balance sheet of the country, but they boost economic growth.

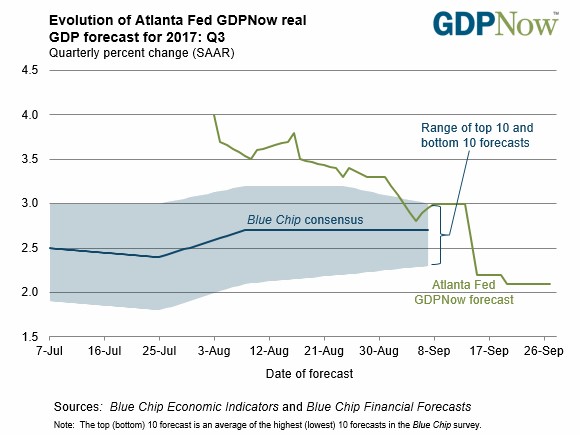

The chart below shows what the latest economic data has done to the GDP Now Q2 forecast. As you can see, the forecast has declined from 2.2% to 2.1% as it has fallen from above the blue chip consensus to below it. The latest decline was caused by weakness in the real residential investment growth forecast which was caused by the weak housing data which was blamed on the hurricanes. The weakness was offset by strength in the real nonresidential equipment investment growth forecast which was caused by the durable manufacturing report we just discussed. If the NY Fed’s update on Friday increases, the Atlanta Fed could be the gloomiest of the bunch. That’s a far cry from the 4% growth initially expected.

Conclusion

The tax cut issue is a huge political football that will be discussed often. It’s tough to trade on the policy because we don’t know how the politics will end up. However, it’s still worth watching closely because it will affect stocks when decisions are made.

The great durable goods orders surprised me. It means either the economy is very strong and able to overcome weather issues or it means the weather didn’t affect the report. The next report for September will be affected by weather, but it might be in a positive way. That might boost GDP forecasts back up closer to 2.5%.